Advertisement

- United Kingdom

- /

- Specialty Stores

- /

- LSE:TPT

Shareholders May Be Wary Of Increasing Topps Tiles Plc's (LON:TPT) CEO Compensation Package

Key Insights

- Topps Tiles to hold its Annual General Meeting on 18 January 2023

- CEO Rob Parker's total compensation includes salary of UK£412.0k

- Total compensation is 31% above industry average

- Topps Tiles' EPS grew by -4.1% over the past three years while total shareholder return over the past three years was -30%

The results at Topps Tiles Plc (LON:TPT) have been quite disappointing recently and CEO Rob Parker bears some responsibility for this. Shareholders can take the chance to hold the board and management accountable for the unsatisfactory performance at the next AGM on 18 January 2023. It would also be an opportunity for shareholders to influence management through voting on company resolutions such as executive remuneration, which could impact the firm significantly. We present the case why we think CEO compensation is out of sync with company performance.

Check out our latest analysis for Topps Tiles

Comparing Topps Tiles Plc's CEO Compensation With The Industry

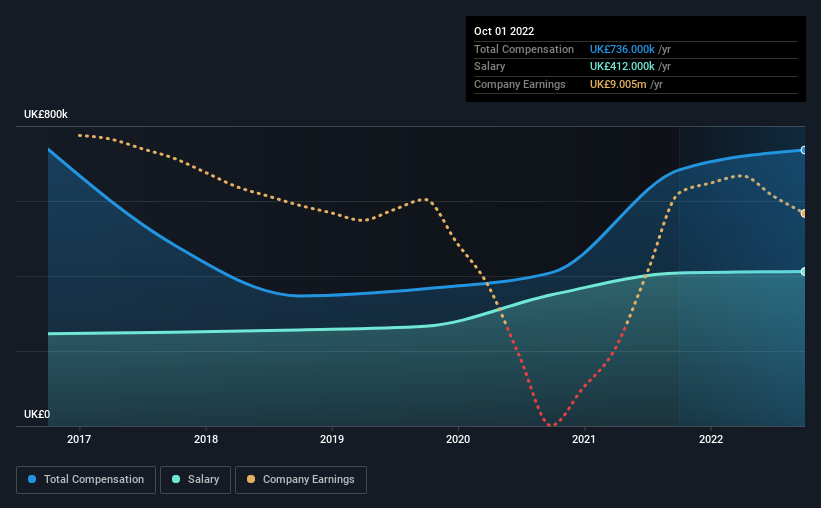

According to our data, Topps Tiles Plc has a market capitalization of UK£92m, and paid its CEO total annual compensation worth UK£736k over the year to October 2022. That's just a smallish increase of 7.8% on last year. In particular, the salary of UK£412.0k, makes up a fairly large portion of the total compensation being paid to the CEO.

In comparison with other companies in the British Specialty Retail industry with market capitalizations under UK£165m, the reported median total CEO compensation was UK£561k. This suggests that Rob Parker is paid more than the median for the industry. What's more, Rob Parker holds UK£455k worth of shares in the company in their own name.

| Component | 2022 | 2021 | Proportion (2022) |

| Salary | UK£412k | UK£408k | 56% |

| Other | UK£324k | UK£275k | 44% |

| Total Compensation | UK£736k | UK£683k | 100% |

Speaking on an industry level, nearly 48% of total compensation represents salary, while the remainder of 52% is other remuneration. According to our research, Topps Tiles has allocated a higher percentage of pay to salary in comparison to the wider industry. If salary dominates total compensation, it suggests that CEO compensation is leaning less towards the variable component, which is usually linked with performance.

A Look at Topps Tiles Plc's Growth Numbers

Over the last three years, Topps Tiles Plc has shrunk its earnings per share by 4.1% per year. In the last year, its revenue is up 8.5%.

The decline in EPS is a bit concerning. The fairly low revenue growth fails to impress given that the EPS is down. It's hard to argue the company is firing on all cylinders, so shareholders might be averse to high CEO remuneration. Moving away from current form for a second, it could be important to check this free visual depiction of what analysts expect for the future.

Has Topps Tiles Plc Been A Good Investment?

With a total shareholder return of -30% over three years, Topps Tiles Plc shareholders would by and large be disappointed. This suggests it would be unwise for the company to pay the CEO too generously.

To Conclude...

Along with the business performing poorly, shareholders have suffered with poor share price returns on their investments, suggesting that there's little to no chance of them being in favor of a CEO pay raise. At the upcoming AGM, the board will get the chance to explain the steps it plans to take to improve business performance.

CEO compensation is a crucial aspect to keep your eyes on but investors also need to keep their eyes open for other issues related to business performance. We did our research and spotted 2 warning signs for Topps Tiles that investors should look into moving forward.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

Valuation is complex, but we're here to simplify it.

Discover if Topps Tiles might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About LSE:TPT

Topps Tiles

Engages in the retail and wholesale distribution of ceramic and porcelain tiles, natural stone, and related products for residential and commercial markets in the United Kingdom.

Undervalued with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

100% Patient Improvement in trial puts this $16M Biotech on the radar

Fair Value US$5.30|74.9% undervalued

JO

Community Contributor

PayPal's Future Growth Through Venmo and Merchant Solutions

Fair Value US$105.25|35.1% undervalued

ZW

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$26.54|1.5% undervalued

BL

Community Contributor