Advertisement

- Hong Kong

- /

- Healthcare Services

- /

- SEHK:2289

Investors Holding Back On Charmacy Pharmaceutical Co., Ltd. (HKG:2289)

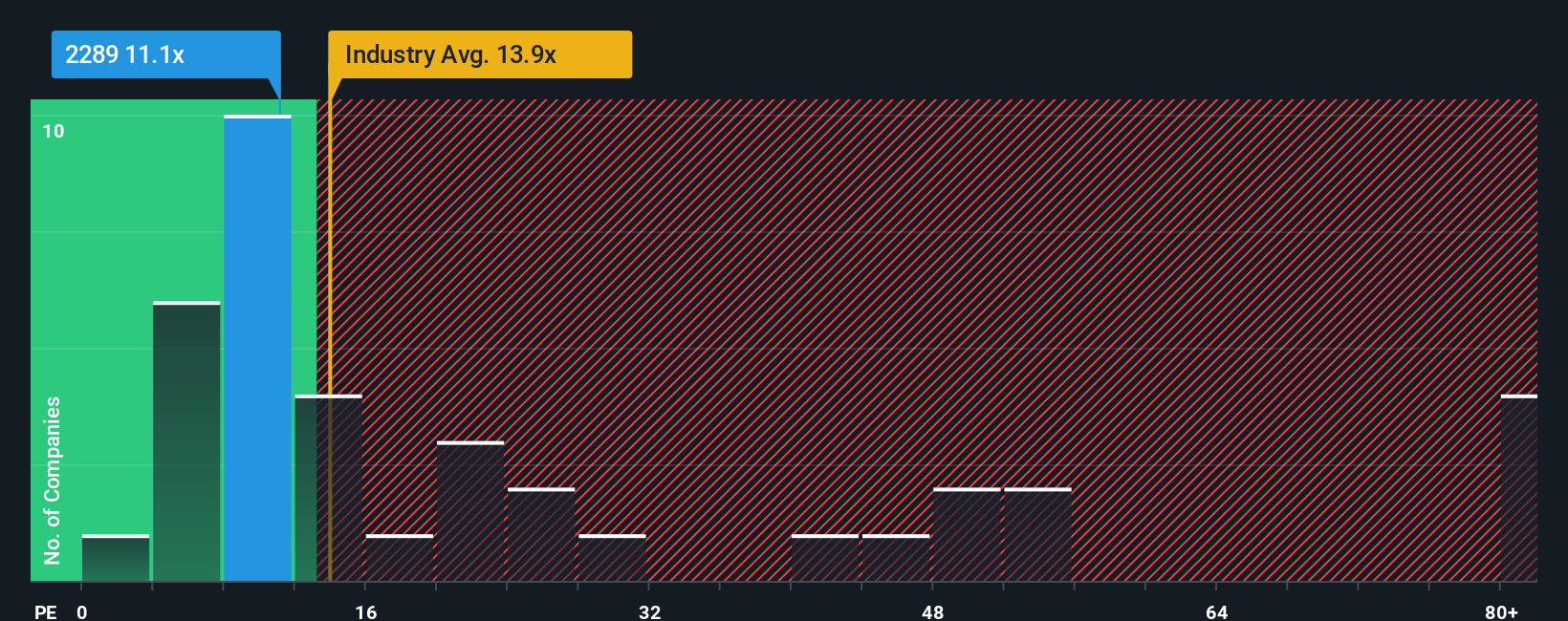

There wouldn't be many who think Charmacy Pharmaceutical Co., Ltd.'s (HKG:2289) price-to-earnings (or "P/E") ratio of 11.1x is worth a mention when the median P/E in Hong Kong is similar at about 12x. While this might not raise any eyebrows, if the P/E ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

The recent earnings growth at Charmacy Pharmaceutical would have to be considered satisfactory if not spectacular. One possibility is that the P/E is moderate because investors think this good earnings growth might only be parallel to the broader market in the near future. If not, then at least existing shareholders probably aren't too pessimistic about the future direction of the share price.

See our latest analysis for Charmacy Pharmaceutical

What Are Growth Metrics Telling Us About The P/E?

The only time you'd be comfortable seeing a P/E like Charmacy Pharmaceutical's is when the company's growth is tracking the market closely.

Retrospectively, the last year delivered a decent 3.8% gain to the company's bottom line. Pleasingly, EPS has also lifted 130% in aggregate from three years ago, partly thanks to the last 12 months of growth. Therefore, it's fair to say the earnings growth recently has been superb for the company.

Weighing that recent medium-term earnings trajectory against the broader market's one-year forecast for expansion of 21% shows it's noticeably more attractive on an annualised basis.

With this information, we find it interesting that Charmacy Pharmaceutical is trading at a fairly similar P/E to the market. It may be that most investors are not convinced the company can maintain its recent growth rates.

The Key Takeaway

Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that Charmacy Pharmaceutical currently trades on a lower than expected P/E since its recent three-year growth is higher than the wider market forecast. When we see strong earnings with faster-than-market growth, we assume potential risks are what might be placing pressure on the P/E ratio. At least the risk of a price drop looks to be subdued if recent medium-term earnings trends continue, but investors seem to think future earnings could see some volatility.

You need to take note of risks, for example - Charmacy Pharmaceutical has 3 warning signs (and 1 which is a bit unpleasant) we think you should know about.

If these risks are making you reconsider your opinion on Charmacy Pharmaceutical, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:2289

Charmacy Pharmaceutical

Engages in the pharmaceutical distribution business in the People’s Republic of China.

Good value with proven track record.

Market Insights

Advertisement

Community Narratives

Gaxos.ai: Early-Stage AI Innovator in Gaming & Health

Fair Value US$2.21|5.9% undervalued

JO

Community Contributor

After the AI Party: A Sobering Look at Microsoft's Future

Fair Value US$500.00|1.4% overvalued

PI

Community Contributor

Amazon's Future Rises as Stock Price Falls: A Long-Term Investment Vision

Fair Value US$234.75|2.5% undervalued

ZW

Community Contributor