The Market Lifts COFCO Joycome Foods Limited (HKG:1610) Shares 25% But It Can Do More

COFCO Joycome Foods Limited (HKG:1610) shares have had a really impressive month, gaining 25% after a shaky period beforehand. Not all shareholders will be feeling jubilant, since the share price is still down a very disappointing 10% in the last twelve months.

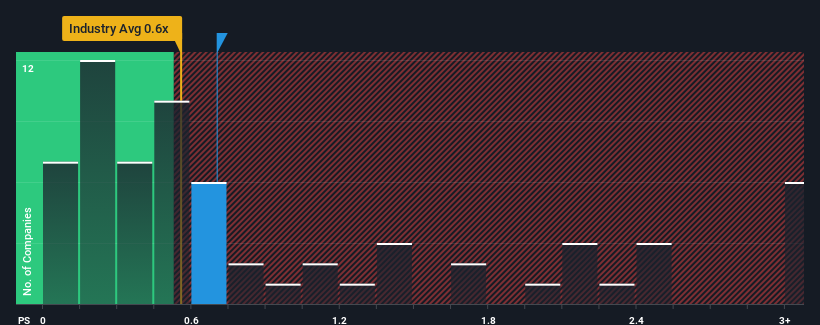

In spite of the firm bounce in price, you could still be forgiven for feeling indifferent about COFCO Joycome Foods' P/S ratio of 0.7x, since the median price-to-sales (or "P/S") ratio for the Food industry in Hong Kong is also close to 0.6x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

Check out our latest analysis for COFCO Joycome Foods

What Does COFCO Joycome Foods' Recent Performance Look Like?

While the industry has experienced revenue growth lately, COFCO Joycome Foods' revenue has gone into reverse gear, which is not great. It might be that many expect the dour revenue performance to strengthen positively, which has kept the P/S from falling. However, if this isn't the case, investors might get caught out paying too much for the stock.

Want the full picture on analyst estimates for the company? Then our free report on COFCO Joycome Foods will help you uncover what's on the horizon.Do Revenue Forecasts Match The P/S Ratio?

COFCO Joycome Foods' P/S ratio would be typical for a company that's only expected to deliver moderate growth, and importantly, perform in line with the industry.

Retrospectively, the last year delivered a frustrating 10% decrease to the company's top line. This means it has also seen a slide in revenue over the longer-term as revenue is down 39% in total over the last three years. Therefore, it's fair to say the revenue growth recently has been undesirable for the company.

Shifting to the future, estimates from the six analysts covering the company suggest revenue should grow by 10.0% per year over the next three years. That's shaping up to be materially higher than the 5.1% each year growth forecast for the broader industry.

With this in consideration, we find it intriguing that COFCO Joycome Foods' P/S is closely matching its industry peers. Apparently some shareholders are skeptical of the forecasts and have been accepting lower selling prices.

What Does COFCO Joycome Foods' P/S Mean For Investors?

COFCO Joycome Foods' stock has a lot of momentum behind it lately, which has brought its P/S level with the rest of the industry. We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

We've established that COFCO Joycome Foods currently trades on a lower than expected P/S since its forecasted revenue growth is higher than the wider industry. There could be some risks that the market is pricing in, which is preventing the P/S ratio from matching the positive outlook. This uncertainty seems to be reflected in the share price which, while stable, could be higher given the revenue forecasts.

A lot of potential risks can sit within a company's balance sheet. You can assess many of the main risks through our free balance sheet analysis for COFCO Joycome Foods with six simple checks.

If these risks are making you reconsider your opinion on COFCO Joycome Foods, explore our interactive list of high quality stocks to get an idea of what else is out there.

If you're looking to trade COFCO Joycome Foods, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1610

COFCO Joycome Foods

An investment holding company, engages in the production and sales of hog, and livestock slaughtering businesses in Mainland China.

Fair value with moderate growth potential.

Market Insights

Community Narratives