Shareholders Will Probably Hold Off On Increasing Amuse Group Holding Limited's (HKG:8545) CEO Compensation For The Time Being

Key Insights

- Amuse Group Holding's Annual General Meeting to take place on 14th of August

- Salary of HK$3.94m is part of CEO Wai Keung Li's total remuneration

- The total compensation is 288% higher than the average for the industry

- Amuse Group Holding's EPS declined by 7.5% over the past three years while total shareholder return over the past three years was 37%

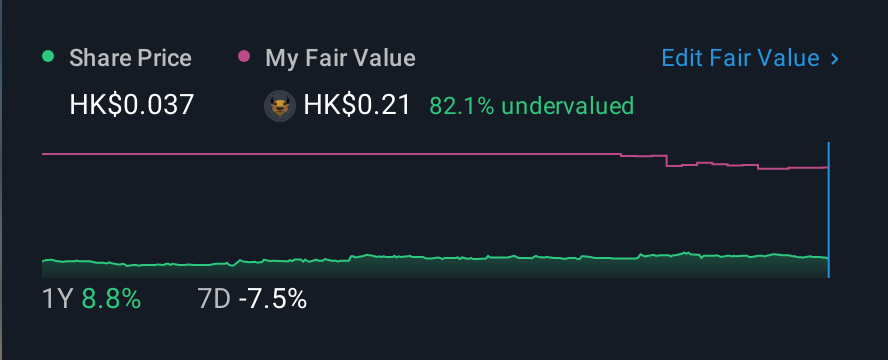

The share price of Amuse Group Holding Limited (HKG:8545) has increased significantly over the past few years. However, the earnings growth has not kept up with the share price momentum, suggesting that some other factors may be driving the price direction. Some of these issues will occupy shareholders' minds as the AGM rolls around on 14th of August. It would also be an opportunity for them to influence management through exercising their voting power on company resolutions, including CEO and executive remuneration, which could impact on firm performance in the future. From what we gathered, we think shareholders should be wary of raising CEO compensation until the company shows some marked improvement.

View our latest analysis for Amuse Group Holding

Comparing Amuse Group Holding Limited's CEO Compensation With The Industry

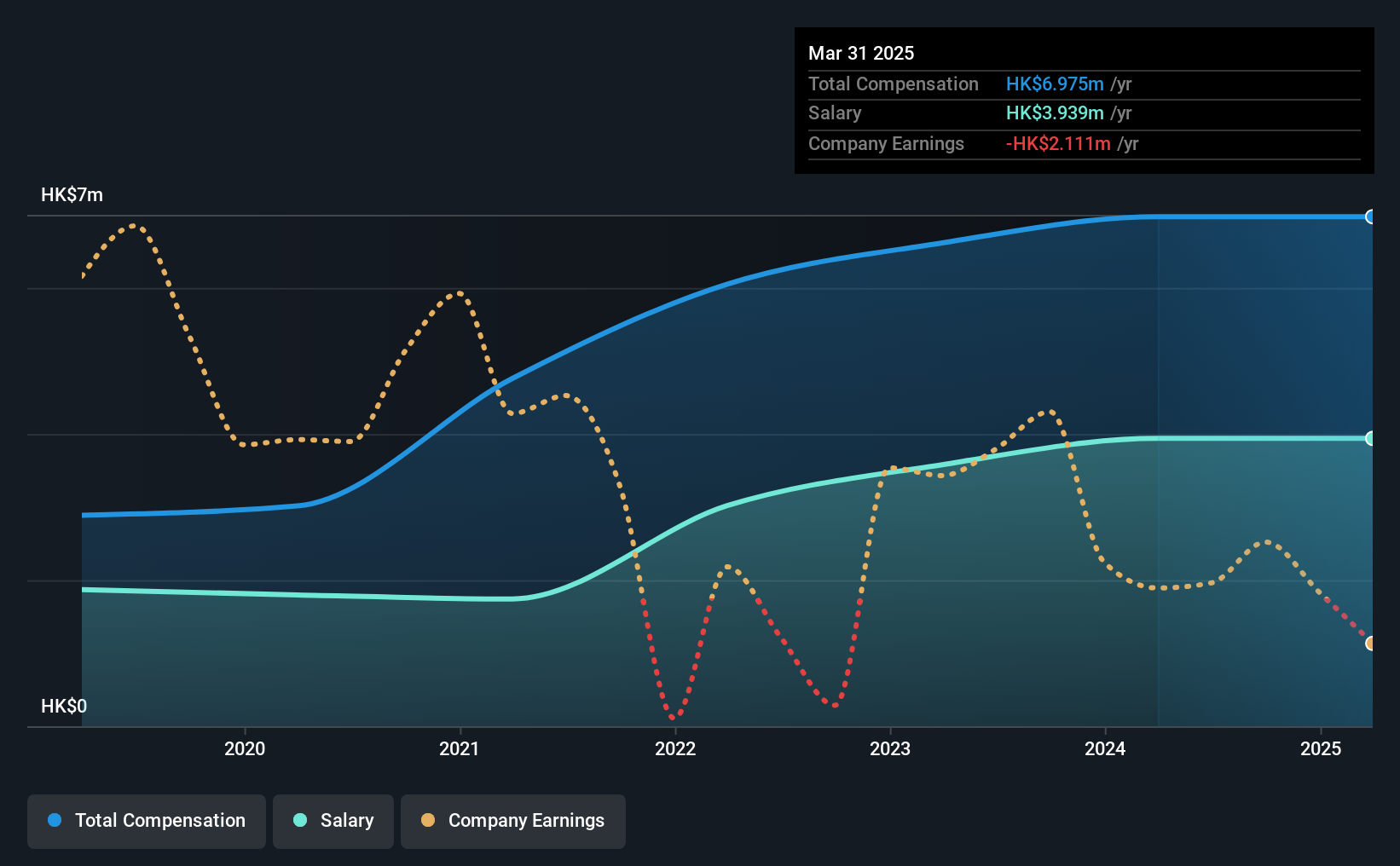

At the time of writing, our data shows that Amuse Group Holding Limited has a market capitalization of HK$57m, and reported total annual CEO compensation of HK$7.0m for the year to March 2025. This was the same amount the CEO received in the prior year. We note that the salary of HK$3.94m makes up a sizeable portion of the total compensation received by the CEO.

In comparison with other companies in the Hong Kong Leisure industry with market capitalizations under HK$1.6b, the reported median total CEO compensation was HK$1.8m. Hence, we can conclude that Wai Keung Li is remunerated higher than the industry median. What's more, Wai Keung Li holds HK$9.8m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2025 | 2024 | Proportion (2025) |

| Salary | HK$3.9m | HK$3.9m | 56% |

| Other | HK$3.0m | HK$3.0m | 44% |

| Total Compensation | HK$7.0m | HK$7.0m | 100% |

Speaking on an industry level, nearly 91% of total compensation represents salary, while the remainder of 9% is other remuneration. It's interesting to note that Amuse Group Holding allocates a smaller portion of compensation to salary in comparison to the broader industry. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

A Look at Amuse Group Holding Limited's Growth Numbers

Over the last three years, Amuse Group Holding Limited has shrunk its earnings per share by 7.5% per year. In the last year, its revenue is down 35%.

Overall this is not a very positive result for shareholders. This is compounded by the fact revenue is actually down on last year. These factors suggest that the business performance wouldn't really justify a high pay packet for the CEO. While we don't have analyst forecasts for the company, shareholders might want to examine this detailed historical graph of earnings, revenue and cash flow.

Has Amuse Group Holding Limited Been A Good Investment?

Most shareholders would probably be pleased with Amuse Group Holding Limited for providing a total return of 37% over three years. So they may not be at all concerned if the CEO were to be paid more than is normal for companies around the same size.

To Conclude...

Although shareholders would be quite happy with the returns they have earned on their initial investment, earnings have failed to grow and this could mean returns may be hard to keep up. The upcoming AGM will provide shareholders the opportunity to revisit the company’s remuneration policies and evaluate if the board’s judgement and decision-making is aligned with that of the company’s shareholders.

While it is important to pay attention to CEO remuneration, investors should also consider other elements of the business. That's why we did some digging and identified 2 warning signs for Amuse Group Holding that investors should think about before committing capital to this stock.

Important note: Amuse Group Holding is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:8545

Amuse Group Holding

An investment holding company, designs, markets, distributes, and sells toys and related products in Hong Kong, Japan, the United States, the People’s Republic of China, Taiwan, South Korea, Germany, Australia, Italy, France, and internationally.

Flawless balance sheet and fair value.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

A case for USD $14.81 per share based on book value. Be warned, this is a micro-cap dependent on a single mine.

Occidental Petroleum to Become Fairly Priced at $68.29 According to Future Projections

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)