- Greece

- /

- Construction

- /

- ATSE:DOMIK

Will Weakness in Domiki Kritis S.A.'s (ATH:DOMIK) Stock Prove Temporary Given Strong Fundamentals?

With its stock down 27% over the past three months, it is easy to disregard Domiki Kritis (ATH:DOMIK). However, stock prices are usually driven by a company’s financial performance over the long term, which in this case looks quite promising. In this article, we decided to focus on Domiki Kritis' ROE.

Return on equity or ROE is an important factor to be considered by a shareholder because it tells them how effectively their capital is being reinvested. In simpler terms, it measures the profitability of a company in relation to shareholder's equity.

View our latest analysis for Domiki Kritis

How Is ROE Calculated?

The formula for return on equity is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Domiki Kritis is:

14% = €1.9m ÷ €13m (Based on the trailing twelve months to December 2023).

The 'return' refers to a company's earnings over the last year. Another way to think of that is that for every €1 worth of equity, the company was able to earn €0.14 in profit.

Why Is ROE Important For Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher the growth rate of a company compared to companies that don't necessarily bear these characteristics.

Domiki Kritis' Earnings Growth And 14% ROE

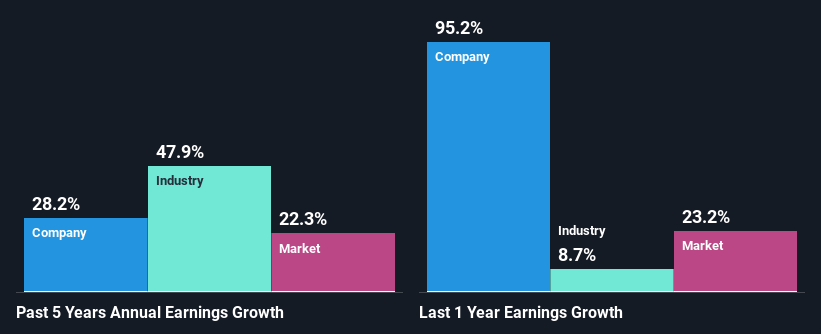

To begin with, Domiki Kritis seems to have a respectable ROE. Further, the company's ROE is similar to the industry average of 14%. Consequently, this likely laid the ground for the impressive net income growth of 28% seen over the past five years by Domiki Kritis. However, there could also be other drivers behind this growth. Such as - high earnings retention or an efficient management in place.

As a next step, we compared Domiki Kritis' net income growth with the industry and were disappointed to see that the company's growth is lower than the industry average growth of 48% in the same period.

The basis for attaching value to a company is, to a great extent, tied to its earnings growth. What investors need to determine next is if the expected earnings growth, or the lack of it, is already built into the share price. Doing so will help them establish if the stock's future looks promising or ominous. Is Domiki Kritis fairly valued compared to other companies? These 3 valuation measures might help you decide.

Is Domiki Kritis Using Its Retained Earnings Effectively?

Domiki Kritis doesn't pay any regular dividends to its shareholders, meaning that the company has been reinvesting all of its profits into the business. This is likely what's driving the high earnings growth number discussed above.

Summary

On the whole, we feel that Domiki Kritis' performance has been quite good. Particularly, we like that the company is reinvesting heavily into its business, and at a high rate of return. As a result, the decent growth in its earnings is not surprising. If the company continues to grow its earnings the way it has, that could have a positive impact on its share price given how earnings per share influence long-term share prices. Not to forget, share price outcomes are also dependent on the potential risks a company may face. So it is important for investors to be aware of the risks involved in the business. To know the 1 risk we have identified for Domiki Kritis visit our risks dashboard for free.

If you're looking to trade Domiki Kritis, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ATSE:DOMIK

Domiki Kritis

Primarily engages in the construction of heavy infrastructure projects for public and private sectors in Greece.

Adequate balance sheet slight.

Market Insights

Community Narratives