- Hong Kong

- /

- Consumer Services

- /

- SEHK:1830

Perfect Medical Health Management (HKG:1830) Will Pay A Smaller Dividend Than Last Year

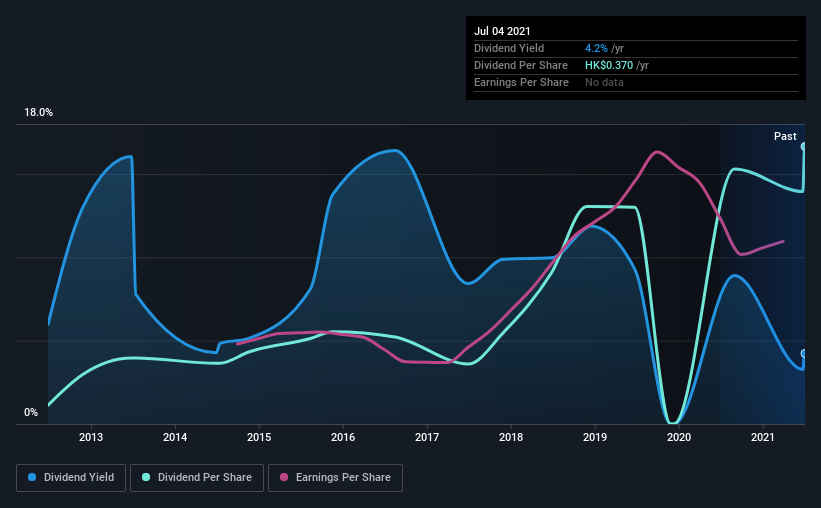

Perfect Medical Health Management Limited (HKG:1830) has announced it will be reducing its dividend payable on the 15th of October to HK$0.25. The yield is still above the industry average at 4.3%.

While the dividend yield is important for income investors, it is also important to consider any large share price moves, as this will generally outweigh any gains from distributions. Investors will be pleased to see that Perfect Medical Health Management's stock price has increased by 85% in the last 3 months, which is good for shareholders and can also explain a decrease in the dividend yield.

See our latest analysis for Perfect Medical Health Management

Perfect Medical Health Management Doesn't Earn Enough To Cover Its Payments

We like to see robust dividend yields, but that doesn't matter if the payment isn't sustainable. Based on the last payment, Perfect Medical Health Management's profits didn't cover the dividend, but the company was generating enough cash instead. Given that the dividend is a cash outflow, we think that cash is more important than accounting measures of profit when assessing the dividend, so this is a mitigating factor.

Earnings per share could rise by 16.1% over the next year if things go the same way as they have for the last few years. Assuming the dividend continues along recent trends, we think the payout ratio could reach 162%, which probably can't continue without starting to put some pressure on the balance sheet.

Perfect Medical Health Management's Dividend Has Lacked Consistency

Perfect Medical Health Management has been paying dividends for a while, but the track record isn't stellar. This suggests that the dividend might not be the most reliable. The dividend has gone from HK$0.025 in 2012 to the most recent annual payment of HK$0.37. This works out to be a compound annual growth rate (CAGR) of approximately 35% a year over that time. Dividends have grown rapidly over this time, but with cuts in the past we are not certain that this stock will be a reliable source of income in the future.

Dividend Growth Could Be Constrained

Growing earnings per share could be a mitigating factor when considering the past fluctuations in the dividend. Perfect Medical Health Management has impressed us by growing EPS at 16% per year over the past five years. Although per-share earnings are growing at a credible rate, the massive payout ratio may limit growth in the company's future dividend payments.

In Summary

Overall, the dividend looks like it may have been a bit high, which explains why it has now been cut. The payments haven't been particularly stable and we don't see huge growth potential, but with the dividend well covered by cash flows it could prove to be reliable over the short term. This company is not in the top tier of income providing stocks.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. For example, we've picked out 3 warning signs for Perfect Medical Health Management that investors should know about before committing capital to this stock. If you are a dividend investor, you might also want to look at our curated list of high performing dividend stock.

When trading stocks or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

If you're looking to trade Perfect Medical Health Management, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SEHK:1830

Perfect Medical Health Management

An investment holding company, engages in the provision of medical, aesthetic medical, and beauty and well services in Hong Kong, the People’s Republic of China, Macau, Australia, and Singapore.

Flawless balance sheet and undervalued.

Market Insights

Community Narratives