- Japan

- /

- Professional Services

- /

- TSE:9216

3 Compelling Dividend Stocks Offering Yields Up To 5.1%

Reviewed by Simply Wall St

As global markets react to political developments and economic indicators, major U.S. indices have reached new highs, driven by optimism around potential trade deals and AI investments. In this dynamic environment, dividend stocks remain an attractive option for investors seeking steady income streams, especially as some offer yields up to 5.1%, providing a cushion against market volatility and economic uncertainties.

Top 10 Dividend Stocks

| Name | Dividend Yield | Dividend Rating |

| Wuliangye YibinLtd (SZSE:000858) | 3.67% | ★★★★★★ |

| CAC Holdings (TSE:4725) | 4.63% | ★★★★★★ |

| Yamato Kogyo (TSE:5444) | 4.07% | ★★★★★★ |

| Padma Oil (DSE:PADMAOIL) | 7.44% | ★★★★★★ |

| GakkyushaLtd (TSE:9769) | 4.38% | ★★★★★★ |

| China South Publishing & Media Group (SHSE:601098) | 4.01% | ★★★★★★ |

| Guangxi LiuYao Group (SHSE:603368) | 3.41% | ★★★★★★ |

| Nihon Parkerizing (TSE:4095) | 3.95% | ★★★★★★ |

| E J Holdings (TSE:2153) | 4.05% | ★★★★★★ |

| DoshishaLtd (TSE:7483) | 3.80% | ★★★★★★ |

Click here to see the full list of 1964 stocks from our Top Dividend Stocks screener.

Let's review some notable picks from our screened stocks.

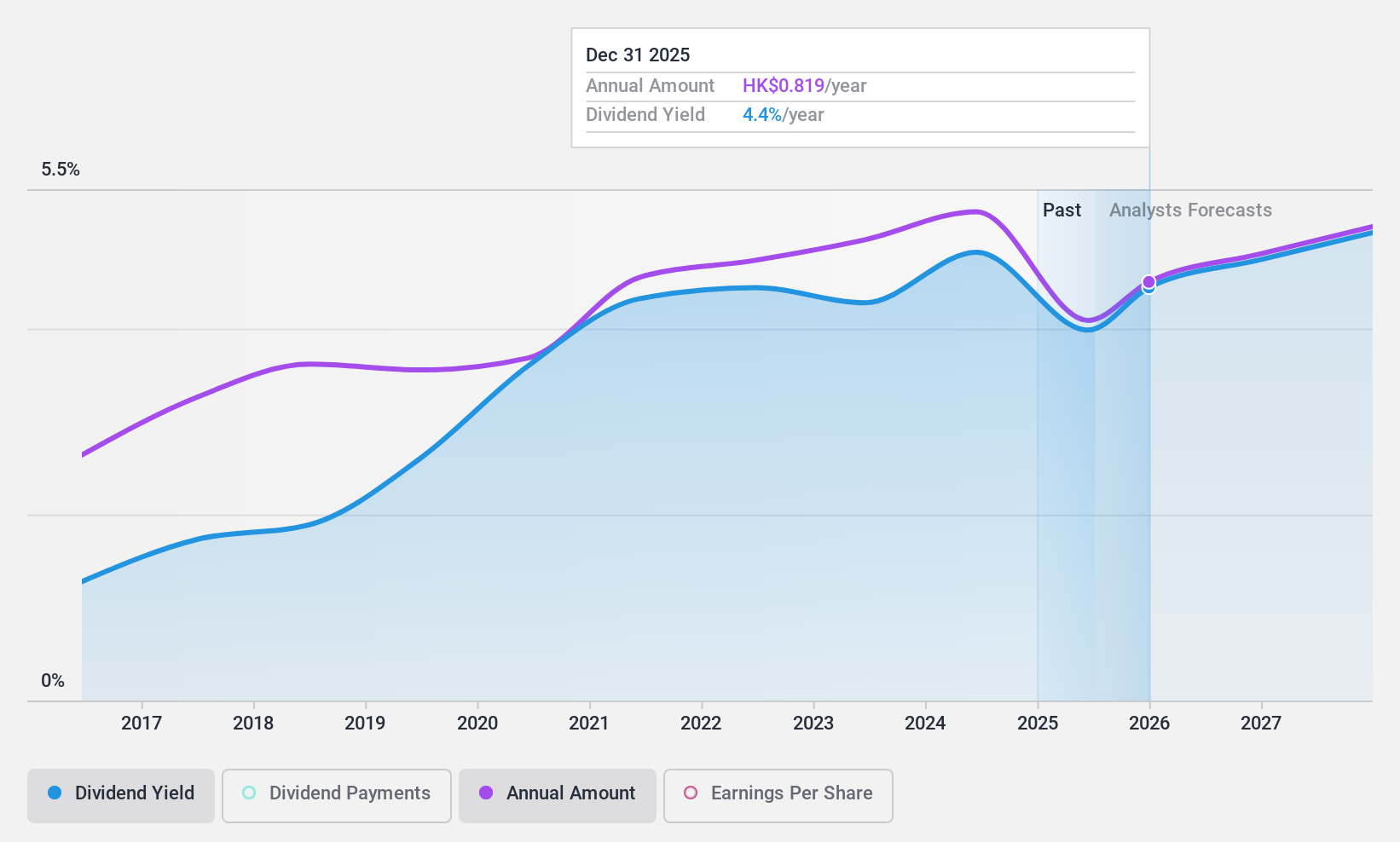

Sinopharm Group (SEHK:1099)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Sinopharm Group Co. Ltd., along with its subsidiaries, operates in the wholesale and retail sectors for pharmaceuticals, medical devices, and healthcare products in China, with a market cap of HK$63.97 billion.

Operations: Sinopharm Group Co. Ltd.'s revenue is primarily derived from pharmaceutical distribution (CN¥442.11 billion), medical devices (CN¥125.75 billion), and retail pharmacy (CN¥34.55 billion).

Dividend Yield: 4.5%

Sinopharm Group's dividend profile is characterized by reliability and sustainability, with a payout ratio of 31.3% and a cash payout ratio of 16%, indicating strong coverage by earnings and cash flows. Despite trading at 62.4% below estimated fair value, recent financials show a decline in net income to CNY 5.28 billion for the first nine months of 2024. Executive board changes may impact strategy, but dividends have grown steadily over the past decade.

- Delve into the full analysis dividend report here for a deeper understanding of Sinopharm Group.

- The valuation report we've compiled suggests that Sinopharm Group's current price could be quite moderate.

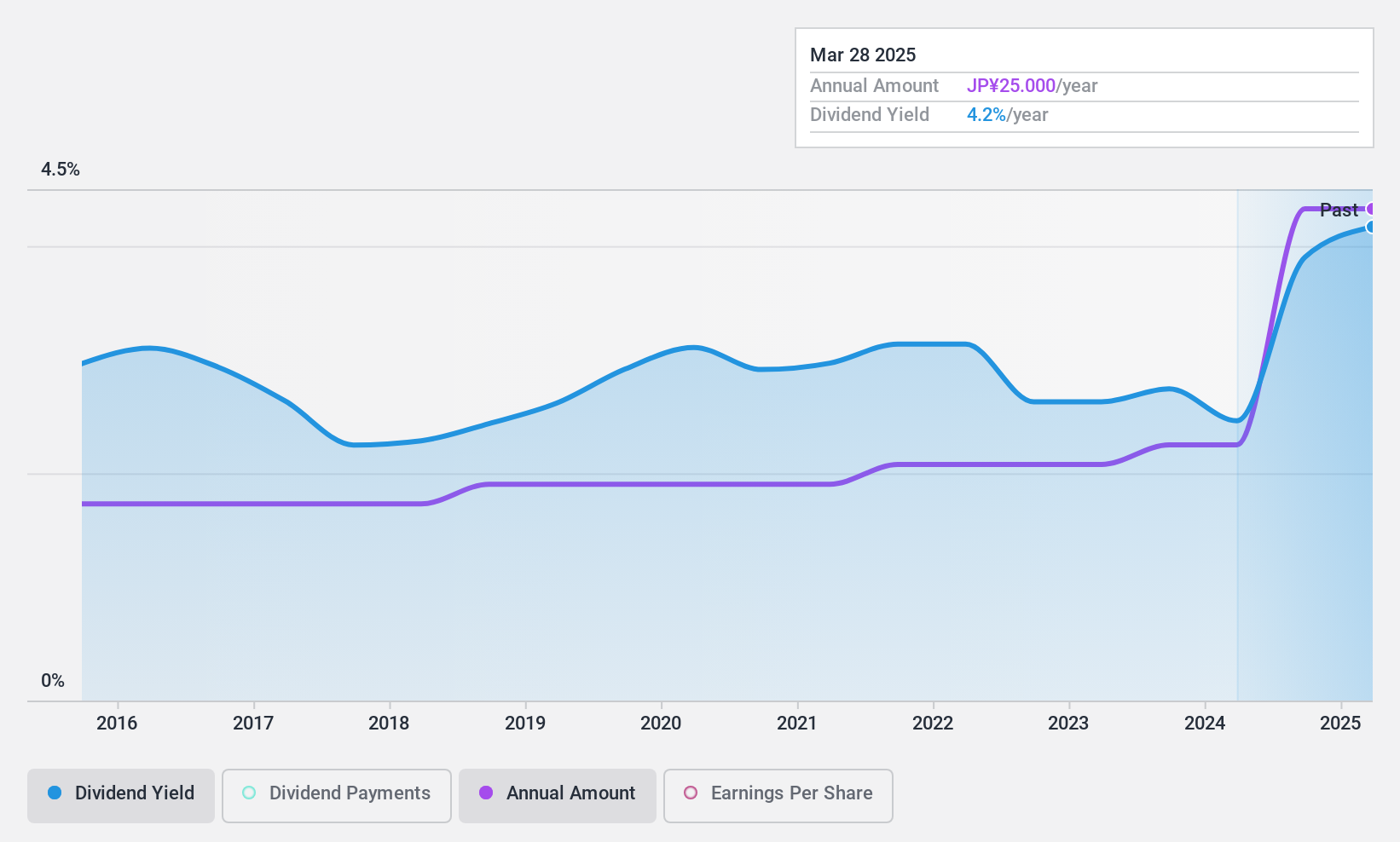

Japan Pulp and Paper (TSE:8032)

Simply Wall St Dividend Rating: ★★★★★★

Overview: Japan Pulp and Paper Company Limited operates in the manufacture, import, export, distribution, wholesale, and sale of papers, paperboards, pulp, and paper-related products across Japan and internationally with a market cap of ¥80.94 billion.

Operations: Japan Pulp and Paper's revenue segments include Domestic Wholesale at ¥207.04 billion, Overseas Wholesale at ¥265.27 billion, Paper Processing at ¥56.13 billion, Real Estate Rental at ¥4.24 billion, and Environmental Raw Materials at ¥29.68 billion.

Dividend Yield: 3.8%

Japan Pulp and Paper's dividend payments are well-supported by a low payout ratio of 22% and a cash payout ratio of 10.2%, ensuring coverage by earnings and cash flows. The company has consistently increased dividends over the past decade, maintaining stability with recent affirmations of JPY 125 per share. While its dividend yield is attractive at 3.81%, recent ¥10 billion fixed-income offerings may impact financial flexibility given its high debt level.

- Unlock comprehensive insights into our analysis of Japan Pulp and Paper stock in this dividend report.

- According our valuation report, there's an indication that Japan Pulp and Paper's share price might be on the cheaper side.

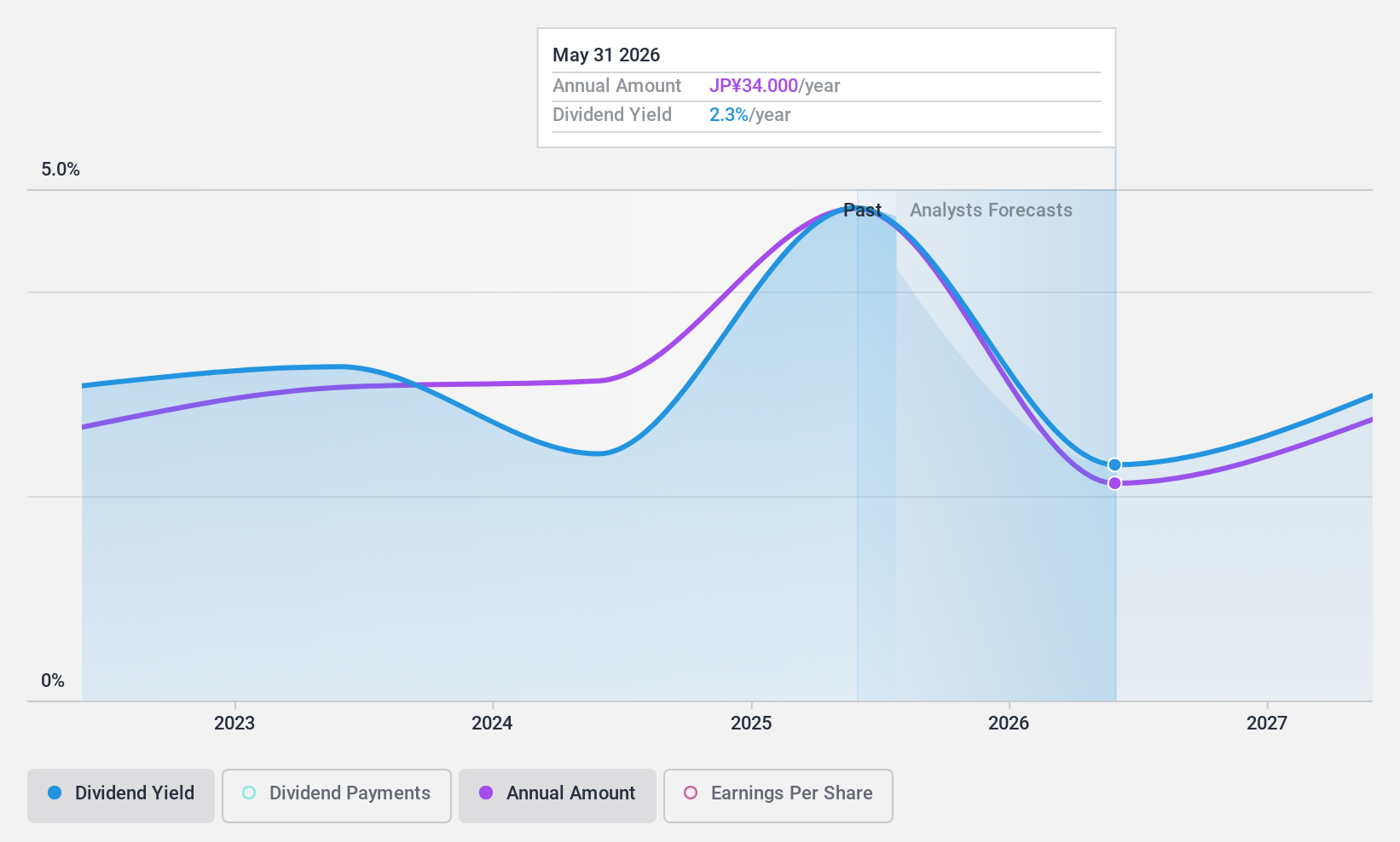

Bewith (TSE:9216)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Bewith, Inc. operates contact and call centers and offers BPO services using digital technologies in Japan, with a market cap of ¥21.16 billion.

Operations: Bewith, Inc.'s revenue segments include contact and call center operations and BPO services in Japan.

Dividend Yield: 5.1%

Bewith's dividend yield of 5.13% ranks in the top 25% among Japanese stocks, supported by a payout ratio of 51.9% and cash flow coverage at 70.6%. Although dividends have been stable and growing, they have only been paid for three years, indicating limited history. Recent guidance revisions with lowered earnings forecasts highlight potential challenges due to weak sales and high operating costs from prior growth investments, which could impact future dividend sustainability.

- Get an in-depth perspective on Bewith's performance by reading our dividend report here.

- Upon reviewing our latest valuation report, Bewith's share price might be too pessimistic.

Turning Ideas Into Actions

- Click here to access our complete index of 1964 Top Dividend Stocks.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Bewith might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:9216

Bewith

Provides contact/call centers and BPO services utilizing digital technologies in Japan.

Excellent balance sheet, good value and pays a dividend.

Market Insights

Community Narratives