Advertisement

- Hong Kong

- /

- Trade Distributors

- /

- SEHK:387

Leeport (Holdings) (HKG:387) Is Increasing Its Dividend To HK$0.035

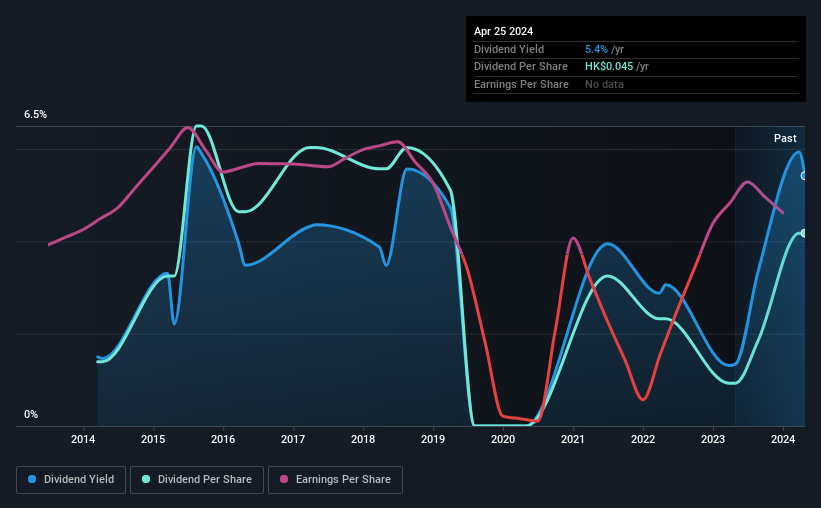

The board of Leeport (Holdings) Limited (HKG:387) has announced that it will be paying its dividend of HK$0.035 on the 15th of July, an increased payment from last year's comparable dividend. Even though the dividend went up, the yield is still quite low at only 5.4%.

Check out our latest analysis for Leeport (Holdings)

Leeport (Holdings) Doesn't Earn Enough To Cover Its Payments

The dividend yield is a little bit low, but sustainability of the payments is also an important part of evaluating an income stock. Before this announcement, Leeport (Holdings) was paying out 92% of earnings, but a comparatively small of free cash flows. Since the dividend is just paying out cash to shareholders, we care more about the cash payout ratio from which we can see plenty is being left over for reinvestment in the business.

EPS is set to fall by 10.1% over the next 12 months if recent trends continue. If the dividend continues along recent trends, we estimate the payout ratio could reach 97%, which could put the dividend in jeopardy if the company's earnings don't improve.

Dividend Volatility

The company's dividend history has been marked by instability, with at least one cut in the last 10 years. The dividend has gone from an annual total of HK$0.015 in 2014 to the most recent total annual payment of HK$0.045. This implies that the company grew its distributions at a yearly rate of about 12% over that duration. Dividends have grown rapidly over this time, but with cuts in the past we are not certain that this stock will be a reliable source of income in the future.

The Dividend Has Limited Growth Potential

With a relatively unstable dividend, it's even more important to see if earnings per share is growing. Leeport (Holdings)'s earnings per share has shrunk at 10% a year over the past five years. Dividend payments are likely to come under some pressure unless EPS can pull out of the nosedive it is in.

Our Thoughts On Leeport (Holdings)'s Dividend

In summary, while it's always good to see the dividend being raised, we don't think Leeport (Holdings)'s payments are rock solid. In the past, the payments have been unstable, but over the short term the dividend could be reliable, with the company generating enough cash to cover it. Overall, we don't think this company has the makings of a good income stock.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. For example, we've picked out 3 warning signs for Leeport (Holdings) that investors should know about before committing capital to this stock. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:387

Leeport (Holdings)

An investment holding company, engages in the trading of metalworking machinery, measuring instruments, cutting tools, and electronic equipment in the People’s Republic of China, Hong Kong, and internationally.

Flawless balance sheet established dividend payer.

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|30.0% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|51.9% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|34.5% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|55.1% undervalued

AX

Community Contributor