Advertisement

- Hong Kong

- /

- Basic Materials

- /

- SEHK:1252

Pinning Down China Tianrui Group Cement Company Limited's (HKG:1252) P/S Is Difficult Right Now

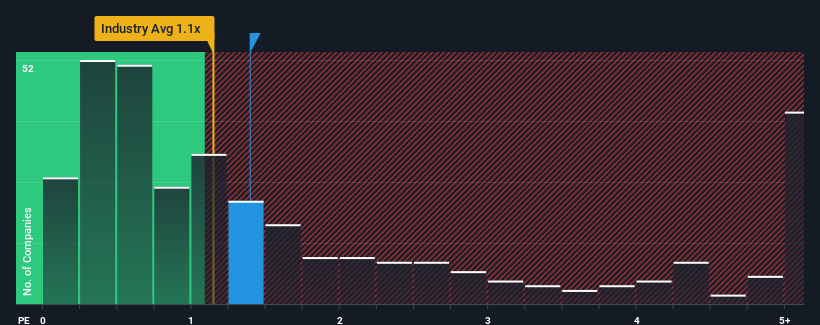

When you see that almost half of the companies in the Basic Materials industry in Hong Kong have price-to-sales ratios (or "P/S") below 0.4x, China Tianrui Group Cement Company Limited (HKG:1252) looks to be giving off some sell signals with its 1.4x P/S ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the elevated P/S.

Check out our latest analysis for China Tianrui Group Cement

How China Tianrui Group Cement Has Been Performing

For instance, China Tianrui Group Cement's receding revenue in recent times would have to be some food for thought. It might be that many expect the company to still outplay most other companies over the coming period, which has kept the P/S from collapsing. However, if this isn't the case, investors might get caught out paying too much for the stock.

We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on China Tianrui Group Cement's earnings, revenue and cash flow.How Is China Tianrui Group Cement's Revenue Growth Trending?

The only time you'd be truly comfortable seeing a P/S as high as China Tianrui Group Cement's is when the company's growth is on track to outshine the industry.

Retrospectively, the last year delivered a frustrating 21% decrease to the company's top line. The last three years don't look nice either as the company has shrunk revenue by 18% in aggregate. So unfortunately, we have to acknowledge that the company has not done a great job of growing revenue over that time.

It turns out the industry is also predicted to shrink 4.4% in the next 12 months, mirroring the company's downward momentum based on recent medium-term annualised revenue results.

In light of this, it's somewhat peculiar that China Tianrui Group Cement's P/S sits above the majority of other companies. With revenue going in reverse, it's not guaranteed that the P/S has found a floor yet. There's strong potential for the P/S to fall to lower levels if the company doesn't improve its top-line growth, which would be difficult to do with the current industry outlook.

What Does China Tianrui Group Cement's P/S Mean For Investors?

Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

Based on our analysis, it's clear that China Tianrui Group Cement is trading at a higher-than-average P/S ratio despite its recent three-year revenue growth rate only matching the industry forecasts for a struggling sector. Right now we are uncomfortable with the high P/S as this revenue performance isn't likely to support such positive sentiment for long. We're also cautious about the company's ability to stay its recent medium-term course and resist further pain to its business from the broader industry turmoil. Unless the company's relative performance improves, it's challenging to accept these prices as being reasonable.

Plus, you should also learn about these 3 warning signs we've spotted with China Tianrui Group Cement (including 2 which make us uncomfortable).

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1252

China Tianrui Group Cement

An investment holding company, engages in the manufacture and sale of cement, clinker, and limestone aggregates in the People’s Republic of China.

Slightly overvalued with imperfect balance sheet.

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|26.3% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|4.8% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor