Advertisement

These 4 Measures Indicate That Sany Heavy Equipment International Holdings (HKG:631) Is Using Debt Reasonably Well

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Sany Heavy Equipment International Holdings Company Limited (HKG:631) does use debt in its business. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company's debt levels is to consider its cash and debt together.

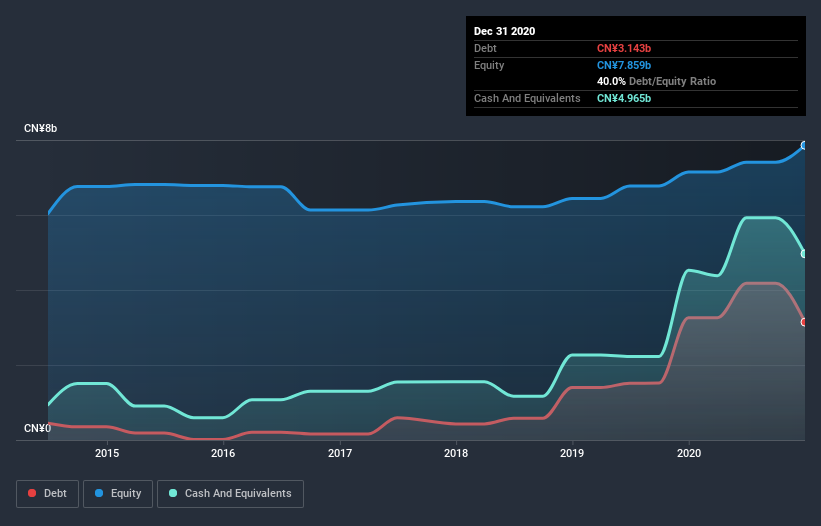

See our latest analysis for Sany Heavy Equipment International Holdings

What Is Sany Heavy Equipment International Holdings's Debt?

The chart below, which you can click on for greater detail, shows that Sany Heavy Equipment International Holdings had CN¥3.14b in debt in December 2020; about the same as the year before. However, it does have CN¥4.97b in cash offsetting this, leading to net cash of CN¥1.82b.

How Strong Is Sany Heavy Equipment International Holdings' Balance Sheet?

We can see from the most recent balance sheet that Sany Heavy Equipment International Holdings had liabilities of CN¥7.94b falling due within a year, and liabilities of CN¥1.67b due beyond that. On the other hand, it had cash of CN¥4.97b and CN¥3.90b worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by CN¥737.7m.

Since publicly traded Sany Heavy Equipment International Holdings shares are worth a total of CN¥24.4b, it seems unlikely that this level of liabilities would be a major threat. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time. Despite its noteworthy liabilities, Sany Heavy Equipment International Holdings boasts net cash, so it's fair to say it does not have a heavy debt load!

On top of that, Sany Heavy Equipment International Holdings grew its EBIT by 41% over the last twelve months, and that growth will make it easier to handle its debt. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Sany Heavy Equipment International Holdings can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. Sany Heavy Equipment International Holdings may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. In the last three years, Sany Heavy Equipment International Holdings's free cash flow amounted to 34% of its EBIT, less than we'd expect. That's not great, when it comes to paying down debt.

Summing up

We could understand if investors are concerned about Sany Heavy Equipment International Holdings's liabilities, but we can be reassured by the fact it has has net cash of CN¥1.82b. And we liked the look of last year's 41% year-on-year EBIT growth. So we don't think Sany Heavy Equipment International Holdings's use of debt is risky. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. Case in point: We've spotted 1 warning sign for Sany Heavy Equipment International Holdings you should be aware of.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

If you’re looking to trade Sany Heavy Equipment International Holdings, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SEHK:631

Sany Heavy Equipment International Holdings

Manufactures and sells mining and logistics equipment, electricity, power station project products, petroleum and new energy manufacturing equipment, spare parts, and related services.

Excellent balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|26.1% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|4.8% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|27.0% undervalued

KA

Community Contributor