Advertisement

- Hong Kong

- /

- Construction

- /

- SEHK:3996

Reassessing China Energy Engineering (SEHK:3996)’s Valuation After Leadership Reshuffle and Chairman Transition

Simply Wall St

Reviewed by Simply Wall St

China Energy Engineering (SEHK:3996) has just entered a leadership reshuffle, with long serving chairman Song Hailiang stepping down. Ni Zhen is temporarily assuming chairman and authorized representative duties while leaving the general manager role.

See our latest analysis for China Energy Engineering.

Despite the leadership reshuffle and upcoming board meeting on governance changes, the latest HK$1.14 share price sits against a solid backdrop. The year to date share price return is 16.33%, and the five year total shareholder return is 72.16%. This suggests long term momentum remains constructive even if near term sentiment is more cautious.

If this leadership change has you reassessing your watchlist, it could be a good moment to scan the market for fast growing stocks with high insider ownership and spot the next potential outperformers.

With shares already delivering strong multi year returns and profits still growing, the key question now is whether China Energy Engineering is trading below its true value or if the market is already pricing in future growth.

Price-to-Earnings of 5.4x: Is it justified?

On a price-to-earnings basis, China Energy Engineering looks inexpensive at 5.4x earnings, especially given the HK$1.14 last close and its solid multi year share gains.

The price-to-earnings multiple compares the current share price with the company’s earnings per share. It is a simple way to gauge how much investors are paying for current profits. For a large, diversified engineering and infrastructure group, this metric is particularly relevant because earnings tend to be cyclical and closely tied to project pipelines and broader economic conditions.

Here, the 5.4x price-to-earnings ratio screens as good value relative to both the broader Hong Kong market multiple of 12.4x and the construction industry average of 10.7x. This suggests the market is pricing China Energy Engineering’s earnings at a clear discount. That discount also looks steep against the estimated fair price-to-earnings ratio of 12x, a level the market could move towards if earnings growth forecasts materialise and confidence in the new leadership bedded in.

Explore the SWS fair ratio for China Energy Engineering

Result: Price-to-Earnings of 5.4x (UNDERVALUED)

However, risks remain, including potential project delays in large infrastructure contracts and uncertainty around leadership transition, which may impact execution and investor confidence.

Find out about the key risks to this China Energy Engineering narrative.

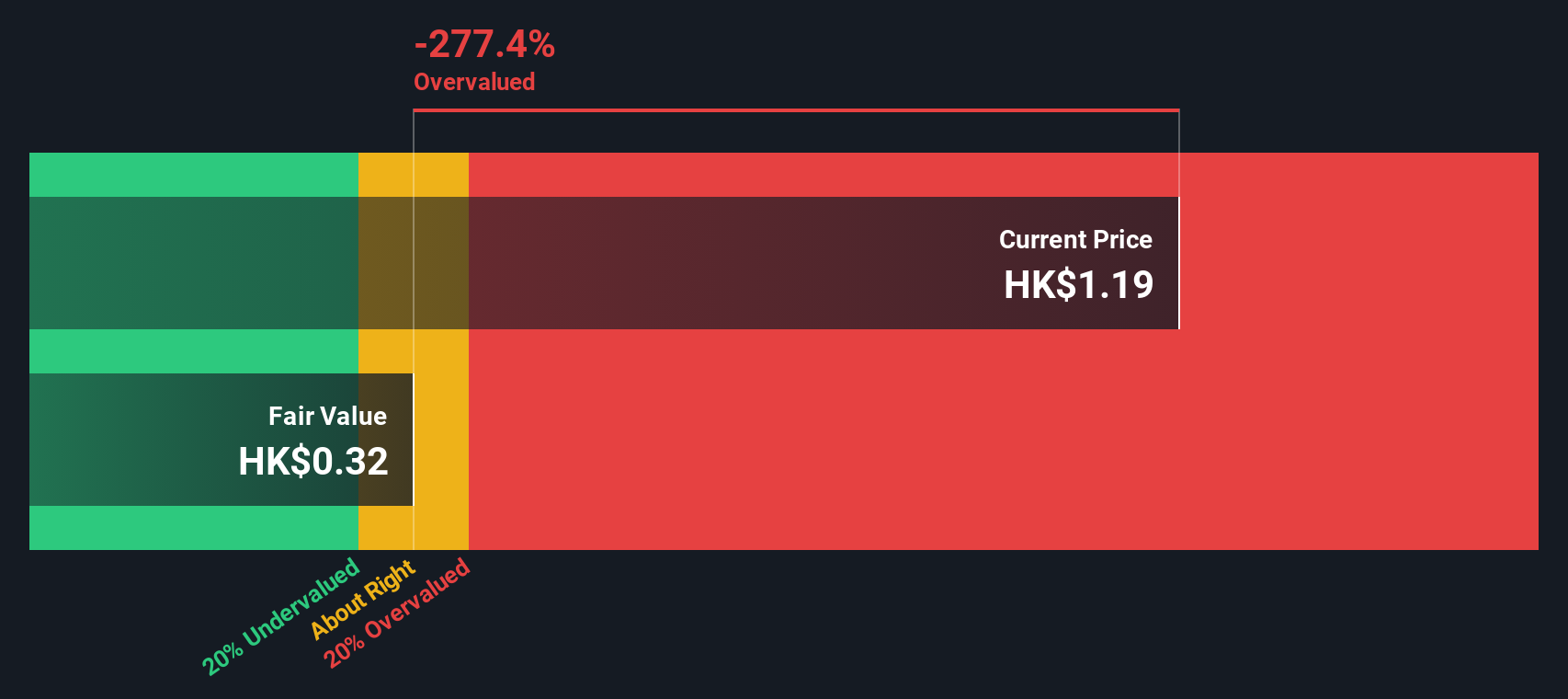

Another View, SWS DCF Model Flags Overvaluation

While the 5.4x earnings multiple hints at value, our DCF model tells a very different story, suggesting fair value closer to HK$0.32 per share versus today’s HK$1.14. If cash flows are right, that points to overvaluation. This raises an important question: which lens should investors trust?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out China Energy Engineering for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 927 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own China Energy Engineering Narrative

If you see the story differently or want to dig into the numbers yourself, you can build a custom view in just a few minutes: Do it your way.

A great starting point for your China Energy Engineering research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Ready for your next investing move?

Do not stop at one opportunity. Use Simply Wall Street’s screener to uncover fresh ideas that match your strategy and keep your portfolio moving forward.

- Capture long term income potential by targeting these 14 dividend stocks with yields > 3% that can strengthen your cash flow and support a more resilient portfolio.

- Ride powerful growth themes by focusing on these 24 AI penny stocks that are shaping the next wave of innovation and market leadership.

- Lock in potential bargains by scanning these 927 undervalued stocks based on cash flows that the market may be mispricing based on future cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:3996

China Energy Engineering

Provides solutions and services in the energy, power and infrastructure sectors in the People’s Republic of China and internationally.

Fair value with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

15 followersusers have followed this narrative

5 commentsusers have commented on this narrative

1 likeusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$126.1% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

YE

Yellow_fever on China Starch Holdings ·

China Starch Holdings eyes a revenue growth of 4.66% with a 5-year strategic plan

Fair Value:HK$0.563.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CO

composite32 on Power Solutions International ·

PSIX The timing of insider sales is a serious question mark

Fair Value:US$37.3845.7% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on Marvell Technology ·

The Great Strategy Swap – Selling "Old Auto" to Buy "Future Light"

Fair Value:US$155.3740.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.6% undervalued

112 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.5% undervalued

948 followersusers have followed this narrative

6 commentsusers have commented on this narrative

24 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3407.1% undervalued

148 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative