First Pacific Company Limited's (HKG:142) Prospects Need A Boost To Lift Shares

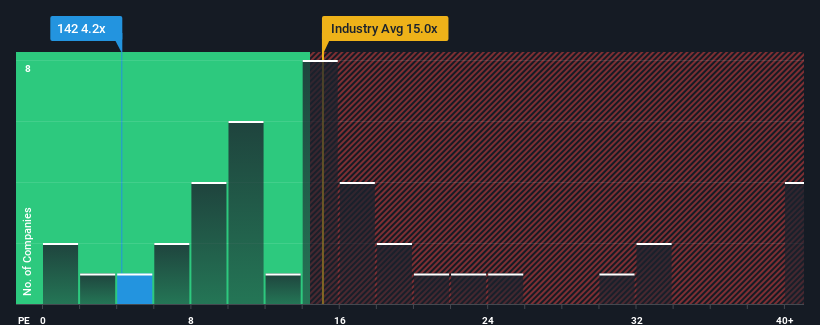

With a price-to-earnings (or "P/E") ratio of 4.2x First Pacific Company Limited (HKG:142) may be sending very bullish signals at the moment, given that almost half of all companies in Hong Kong have P/E ratios greater than 10x and even P/E's higher than 19x are not unusual. However, the P/E might be quite low for a reason and it requires further investigation to determine if it's justified.

First Pacific certainly has been doing a good job lately as it's been growing earnings more than most other companies. One possibility is that the P/E is low because investors think this strong earnings performance might be less impressive moving forward. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

Check out our latest analysis for First Pacific

How Is First Pacific's Growth Trending?

There's an inherent assumption that a company should far underperform the market for P/E ratios like First Pacific's to be considered reasonable.

If we review the last year of earnings growth, the company posted a terrific increase of 29%. The strong recent performance means it was also able to grow EPS by 287% in total over the last three years. Therefore, it's fair to say the earnings growth recently has been superb for the company.

Turning to the outlook, the next three years should generate growth of 13% per year as estimated by the only analyst watching the company. Meanwhile, the rest of the market is forecast to expand by 16% per year, which is noticeably more attractive.

With this information, we can see why First Pacific is trading at a P/E lower than the market. It seems most investors are expecting to see limited future growth and are only willing to pay a reduced amount for the stock.

The Key Takeaway

While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

We've established that First Pacific maintains its low P/E on the weakness of its forecast growth being lower than the wider market, as expected. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

Don't forget that there may be other risks. For instance, we've identified 2 warning signs for First Pacific (1 shouldn't be ignored) you should be aware of.

If P/E ratios interest you, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:142

First Pacific

An investment holding company, engages in the consumer food products, telecommunications, infrastructure, and natural resources businesses in the Philippines, Indonesia, Singapore, the Middle East, Africa, and internationally.

Undervalued average dividend payer.