Advertisement

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Luxxu Group Limited (HKG:1327) does use debt in its business. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is Luxxu Group's Debt?

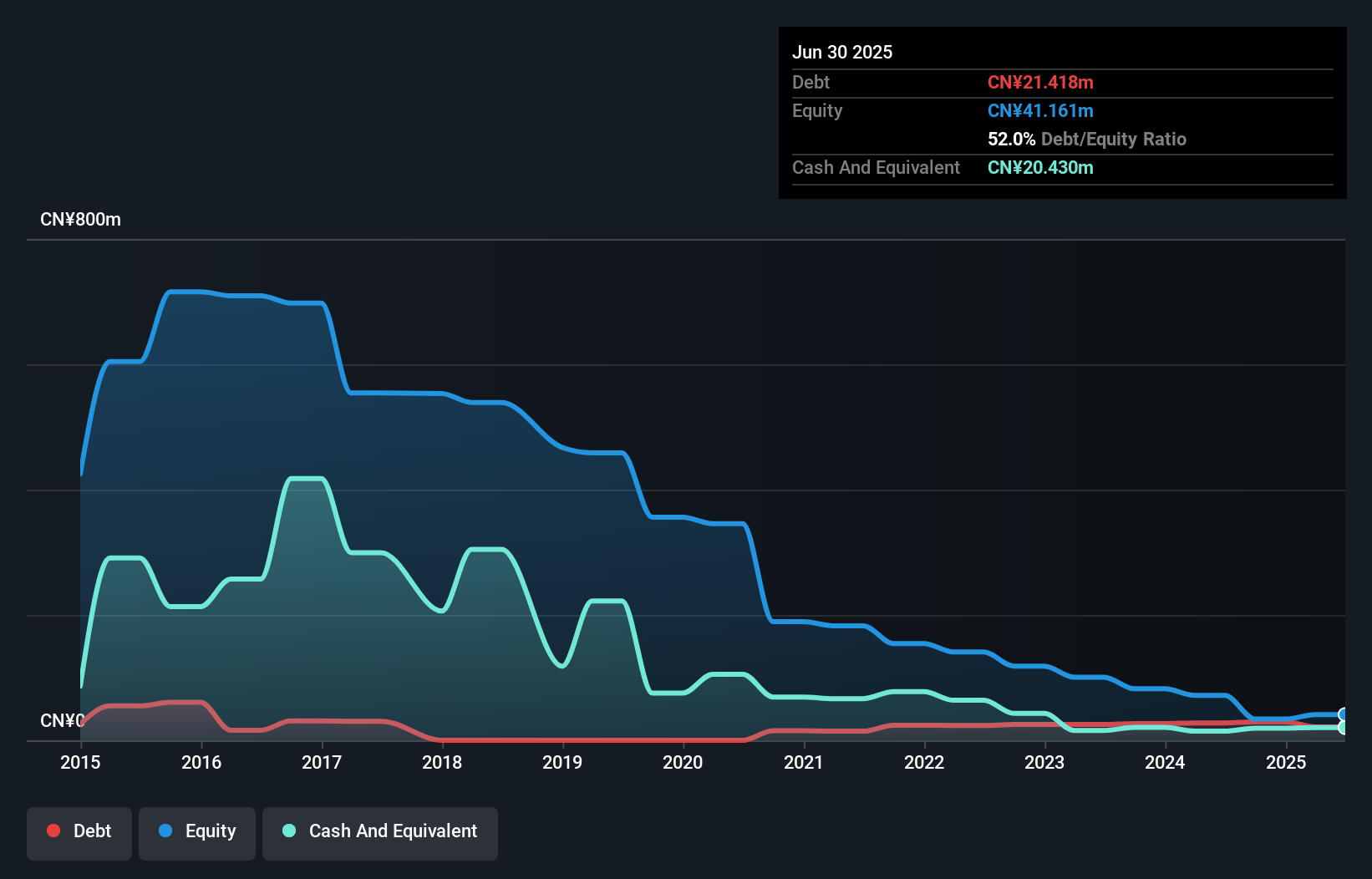

The image below, which you can click on for greater detail, shows that Luxxu Group had debt of CN¥21.4m at the end of June 2025, a reduction from CN¥27.8m over a year. However, because it has a cash reserve of CN¥20.4m, its net debt is less, at about CN¥988.0k.

How Healthy Is Luxxu Group's Balance Sheet?

The latest balance sheet data shows that Luxxu Group had liabilities of CN¥3.90m due within a year, and liabilities of CN¥24.7m falling due after that. Offsetting this, it had CN¥20.4m in cash and CN¥11.7m in receivables that were due within 12 months. So it can boast CN¥3.50m more liquid assets than total liabilities.

This surplus suggests that Luxxu Group has a conservative balance sheet, and could probably eliminate its debt without much difficulty. Carrying virtually no net debt, Luxxu Group has a very light debt load indeed. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since Luxxu Group will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

See our latest analysis for Luxxu Group

In the last year Luxxu Group wasn't profitable at an EBIT level, but managed to grow its revenue by 8.2%, to CN¥29m. We usually like to see faster growth from unprofitable companies, but each to their own.

Caveat Emptor

Importantly, Luxxu Group had an earnings before interest and tax (EBIT) loss over the last year. Indeed, it lost a very considerable CN¥51m at the EBIT level. On a more positive note, the company does have liquid assets, so it has a bit of time to improve its operations before the debt becomes an acute problem. But a profit would do more to inspire us to research the business more closely. This one is a bit too risky for our liking. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. These risks can be hard to spot. Every company has them, and we've spotted 4 warning signs for Luxxu Group (of which 1 doesn't sit too well with us!) you should know about.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1327

Luxxu Group

An investment holding company, manufactures, trades in, retails, and sells watches and jewelries in the People’s Republic of China and Hong Kong.

Excellent balance sheet with slight risk.

Market Insights

Advertisement

Community Narratives

100% Patient Improvement in trial puts this $16M Biotech on the radar

Fair Value US$5.30|74.9% undervalued

JO

Community Contributor

PayPal's Future Growth Through Venmo and Merchant Solutions

Fair Value US$105.25|33.8% undervalued

ZW

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$26.54|6.3% overvalued

BL

Community Contributor