Advertisement

- Hong Kong

- /

- Trade Distributors

- /

- SEHK:387

Leeport (Holdings) (HKG:387) Will Pay A Smaller Dividend Than Last Year

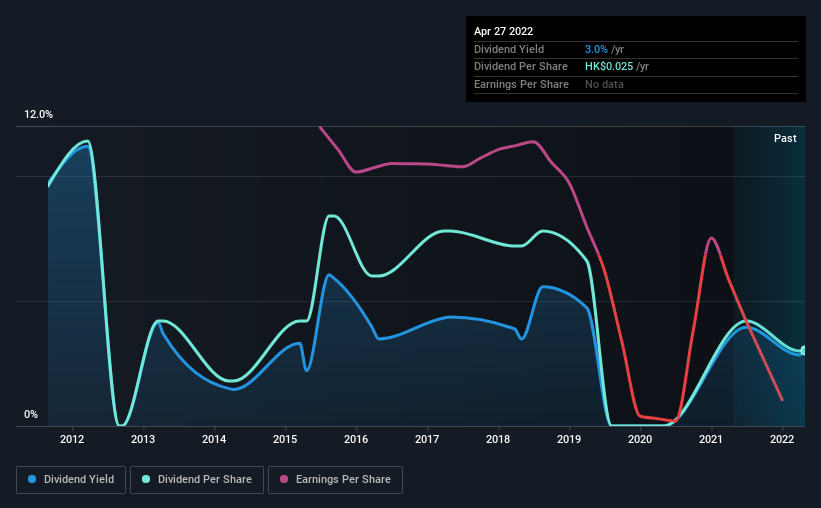

Leeport (Holdings) Limited (HKG:387) has announced it will be reducing its dividend payable on the 15th of July to HK$0.025. This means that the annual payment is 6.1% of the current stock price, which is lower than what the rest of the industry is paying.

See our latest analysis for Leeport (Holdings)

Leeport (Holdings)'s Distributions May Be Difficult To Sustain

The dividend yield is a little bit low, but sustainability of the payments is also an important part of evaluating an income stock. Even though Leeport (Holdings) isn't generating a profit, it is generating healthy free cash flows that easily cover the dividend. We generally think that cash flow is more important than accounting measures of profit, so we are fairly comfortable with the dividend at this level.

Looking forward, earnings per share could 57.7% over the next year if the trend of the last few years can't be broken. This means the company won't be turning a profit, which could place managers in the tough spot of having to choose between suspending the dividend or putting more pressure on the balance sheet.

Dividend Volatility

The company's dividend history has been marked by instability, with at least 1 cut in the last 10 years. Since 2012, the first annual payment was HK$0.08, compared to the most recent full-year payment of HK$0.025. The dividend has fallen 69% over that period. A company that decreases its dividend over time generally isn't what we are looking for.

Dividend Growth Potential Is Shaky

Given that the track record hasn't been stellar, we really want to see earnings per share growing over time. Earnings per share has been sinking by 58% over the last five years. Dividend payments are likely to come under some pressure unless EPS can pull out of the nosedive it is in.

Leeport (Holdings)'s Dividend Doesn't Look Sustainable

Overall, it's not great to see that the dividend has been cut, but this might be explained by the payments being a bit high previously. The payments haven't been particularly stable and we don't see huge growth potential, but with the dividend well covered by cash flows it could prove to be reliable over the short term. We would be a touch cautious of relying on this stock primarily for the dividend income.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. Case in point: We've spotted 3 warning signs for Leeport (Holdings) (of which 1 is a bit unpleasant!) you should know about. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:387

Leeport (Holdings)

An investment holding company, engages in the trading of metalworking machinery, measuring instruments, cutting tools, and electronic equipment in the People’s Republic of China, Hong Kong, and internationally.

Flawless balance sheet established dividend payer.

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|30.0% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|51.9% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|34.5% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|55.1% undervalued

AX

Community Contributor