- Hong Kong

- /

- Healthcare Services

- /

- SEHK:2135

Revenues Working Against Raily Aesthetic Medicine International Holdings Limited's (HKG:2135) Share Price Following 47% Dive

Unfortunately for some shareholders, the Raily Aesthetic Medicine International Holdings Limited (HKG:2135) share price has dived 47% in the last thirty days, prolonging recent pain. The recent drop completes a disastrous twelve months for shareholders, who are sitting on a 82% loss during that time.

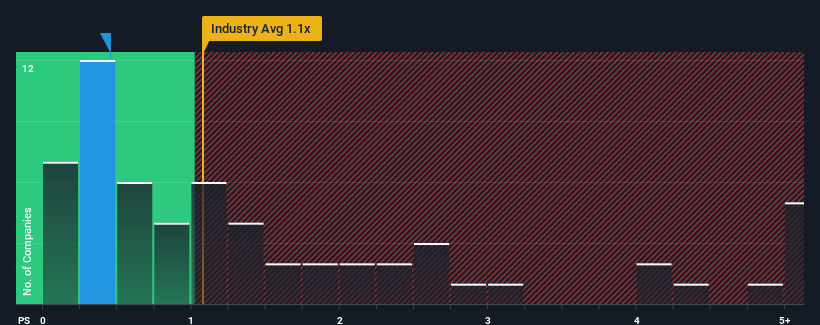

Following the heavy fall in price, when close to half the companies operating in Hong Kong's Healthcare industry have price-to-sales ratios (or "P/S") above 1.1x, you may consider Raily Aesthetic Medicine International Holdings as an enticing stock to check out with its 0.5x P/S ratio. However, the P/S might be low for a reason and it requires further investigation to determine if it's justified.

Check out our latest analysis for Raily Aesthetic Medicine International Holdings

What Does Raily Aesthetic Medicine International Holdings' P/S Mean For Shareholders?

The revenue growth achieved at Raily Aesthetic Medicine International Holdings over the last year would be more than acceptable for most companies. It might be that many expect the respectable revenue performance to degrade substantially, which has repressed the P/S. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on Raily Aesthetic Medicine International Holdings will help you shine a light on its historical performance.Is There Any Revenue Growth Forecasted For Raily Aesthetic Medicine International Holdings?

The only time you'd be truly comfortable seeing a P/S as low as Raily Aesthetic Medicine International Holdings' is when the company's growth is on track to lag the industry.

Retrospectively, the last year delivered an exceptional 15% gain to the company's top line. The latest three year period has also seen a 15% overall rise in revenue, aided extensively by its short-term performance. Accordingly, shareholders would have probably been satisfied with the medium-term rates of revenue growth.

This is in contrast to the rest of the industry, which is expected to grow by 16% over the next year, materially higher than the company's recent medium-term annualised growth rates.

With this information, we can see why Raily Aesthetic Medicine International Holdings is trading at a P/S lower than the industry. Apparently many shareholders weren't comfortable holding on to something they believe will continue to trail the wider industry.

What We Can Learn From Raily Aesthetic Medicine International Holdings' P/S?

The southerly movements of Raily Aesthetic Medicine International Holdings' shares means its P/S is now sitting at a pretty low level. We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

As we suspected, our examination of Raily Aesthetic Medicine International Holdings revealed its three-year revenue trends are contributing to its low P/S, given they look worse than current industry expectations. At this stage investors feel the potential for an improvement in revenue isn't great enough to justify a higher P/S ratio. Unless the recent medium-term conditions improve, they will continue to form a barrier for the share price around these levels.

Plus, you should also learn about these 4 warning signs we've spotted with Raily Aesthetic Medicine International Holdings (including 2 which are significant).

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

If you're looking to trade Raily Aesthetic Medicine International Holdings, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:2135

Raily Aesthetic Medicine International Holdings

An investment holding company, engages in the provision of aesthetic medical services in the People’s Republic of China.

Mediocre balance sheet low.

Market Insights

Community Narratives