Advertisement

- Hong Kong

- /

- Capital Markets

- /

- SEHK:430

Don't Race Out To Buy Oriental Explorer Holdings Limited (HKG:430) Just Because It's Going Ex-Dividend

Readers hoping to buy Oriental Explorer Holdings Limited (HKG:430) for its dividend will need to make their move shortly, as the stock is about to trade ex-dividend. The ex-dividend date is usually set to be two business days before the record date, which is the cut-off date on which you must be present on the company's books as a shareholder in order to receive the dividend. The ex-dividend date is important as the process of settlement involves at least two full business days. So if you miss that date, you would not show up on the company's books on the record date. Accordingly, Oriental Explorer Holdings investors that purchase the stock on or after the 30th of May will not receive the dividend, which will be paid on the 26th of June.

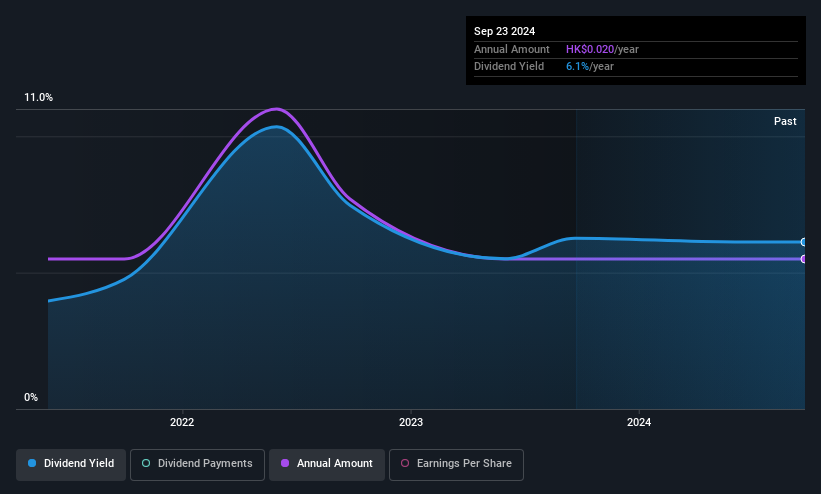

The company's next dividend payment will be HK$0.006 per share. Last year, in total, the company distributed HK$0.014 to shareholders. Last year's total dividend payments show that Oriental Explorer Holdings has a trailing yield of 3.6% on the current share price of HK$0.39. Dividends are a major contributor to investment returns for long term holders, but only if the dividend continues to be paid. We need to see whether the dividend is covered by earnings and if it's growing.

We've discovered 4 warning signs about Oriental Explorer Holdings. View them for free.Dividends are typically paid out of company income, so if a company pays out more than it earned, its dividend is usually at a higher risk of being cut. Oriental Explorer Holdings reported a loss last year, so it's not great to see that it has continued paying a dividend.

Check out our latest analysis for Oriental Explorer Holdings

Click here to see how much of its profit Oriental Explorer Holdings paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

Businesses with shrinking earnings are tricky from a dividend perspective. Investors love dividends, so if earnings fall and the dividend is reduced, expect a stock to be sold off heavily at the same time. Oriental Explorer Holdings reported a loss last year, and the general trend suggests its earnings have also been declining in recent years, making us wonder if the dividend is at risk.

Another key way to measure a company's dividend prospects is by measuring its historical rate of dividend growth. Oriental Explorer Holdings has seen its dividend decline 8.5% per annum on average over the past four years, which is not great to see. While it's not great that earnings and dividends per share have fallen in recent years, we're encouraged by the fact that management has trimmed the dividend rather than risk over-committing the company in a risky attempt to maintain yields to shareholders.

Get our latest analysis on Oriental Explorer Holdings's balance sheet health here.

The Bottom Line

Has Oriental Explorer Holdings got what it takes to maintain its dividend payments? It's hard to get past the idea of Oriental Explorer Holdings paying a dividend despite reporting a loss over the past year - especially when the general trend in its earnings also looks to be negative. All things considered, we're not optimistic about its dividend prospects, and would be inclined to leave it on the shelf for now.

Having said that, if you're looking at this stock without much concern for the dividend, you should still be familiar of the risks involved with Oriental Explorer Holdings. For instance, we've identified 4 warning signs for Oriental Explorer Holdings (1 doesn't sit too well with us) you should be aware of.

If you're in the market for strong dividend payers, we recommend checking our selection of top dividend stocks.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:430

Oriental Explorer Holdings

An investment holding company, engages in the property investment activities in Hong Kong and Mainland China.

Slight with imperfect balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|27.5% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|4.2% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.7% undervalued

KA

Community Contributor