Advertisement

- Greece

- /

- Metals and Mining

- /

- ATSE:ALMY

Here's Why We Don't Think Alumil Aluminium Industry's (ATH:ALMY) Statutory Earnings Reflect Its Underlying Earnings Potential

As a general rule, we think profitable companies are less risky than companies that lose money. However, sometimes companies receive a one-off boost (or reduction) to their profit, and it's not always clear whether statutory profits are a good guide, going forward. Today we'll focus on whether this year's statutory profits are a good guide to understanding Alumil Aluminium Industry (ATH:ALMY).

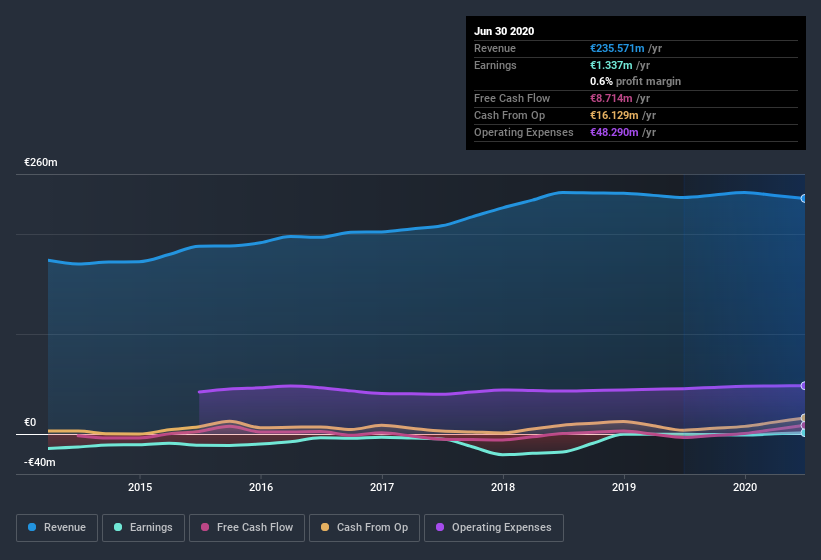

We like the fact that Alumil Aluminium Industry made a profit of €1.34m on its revenue of €235.6m, in the last year. The chart below shows that revenue has improved over the last three years, and, even better, the company has moved from unprofitable to profitable.

See our latest analysis for Alumil Aluminium Industry

Importantly, statutory profits are not always the best tool for understanding a company's true earnings power, so it's well worth examining profits in a little more detail. In this article we'll look at how Alumil Aluminium Industry is impacting shareholders by issuing new shares, as well as how unusual items have affected the income line. Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Alumil Aluminium Industry.

To understand the value of a company's earnings growth, it is imperative to consider any dilution of shareholders' interests. As it happens, Alumil Aluminium Industry issued 47% more new shares over the last year. Therefore, each share now receives a smaller portion of profit. Per share metrics like EPS help us understand how much actual shareholders are benefitting from the company's profits, while the net income level gives us a better view of the company's absolute size. Check out Alumil Aluminium Industry's historical EPS growth by clicking on this link.

A Look At The Impact Of Alumil Aluminium Industry's Dilution on Its Earnings Per Share (EPS).

Alumil Aluminium Industry was losing money three years ago. And even focusing only on the last twelve months, we don't have a meaningful growth rate because it made a loss a year ago, too. But mathematics aside, it is always good to see when a formerly unprofitable business come good (though we accept profit would have been higher if dilution had not been required). And so, you can see quite clearly that dilution is having a rather significant impact on shareholders.

In the long term, if Alumil Aluminium Industry's earnings per share can increase, then the share price should too. But on the other hand, we'd be far less excited to learn profit (but not EPS) was improving. For the ordinary retail shareholder, EPS is a great measure to check your hypothetical "share" of the company's profit.

The Impact Of Unusual Items On Profit

Alongside that dilution, it's also important to note that Alumil Aluminium Industry's profit was boosted by unusual items worth €1.7m in the last twelve months. While it's always nice to have higher profit, a large contribution from unusual items sometimes dampens our enthusiasm. When we analysed the vast majority of listed companies worldwide, we found that significant unusual items are often not repeated. Which is hardly surprising, given the name. Assuming those unusual items don't show up again in the current year, we'd thus expect profit to be weaker next year (in the absence of business growth, that is).

Our Take On Alumil Aluminium Industry's Profit Performance

In its last report Alumil Aluminium Industry benefitted from unusual items which boosted its profit, which could make the profit seem better than it really is on a sustainable basis. On top of that, the dilution means that its earnings per share performance is worse than its profit performance. Considering all this we'd argue Alumil Aluminium Industry's profits probably give an overly generous impression of its sustainable level of profitability. So while earnings quality is important, it's equally important to consider the risks facing Alumil Aluminium Industry at this point in time. Case in point: We've spotted 5 warning signs for Alumil Aluminium Industry you should be mindful of and 1 of these shouldn't be ignored.

Our examination of Alumil Aluminium Industry has focussed on certain factors that can make its earnings look better than they are. And, on that basis, we are somewhat skeptical. But there are plenty of other ways to inform your opinion of a company. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

If you decide to trade Alumil Aluminium Industry, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About ATSE:ALMY

Alumil Aluminium Industry

Engages in the design, development, and production of aluminum architectural systems in Greece and internationally.

Solid track record with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|24.5% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|45.3% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|33.9% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|57.0% undervalued

AX

Community Contributor