Advertisement

- Hong Kong

- /

- Trade Distributors

- /

- SEHK:299

We Think Glory Sun Land Group Limited's (HKG:299) CEO Compensation Package Needs To Be Put Under A Microscope

Key Insights

- Glory Sun Land Group to hold its Annual General Meeting on 6th of June

- Total pay for CEO Lingjie Xia includes HK$1.30m salary

- Total compensation is similar to the industry average

- Glory Sun Land Group's EPS declined by 51% over the past three years while total shareholder loss over the past three years was 98%

Shareholders will probably not be too impressed with the underwhelming results at Glory Sun Land Group Limited (HKG:299) recently. Shareholders will be interested in what the board will have to say about turning performance around at the next AGM on 6th of June. They will also get a chance to influence managerial decision-making through voting on resolutions such as executive remuneration, which may impact firm value in the future. The data we present below explains why we think CEO compensation is not consistent with recent performance.

Check out our latest analysis for Glory Sun Land Group

How Does Total Compensation For Lingjie Xia Compare With Other Companies In The Industry?

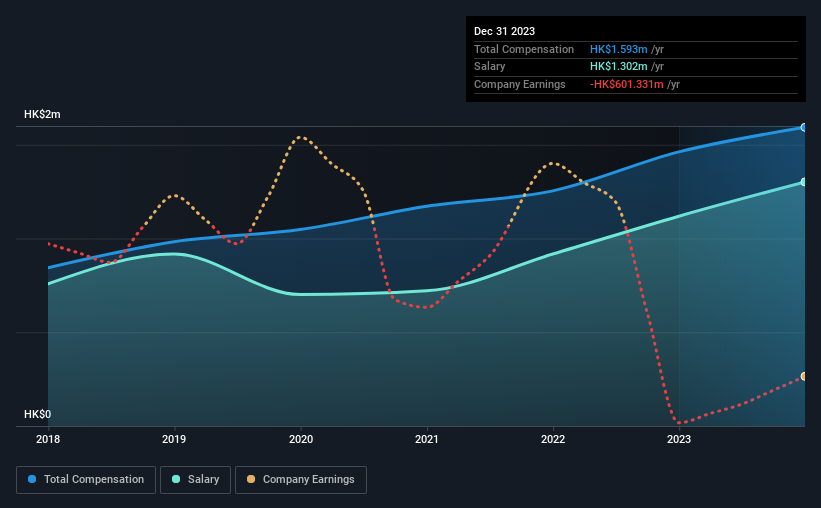

According to our data, Glory Sun Land Group Limited has a market capitalization of HK$22m, and paid its CEO total annual compensation worth HK$1.6m over the year to December 2023. Notably, that's an increase of 9.0% over the year before. We note that the salary portion, which stands at HK$1.30m constitutes the majority of total compensation received by the CEO.

In comparison with other companies in the Hong Kong Trade Distributors industry with market capitalizations under HK$1.6b, the reported median total CEO compensation was HK$2.0m. From this we gather that Lingjie Xia is paid around the median for CEOs in the industry.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | HK$1.3m | HK$1.1m | 82% |

| Other | HK$291k | HK$343k | 18% |

| Total Compensation | HK$1.6m | HK$1.5m | 100% |

Speaking on an industry level, nearly 92% of total compensation represents salary, while the remainder of 8% is other remuneration. In Glory Sun Land Group's case, non-salary compensation represents a greater slice of total remuneration, in comparison to the broader industry. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

Glory Sun Land Group Limited's Growth

Over the last three years, Glory Sun Land Group Limited has shrunk its earnings per share by 51% per year. It saw its revenue drop 26% over the last year.

Few shareholders would be pleased to read that EPS have declined. And the fact that revenue is down year on year arguably paints an ugly picture. It's hard to argue the company is firing on all cylinders, so shareholders might be averse to high CEO remuneration. Although we don't have analyst forecasts, you might want to assess this data-rich visualization of earnings, revenue and cash flow.

Has Glory Sun Land Group Limited Been A Good Investment?

With a total shareholder return of -98% over three years, Glory Sun Land Group Limited shareholders would by and large be disappointed. So shareholders would probably want the company to be less generous with CEO compensation.

In Summary...

Given that shareholders haven't seen any positive returns on their investment, not to mention the lack of earnings growth, this may suggest that few of them would be willing to award the CEO with a pay rise. At the upcoming AGM, management will get a chance to explain how they plan to get the business back on track and address the concerns from investors.

CEO compensation can have a massive impact on performance, but it's just one element. We did our research and spotted 2 warning signs for Glory Sun Land Group that investors should look into moving forward.

Of course, you might find a fantastic investment by looking at a different set of stocks. So take a peek at this free list of interesting companies.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:299

Glory Sun Land Group

An investment holding company, engages in the property development and investment business in the People’s Republic of China.

Good value slight.

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|19.2% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|86.0% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|14.3% undervalued

CH

Community Contributor