- Hong Kong

- /

- Healthcare Services

- /

- SEHK:2522

SEHK Value Stock Estimates For October 2024

Reviewed by Simply Wall St

Amid escalating geopolitical tensions in the Middle East and fluctuating global markets, Hong Kong's Hang Seng Index has experienced a notable climb, gaining 10.2% recently despite broader economic uncertainties. In this environment, identifying undervalued stocks could present opportunities for investors seeking value plays within the market; these stocks often exhibit strong fundamentals or potential for growth that is not yet reflected in their current valuations.

Top 10 Undervalued Stocks Based On Cash Flows In Hong Kong

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| BYD Electronic (International) (SEHK:285) | HK$34.05 | HK$64.15 | 46.9% |

| MicroPort NeuroScientific (SEHK:2172) | HK$9.97 | HK$18.90 | 47.2% |

| China Ruyi Holdings (SEHK:136) | HK$2.24 | HK$4.14 | 45.9% |

| Shanghai INT Medical Instruments (SEHK:1501) | HK$30.00 | HK$56.20 | 46.6% |

| Semiconductor Manufacturing International (SEHK:981) | HK$27.35 | HK$52.71 | 48.1% |

| COSCO SHIPPING Energy Transportation (SEHK:1138) | HK$10.14 | HK$19.03 | 46.7% |

| Q Technology (Group) (SEHK:1478) | HK$5.75 | HK$11.23 | 48.8% |

| Zylox-Tonbridge Medical Technology (SEHK:2190) | HK$13.40 | HK$25.84 | 48.2% |

| Nayuki Holdings (SEHK:2150) | HK$1.83 | HK$3.37 | 45.6% |

| Digital China Holdings (SEHK:861) | HK$3.01 | HK$5.86 | 48.6% |

Let's review some notable picks from our screened stocks.

COSCO SHIPPING Energy Transportation (SEHK:1138)

Overview: COSCO SHIPPING Energy Transportation Co., Ltd. is an investment holding company involved in the transportation of oil, liquefied natural gas (LNG), and chemicals both domestically along the coast of China and internationally, with a market cap of HK$73.47 billion.

Operations: The company generates revenue through the transportation of oil, liquefied natural gas (LNG), and chemicals across domestic and international routes.

Estimated Discount To Fair Value: 46.7%

COSCO SHIPPING Energy Transportation is trading at HK$10.14, significantly below its estimated fair value of HK$19.03, indicating potential undervaluation based on cash flows. Despite high debt levels and a dividend not well covered by free cash flows, earnings are forecast to grow 22% annually, outpacing the Hong Kong market's 12.4%. Recent earnings show stable revenue but a slight decline in net income compared to last year.

- Our expertly prepared growth report on COSCO SHIPPING Energy Transportation implies its future financial outlook may be stronger than recent results.

- Unlock comprehensive insights into our analysis of COSCO SHIPPING Energy Transportation stock in this financial health report.

XD (SEHK:2400)

Overview: XD Inc., an investment holding company, focuses on developing, publishing, operating, and distributing mobile and web games both in Mainland China and internationally with a market capitalization of HK$13.28 billion.

Operations: The company's revenue is primarily derived from its Game segment, which generated CN¥2.43 billion, and the TapTap Platform segment, contributing CN¥1.43 billion.

Estimated Discount To Fair Value: 42%

XD Inc. is trading at HK$27.55, well below its estimated fair value of HK$47.51, highlighting potential undervaluation based on cash flows. The company reported strong earnings growth with net income rising to CNY 205.1 million for the first half of 2024, driven by new game launches and increased information services revenue from TapTap PRC. However, shareholder dilution over the past year remains a concern despite robust profit forecasts exceeding market expectations in Hong Kong.

- Our growth report here indicates XD may be poised for an improving outlook.

- Click here to discover the nuances of XD with our detailed financial health report.

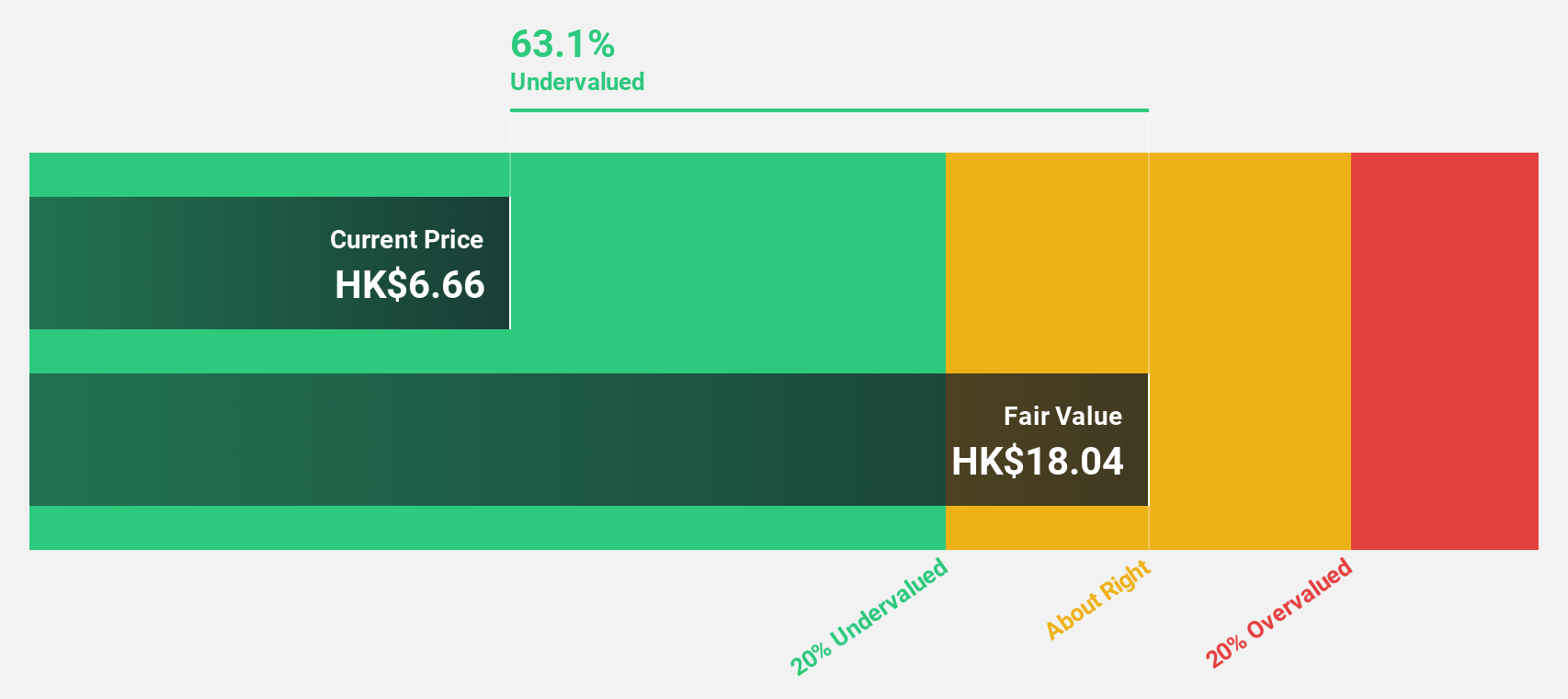

Jiangxi Rimag Group (SEHK:2522)

Overview: Jiangxi Rimag Group Co., Ltd. operates medical imaging centers in China and has a market cap of HK$12.10 billion.

Operations: The company generates revenue from its medical labs and research segment, amounting to CN¥812.85 million.

Estimated Discount To Fair Value: 31.1%

Jiangxi Rimag Group is trading at HK$33.95, significantly below its estimated fair value of HK$49.31, suggesting it may be undervalued based on cash flows. Despite a decline in sales to CNY 413.71 million and net income to CNY 3.84 million for the first half of 2024, earnings are projected to grow substantially by 71.8% annually over the next three years, outpacing the Hong Kong market's growth rate and indicating strong future potential despite current challenges in profit margins and return on equity forecasts.

- The growth report we've compiled suggests that Jiangxi Rimag Group's future prospects could be on the up.

- Dive into the specifics of Jiangxi Rimag Group here with our thorough financial health report.

Where To Now?

- Explore the 42 names from our Undervalued SEHK Stocks Based On Cash Flows screener here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:2522

Reasonable growth potential with adequate balance sheet.