3 SEHK Growth Companies With High Insider Ownership Expecting Up To 22% Profit Growth

Reviewed by Simply Wall St

The Hong Kong market has been navigating a challenging landscape, with the Hang Seng Index recently experiencing a slight decline amid global economic uncertainties. Despite this, opportunities remain for discerning investors, particularly in growth companies with high insider ownership. In such an environment, stocks with substantial insider ownership can be particularly appealing as they often indicate strong confidence from those closest to the company's operations. This article will explore three SEHK-listed growth companies that boast significant insider stakes and are projecting profit growth of up to 22%.

Top 10 Growth Companies With High Insider Ownership In Hong Kong

| Name | Insider Ownership | Earnings Growth |

| iDreamSky Technology Holdings (SEHK:1119) | 18.8% | 104.1% |

| Pacific Textiles Holdings (SEHK:1382) | 11.2% | 37.7% |

| Tian Tu Capital (SEHK:1973) | 34% | 70.5% |

| Adicon Holdings (SEHK:9860) | 22.4% | 28.3% |

| Biocytogen Pharmaceuticals (Beijing) (SEHK:2315) | 13.9% | 100.1% |

| Zhejiang Leapmotor Technology (SEHK:9863) | 15% | 74.5% |

| DPC Dash (SEHK:1405) | 38.2% | 91.4% |

| Zylox-Tonbridge Medical Technology (SEHK:2190) | 18.7% | 79.3% |

| Ocumension Therapeutics (SEHK:1477) | 23.3% | 93.7% |

| Beijing Airdoc Technology (SEHK:2251) | 28.6% | 83.9% |

Here we highlight a subset of our preferred stocks from the screener.

Kuaishou Technology (SEHK:1024)

Simply Wall St Growth Rating: ★★★★★☆

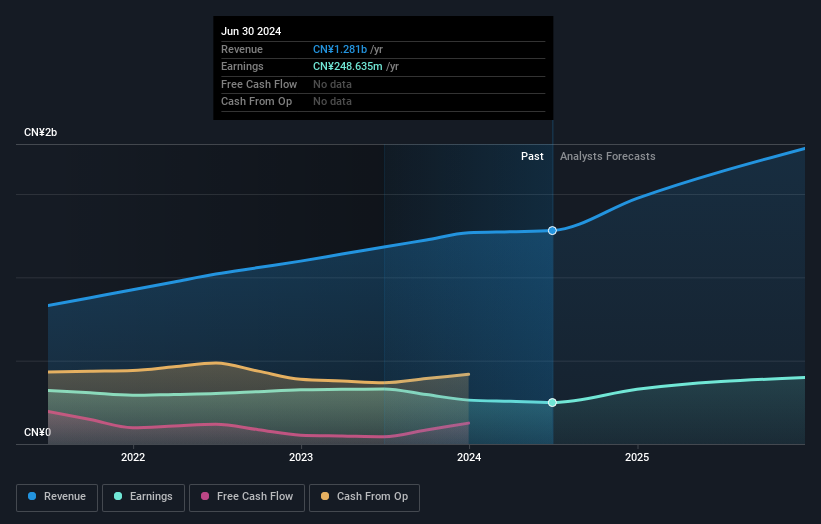

Overview: Kuaishou Technology, an investment holding company with a market cap of HK$187.10 billion, offers live streaming, online marketing, and other services in the People’s Republic of China.

Operations: The company generates revenue primarily from its domestic operations (CN¥114.72 billion) and overseas activities (CN¥2.94 billion).

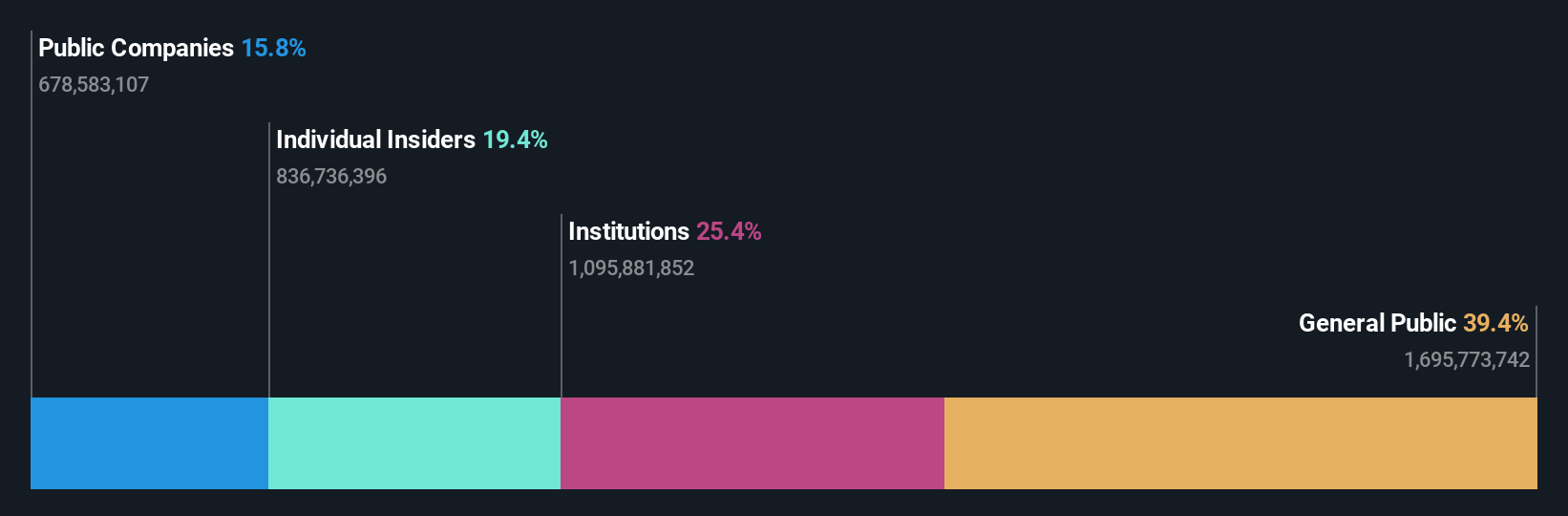

Insider Ownership: 19.2%

Earnings Growth Forecast: 22.5% p.a.

Kuaishou Technology, a growth company with high insider ownership, has shown significant potential. Recently becoming profitable and trading at 61.9% below its estimated fair value, its earnings are forecast to grow 22.5% annually over the next three years, outpacing market averages. The company's Kling AI video generation model has seen substantial upgrades and strong user engagement, enhancing Kuaishou's commercial ecosystem and driving revenue growth faster than the Hong Kong market rate of 7.4%.

- Delve into the full analysis future growth report here for a deeper understanding of Kuaishou Technology.

- Insights from our recent valuation report point to the potential undervaluation of Kuaishou Technology shares in the market.

LifeTech Scientific (SEHK:1302)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: LifeTech Scientific Corporation develops, manufactures, and trades interventional medical devices for cardiovascular and peripheral vascular diseases globally, with a market cap of HK$7.18 billion.

Operations: The company's revenue segments include CN¥495.67 million from the Structural Heart Diseases Business, CN¥707.11 million from the Peripheral Vascular Diseases Business, and CN¥64.40 million from the Cardiac Pacing and Electrophysiology Business.

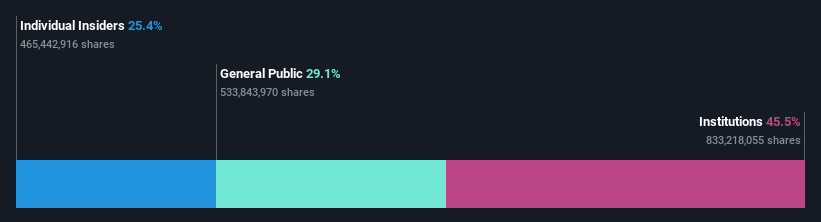

Insider Ownership: 16%

Earnings Growth Forecast: 20.5% p.a.

LifeTech Scientific, with high insider ownership, shows promising growth prospects. Earnings are forecast to grow 20.55% annually, outpacing the Hong Kong market's 11.3%. Revenue is expected to increase by 16.8% per year. Recent advancements include successful phase II clinical trials for its IBS® Coronary Scaffold, demonstrating safety and efficacy comparable to mainstream stents and enhancing global development potential. Amendments to company bylaws were also approved at the recent AGM on May 27, 2024.

- Take a closer look at LifeTech Scientific's potential here in our earnings growth report.

- Our expertly prepared valuation report LifeTech Scientific implies its share price may be too high.

Techtronic Industries (SEHK:669)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Techtronic Industries Company Limited designs, manufactures, and markets power tools, outdoor power equipment, and floorcare and cleaning products across North America, Europe, and internationally with a market cap of HK$179.40 billion.

Operations: The company's revenue segments include Power Equipment at $12.79 billion and Floorcare & Cleaning at $974.75 million.

Insider Ownership: 25.4%

Earnings Growth Forecast: 14.9% p.a.

Techtronic Industries, with substantial insider ownership, is poised for growth with earnings forecasted to rise 14.93% annually, surpassing the Hong Kong market's 11.3%. Revenue is expected to grow at 8.1% per year. Recent developments include a significant share buyback program aimed at enhancing net asset value and earnings per share, and leadership changes with Steven Richman appointed as CEO following Joseph Galli Jr.'s retirement.

- Get an in-depth perspective on Techtronic Industries' performance by reading our analyst estimates report here.

- Our comprehensive valuation report raises the possibility that Techtronic Industries is priced higher than what may be justified by its financials.

Taking Advantage

- Unlock more gems! Our Fast Growing SEHK Companies With High Insider Ownership screener has unearthed 51 more companies for you to explore.Click here to unveil our expertly curated list of 54 Fast Growing SEHK Companies With High Insider Ownership.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Techtronic Industries might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:669

Techtronic Industries

Engages in the design, manufacture, and marketing of power tools, outdoor power equipment, and floorcare and cleaning products in the North America, Europe, and internationally.

Flawless balance sheet average dividend payer.