It is no surprise that investors are buzzing about CK Hutchison Holdings (SEHK:1). With recent shifts in global markets, even slight movements in well-established conglomerates can trigger a fresh round of questions. The company’s diverse interests across telecommunications, retail, infrastructure, and ports make any news about its underlying performance particularly relevant for those weighing their next move.

Over the past year, the stock has delivered steady gains, rising 29% and outpacing many sector peers. Growth appears to have picked up in the past 3 months, and the company has been marking annual revenue and net income increases as well. Momentum has been building, though not without some short-term fluctuations typical for a group of its size and complexity.

Given all this, the real question is whether CK Hutchison Holdings is trading at a bargain or if the market has already factored future growth into its share price. Is there value left on the table, or is this as good as it gets?

Advertisement

Most Popular Narrative: 15.5% Undervalued

According to the most closely followed analysis of CK Hutchison Holdings, the stock is trading well below its estimated fair value. This widely cited narrative indicates a 15.5% discount, suggesting meaningful upside if the forecasts play out.

Sustained investment and efficiency-driven growth in the Ports division, including expanded facilities in key geographies and increased storage income, position the company to benefit from global trade resilience and supply chain optimization. This supports higher revenue and stable cash flows. Strategic expansion and modernization of the group's retail arm (notably A.S. Watson's store portfolio and loyalty program development, plus omni-channel and dark store initiatives), are anticipated to drive same-store sales growth and operational leverage, contributing to higher revenue and sustainable bottom-line growth.

Curious what is fueling this bold undervaluation? The answer lies in a series of aggressive projections for revenue, profits, and margins. These numbers hint at a potential transformation across CK Hutchison’s global businesses. Big changes are expected. The underlying assumptions behind these forecasts just might surprise you.

However, recurring gains from asset sales and currency moves, as well as ongoing weakness in Mainland China retail, could quickly challenge the bullish valuation case.

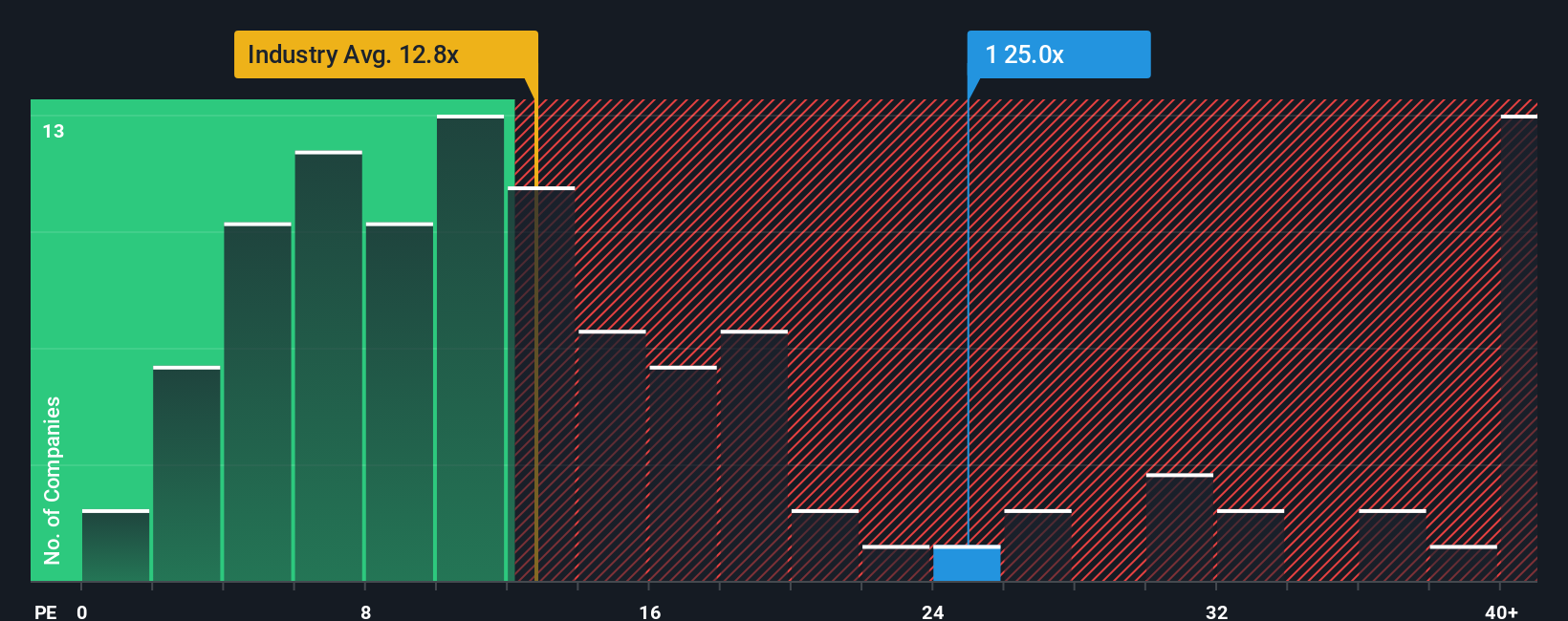

Looking through another lens, the current market price appears quite expensive relative to similar companies in the region. This view challenges the optimistic growth narrative and raises the question: has value already been priced in?

Stay updated when valuation signals shift by adding CK Hutchison Holdings to your watchlist or portfolio. Alternatively, explore our screener to discover other companies that fit your criteria.

Build Your Own CK Hutchison Holdings Narrative

If you have a different perspective or want to dig into the numbers yourself, you can craft a custom view of CK Hutchison Holdings in under three minutes. Do it your way

A great starting point for your CK Hutchison Holdings research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Unlock even more opportunities using our powerful screeners. Don’t limit yourself to just one stock when standout options are just a click away.

Find established names offering strong income by checking out stocks with reliable yields above 3% with dividend stocks with yields > 3%.

Uncover trendsetting innovations shaping the digital health space by tapping into the future of medical technology via healthcare AI stocks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield) • Undervalued Small Caps with Insider Buying • High growth Tech and AI Companies

Kshitija (or Keisha) Bhandaru is an Equity Analyst at Simply Wall St and has over 6 years of experience in the finance industry and describes herself as a lifelong learner driven by her intellectual curiosity. She previously worked with Market Realist for 5 years as an Equity Analyst.

An investment holding company, primarily operates in ports and related services, retail, infrastructure, and telecommunications businesses in Hong Kong, Mainland China, Europe, Canada, Asia, Australia, and internationally.