- United Kingdom

- /

- Software

- /

- AIM:SAAS

Why It Might Not Make Sense To Buy Microlise Group plc (LON:SAAS) For Its Upcoming Dividend

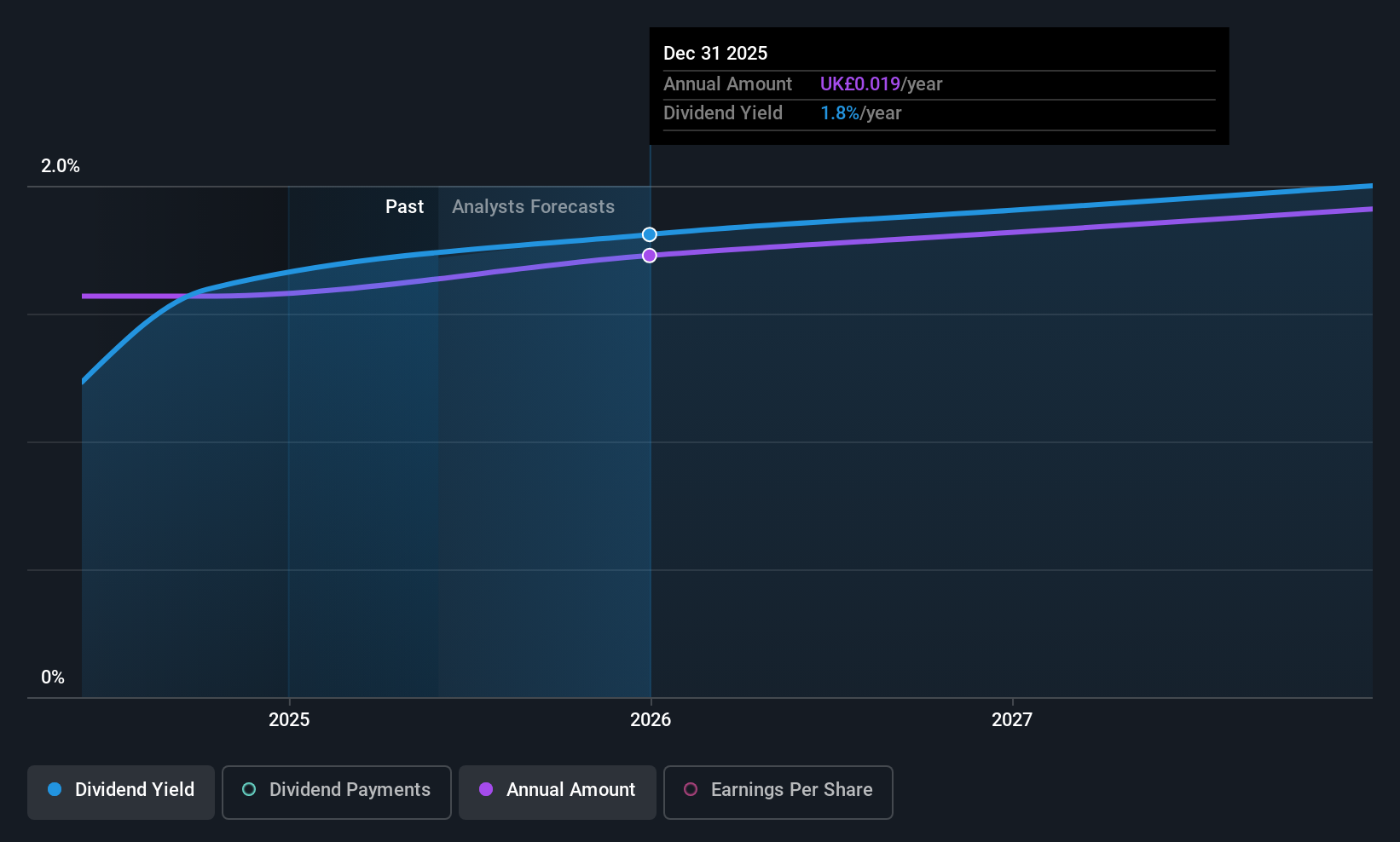

Microlise Group plc (LON:SAAS) is about to trade ex-dividend in the next three days. The ex-dividend date is usually set to be two business days before the record date, which is the cut-off date on which you must be present on the company's books as a shareholder in order to receive the dividend. The ex-dividend date is important as the process of settlement involves at least two full business days. So if you miss that date, you would not show up on the company's books on the record date. In other words, investors can purchase Microlise Group's shares before the 5th of June in order to be eligible for the dividend, which will be paid on the 27th of June.

The company's next dividend payment will be UK£0.0124 per share, and in the last 12 months, the company paid a total of UK£0.018 per share. Last year's total dividend payments show that Microlise Group has a trailing yield of 1.7% on the current share price of UK£1.05. If you buy this business for its dividend, you should have an idea of whether Microlise Group's dividend is reliable and sustainable. So we need to investigate whether Microlise Group can afford its dividend, and if the dividend could grow.

If a company pays out more in dividends than it earned, then the dividend might become unsustainable - hardly an ideal situation. Microlise Group reported a loss after tax last year, which means it's paying a dividend despite being unprofitable. While this might be a one-off event, this is unlikely to be sustainable in the long term. With the recent loss, it's important to check if the business generated enough cash to pay its dividend. If cash earnings don't cover the dividend, the company would have to pay dividends out of cash in the bank, or by borrowing money, neither of which is long-term sustainable. Thankfully its dividend payments took up just 48% of the free cash flow it generated, which is a comfortable payout ratio.

View our latest analysis for Microlise Group

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

When earnings decline, dividend companies become much harder to analyse and own safely. If business enters a downturn and the dividend is cut, the company could see its value fall precipitously. Microlise Group reported a loss last year, and the general trend suggests its earnings have also been declining in recent years, making us wonder if the dividend is at risk.

Unfortunately Microlise Group has only been paying a dividend for a year or so, so there's not much of a history to draw insight from.

Get our latest analysis on Microlise Group's balance sheet health here.

The Bottom Line

From a dividend perspective, should investors buy or avoid Microlise Group? First, it's not great to see the company paying a dividend despite being loss-making over the last year. On the plus side, the dividend was covered by free cash flow." With the way things are shaping up from a dividend perspective, we'd be inclined to steer clear of Microlise Group.

Wondering what the future holds for Microlise Group? See what the four analysts we track are forecasting, with this visualisation of its historical and future estimated earnings and cash flow

If you're in the market for strong dividend payers, we recommend checking our selection of top dividend stocks.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About AIM:SAAS

Microlise Group

Provides transport management technology solutions in the United Kingdom, Rest of Europe, and internationally.

Flawless balance sheet and undervalued.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Hitit Bilgisayar Hizmetleri will achieve a 19.7% revenue boost in the next five years

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)