Advertisement

- Hong Kong

- /

- Industrials

- /

- SEHK:25

Chevalier International Holdings (HKG:25) Is Paying Out Less In Dividends Than Last Year

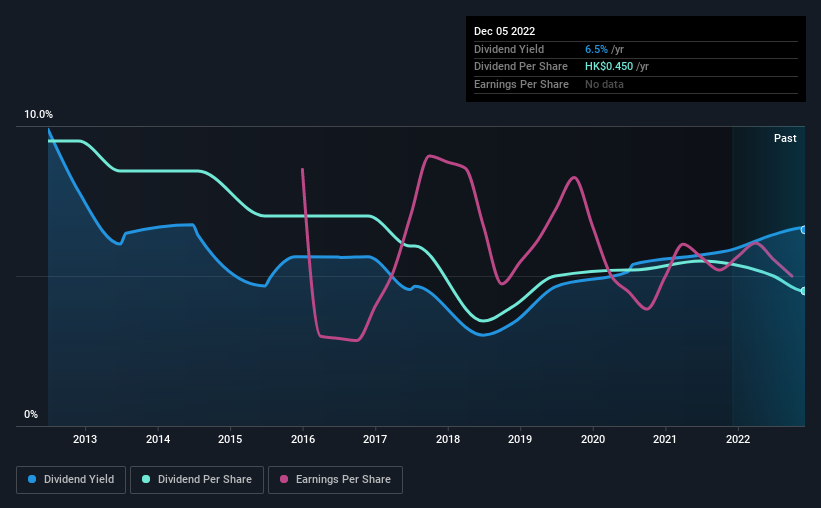

Chevalier International Holdings Limited's (HKG:25) dividend is being reduced from last year's payment covering the same period to HK$0.10 on the 22nd of December. Despite the cut, the dividend yield of 6.5% will still be comparable to other companies in the industry.

Check out the opportunities and risks within the HK Industrials industry.

Chevalier International Holdings' Payment Has Solid Earnings Coverage

We like a dividend to be consistent over the long term, so checking whether it is sustainable is important. Prior to this announcement, Chevalier International Holdings' dividend was only 26% of earnings, however it was paying out 366% of free cash flows. While the business may be attempting to set a balanced dividend policy, a cash payout ratio this high might expose the dividend to being cut if the business ran into some challenges.

Looking forward, EPS could fall by 11.1% if the company can't turn things around from the last few years. If the dividend continues along the path it has been on recently, we estimate the payout ratio could be 28%, which is definitely feasible to continue.

Dividend Volatility

While the company has been paying a dividend for a long time, it has cut the dividend at least once in the last 10 years. Since 2012, the dividend has gone from HK$0.95 total annually to HK$0.45. This works out to be a decline of approximately 7.2% per year over that time. A company that decreases its dividend over time generally isn't what we are looking for.

The Dividend Has Limited Growth Potential

Given that dividend payments have been shrinking like a glacier in a warming world, we need to check if there are some bright spots on the horizon. Chevalier International Holdings' earnings per share has shrunk at 11% a year over the past five years. Dividend payments are likely to come under some pressure unless EPS can pull out of the nosedive it is in.

The Dividend Could Prove To Be Unreliable

Overall, the dividend looks like it may have been a bit high, which explains why it has now been cut. While Chevalier International Holdings is earning enough to cover the payments, the cash flows are lacking. We don't think Chevalier International Holdings is a great stock to add to your portfolio if income is your focus.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. However, there are other things to consider for investors when analysing stock performance. Just as an example, we've come across 3 warning signs for Chevalier International Holdings you should be aware of, and 1 of them is a bit concerning. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:25

Chevalier International Holdings

Engages in the construction and engineering, property investment and development, healthcare investment, car dealership, and other businesses.

Mediocre balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|29.6% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|49.1% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|35.4% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|54.5% undervalued

AX

Community Contributor