- Hong Kong

- /

- Consumer Durables

- /

- SEHK:1418

Sinomax Group's (HKG:1418) Shareholders Will Receive A Smaller Dividend Than Last Year

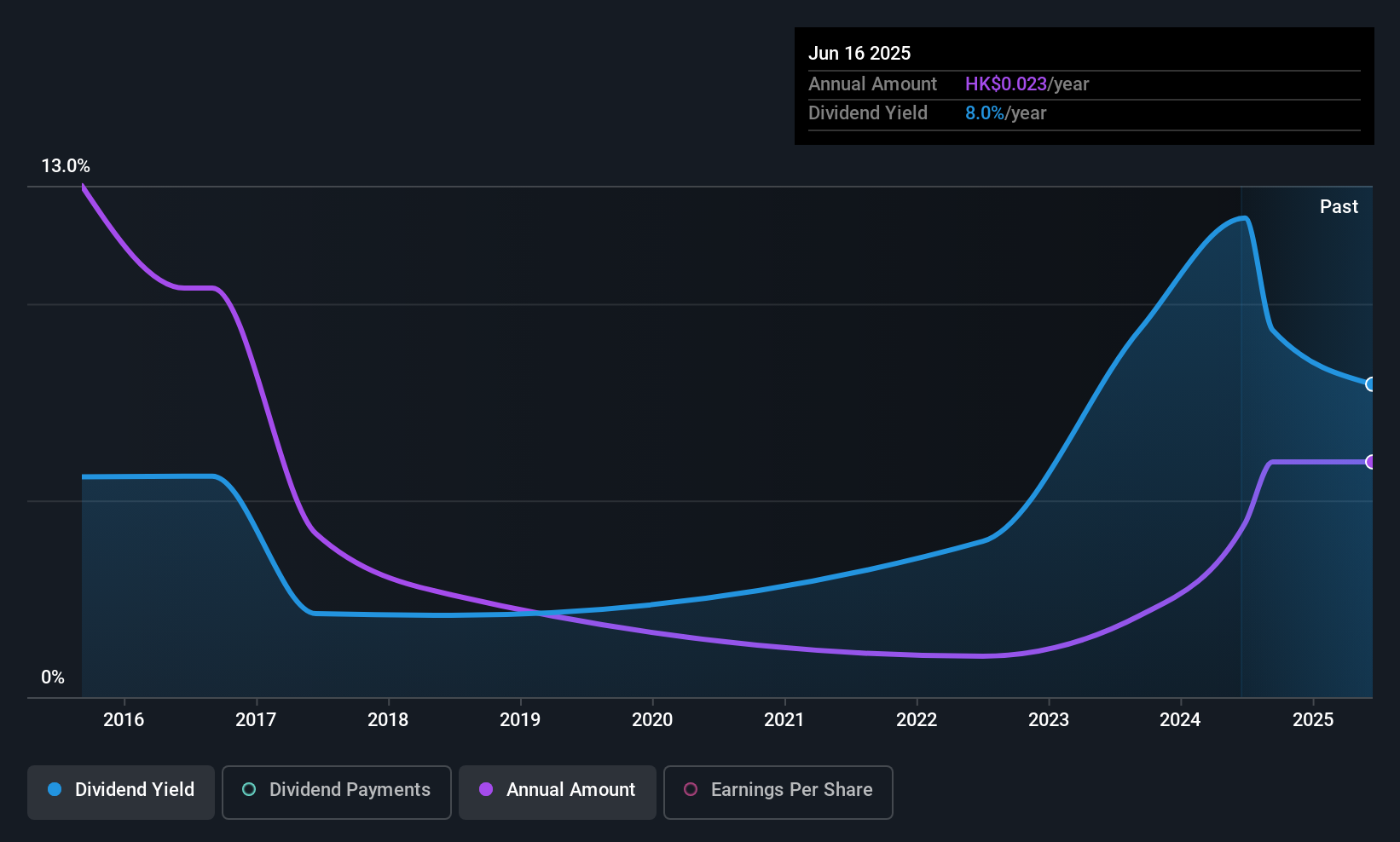

Sinomax Group Limited (HKG:1418) is reducing its dividend to HK$0.005 on the 8th of Octoberwhich is 50% less than last year's comparable payment of HK$0.01. This means the annual payment is 9.3% of the current stock price, which is above the average for the industry.

Sinomax Group's Payment Could Potentially Have Solid Earnings Coverage

We like to see robust dividend yields, but that doesn't matter if the payment isn't sustainable. However, Sinomax Group's earnings easily cover the dividend. This means that most of its earnings are being retained to grow the business.

Looking forward, earnings per share could rise by 49.1% over the next year if the trend from the last few years continues. If the dividend continues along recent trends, we estimate the payout ratio will be 19%, which is in the range that makes us comfortable with the sustainability of the dividend.

Check out our latest analysis for Sinomax Group

Dividend Volatility

While the company has been paying a dividend for a long time, it has cut the dividend at least once in the last 10 years. The annual payment during the last 10 years was HK$0.02 in 2015, and the most recent fiscal year payment was HK$0.023. This works out to be a compound annual growth rate (CAGR) of approximately 1.4% a year over that time. It's encouraging to see some dividend growth, but the dividend has been cut at least once, and the size of the cut would eliminate most of the growth anyway, which makes this less attractive as an income investment.

The Dividend Looks Likely To Grow

With a relatively unstable dividend, it's even more important to see if earnings per share is growing. It's encouraging to see that Sinomax Group has been growing its earnings per share at 49% a year over the past five years. Rapid earnings growth and a low payout ratio suggest this company has been effectively reinvesting in its business. Should that continue, this company could have a bright future.

Sinomax Group Looks Like A Great Dividend Stock

Overall, we think that Sinomax Group could be a great option for a dividend investment, although we would have preferred if the dividend wasn't cut this year. By reducing the dividend, pressure will be taken off the balance sheet, which could help the dividend to be consistent in the future. All in all, this checks a lot of the boxes we look for when choosing an income stock.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. However, there are other things to consider for investors when analysing stock performance. Taking the debate a bit further, we've identified 2 warning signs for Sinomax Group that investors need to be conscious of moving forward. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1418

Sinomax Group

An investment holding company, develops, manufactures, and sells health and wellness products.

Flawless balance sheet average dividend payer.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Butler National (Buks) outperforms.

A tech powerhouse quietly powering the world’s AI infrastructure.

Keppel DC REIT (SGX: AJBU) is a resilient gem in the data center space.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)