- Hong Kong

- /

- Auto Components

- /

- SEHK:1930

Here's What's Concerning About Shinelong Automotive Lightweight Application's (HKG:1930) Returns On Capital

If you're looking for a multi-bagger, there's a few things to keep an eye out for. Typically, we'll want to notice a trend of growing return on capital employed (ROCE) and alongside that, an expanding base of capital employed. This shows us that it's a compounding machine, able to continually reinvest its earnings back into the business and generate higher returns. Having said that, from a first glance at Shinelong Automotive Lightweight Application (HKG:1930) we aren't jumping out of our chairs at how returns are trending, but let's have a deeper look.

What is Return On Capital Employed (ROCE)?

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. The formula for this calculation on Shinelong Automotive Lightweight Application is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

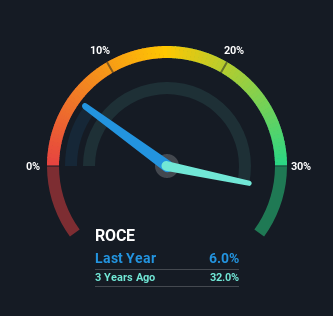

0.06 = CN¥18m ÷ (CN¥460m - CN¥156m) (Based on the trailing twelve months to June 2021).

Thus, Shinelong Automotive Lightweight Application has an ROCE of 6.0%. On its own that's a low return on capital but it's in line with the industry's average returns of 6.0%.

See our latest analysis for Shinelong Automotive Lightweight Application

While the past is not representative of the future, it can be helpful to know how a company has performed historically, which is why we have this chart above. If you want to delve into the historical earnings, revenue and cash flow of Shinelong Automotive Lightweight Application, check out these free graphs here.

So How Is Shinelong Automotive Lightweight Application's ROCE Trending?

When we looked at the ROCE trend at Shinelong Automotive Lightweight Application, we didn't gain much confidence. Around four years ago the returns on capital were 35%, but since then they've fallen to 6.0%. And considering revenue has dropped while employing more capital, we'd be cautious. This could mean that the business is losing its competitive advantage or market share, because while more money is being put into ventures, it's actually producing a lower return - "less bang for their buck" per se.

On a related note, Shinelong Automotive Lightweight Application has decreased its current liabilities to 34% of total assets. That could partly explain why the ROCE has dropped. Effectively this means their suppliers or short-term creditors are funding less of the business, which reduces some elements of risk. Some would claim this reduces the business' efficiency at generating ROCE since it is now funding more of the operations with its own money.

The Key Takeaway

In summary, we're somewhat concerned by Shinelong Automotive Lightweight Application's diminishing returns on increasing amounts of capital. Long term shareholders who've owned the stock over the last year have experienced a 24% depreciation in their investment, so it appears the market might not like these trends either. With underlying trends that aren't great in these areas, we'd consider looking elsewhere.

Shinelong Automotive Lightweight Application does come with some risks though, we found 3 warning signs in our investment analysis, and 1 of those is concerning...

While Shinelong Automotive Lightweight Application may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1930

Shinelong Automotive Lightweight Application

An investment holding company, designs and develops moulding services and solutions in Mainland China and internationally.

Excellent balance sheet with proven track record.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Stride Stock: Online Education Finds Its Second Act

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)