Advertisement

- United Kingdom

- /

- IT

- /

- LSE:CCC

Computacenter plc's (LON:CCC) Share Price Not Quite Adding Up

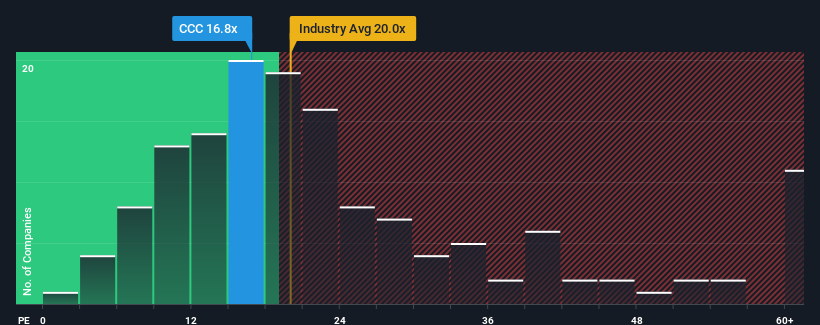

With a median price-to-earnings (or "P/E") ratio of close to 17x in the United Kingdom, you could be forgiven for feeling indifferent about Computacenter plc's (LON:CCC) P/E ratio of 16.8x. While this might not raise any eyebrows, if the P/E ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

Computacenter certainly has been doing a good job lately as it's been growing earnings more than most other companies. It might be that many expect the strong earnings performance to wane, which has kept the P/E from rising. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's not quite in favour.

View our latest analysis for Computacenter

How Is Computacenter's Growth Trending?

Computacenter's P/E ratio would be typical for a company that's only expected to deliver moderate growth, and importantly, perform in line with the market.

Retrospectively, the last year delivered a decent 8.0% gain to the company's bottom line. EPS has also lifted 29% in aggregate from three years ago, partly thanks to the last 12 months of growth. Accordingly, shareholders would have probably been satisfied with the medium-term rates of earnings growth.

Turning to the outlook, the next three years should generate growth of 3.9% per annum as estimated by the ten analysts watching the company. That's shaping up to be materially lower than the 14% each year growth forecast for the broader market.

With this information, we find it interesting that Computacenter is trading at a fairly similar P/E to the market. It seems most investors are ignoring the fairly limited growth expectations and are willing to pay up for exposure to the stock. These shareholders may be setting themselves up for future disappointment if the P/E falls to levels more in line with the growth outlook.

The Bottom Line On Computacenter's P/E

Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

Our examination of Computacenter's analyst forecasts revealed that its inferior earnings outlook isn't impacting its P/E as much as we would have predicted. Right now we are uncomfortable with the P/E as the predicted future earnings aren't likely to support a more positive sentiment for long. This places shareholders' investments at risk and potential investors in danger of paying an unnecessary premium.

You always need to take note of risks, for example - Computacenter has 1 warning sign we think you should be aware of.

You might be able to find a better investment than Computacenter. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:CCC

Computacenter

Provides technology and services to corporate and public sector organizations in the United Kingdom, Germany, Western Europe, North America, and internationally.

Flawless balance sheet with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Sparc Al ·

When GPS fails: this small cap is fixing a $54B drone problem

Fair Value:CA$5.251.3% overvalued

18 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

SO

sorkdhkddlek on Marvell Technology ·

From AI Infrastructure Plumber to Full-Stack AI Factory Architect

Fair Value:US$14018.0% overvalued

14 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

MI

MiningStockAnalyst on Aurelia Metals ·

Aurelia Metals Limited — Transitioning Into a Higher-Quality Mid-Tier Producer

Fair Value:AU$0.427.5% undervalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

CO

composite32 on TotalEnergies ·

Is This strategic transformation of TTE? Significant re-rating potential

Fair Value:€88.2910.2% undervalued

16 followersusers have followed this narrative

2 commentsusers have commented on this narrative

3 likesusers have liked this narrative

Recently Updated Narratives

JA

Janpeo on Stellantis ·

IA Analysis

Fair Value:€1143.5% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AS

Asrikk on NVIDIA ·

Sustainable Dominance: Justifying a $270 Fair Value

Fair Value:US$27026.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MR

MRT23 on CorMedix ·

CRMD is trading at 5.9x trough-year EBITDA with the market ascribing near-zero value to two near-term pipeline events

Fair Value:US$1236.8% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

KI

Kingman1152 on NVIDIA ·

NVIDIA will see a profit margin surge of 55% in the next 5 years

Fair Value:US$305.234.6% undervalued

68 followersusers have followed this narrative

2 commentsusers have commented on this narrative

24 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$579.5729.6% undervalued

1392 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

TR

tripledub on Meta Platforms ·

The $135 Billion Bet That Should Make Every Shareholder Nervous

Fair Value:US$5805.5% overvalued

30 followersusers have followed this narrative

3 commentsusers have commented on this narrative

31 likesusers have liked this narrative