- United Kingdom

- /

- Retail REITs

- /

- LSE:SUPR

UK Undervalued Small Caps With Insider Action In January 2025

Reviewed by Simply Wall St

Amidst the backdrop of a faltering FTSE 100 and sluggish global economic signals, particularly from China, the UK market has seen its major indices slip as concerns over commodity demand and domestic consumption in key international markets weigh heavily. Despite these challenges, small-cap stocks often present unique opportunities for investors seeking growth potential that may not be fully reflected in broader market movements. In this environment, identifying small-cap companies with solid fundamentals and insider activity can be an intriguing strategy.

Top 10 Undervalued Small Caps With Insider Buying In The United Kingdom

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| NCC Group | NA | 1.3x | 28.11% | ★★★★★★ |

| 4imprint Group | 14.9x | 1.2x | 42.65% | ★★★★★☆ |

| Speedy Hire | NA | 0.3x | 36.30% | ★★★★★☆ |

| Sabre Insurance Group | 11.0x | 1.4x | 15.87% | ★★★★☆☆ |

| iomart Group | 24.5x | 0.7x | 32.86% | ★★★★☆☆ |

| Gym Group | NA | 1.2x | 17.02% | ★★★★☆☆ |

| Warpaint London | 23.7x | 4.1x | 2.96% | ★★★☆☆☆ |

| Telecom Plus | 17.2x | 0.7x | 33.36% | ★★★☆☆☆ |

| Robert Walters | 35.7x | 0.2x | 29.03% | ★★★☆☆☆ |

| THG | NA | 0.3x | -518.35% | ★★★☆☆☆ |

We're going to check out a few of the best picks from our screener tool.

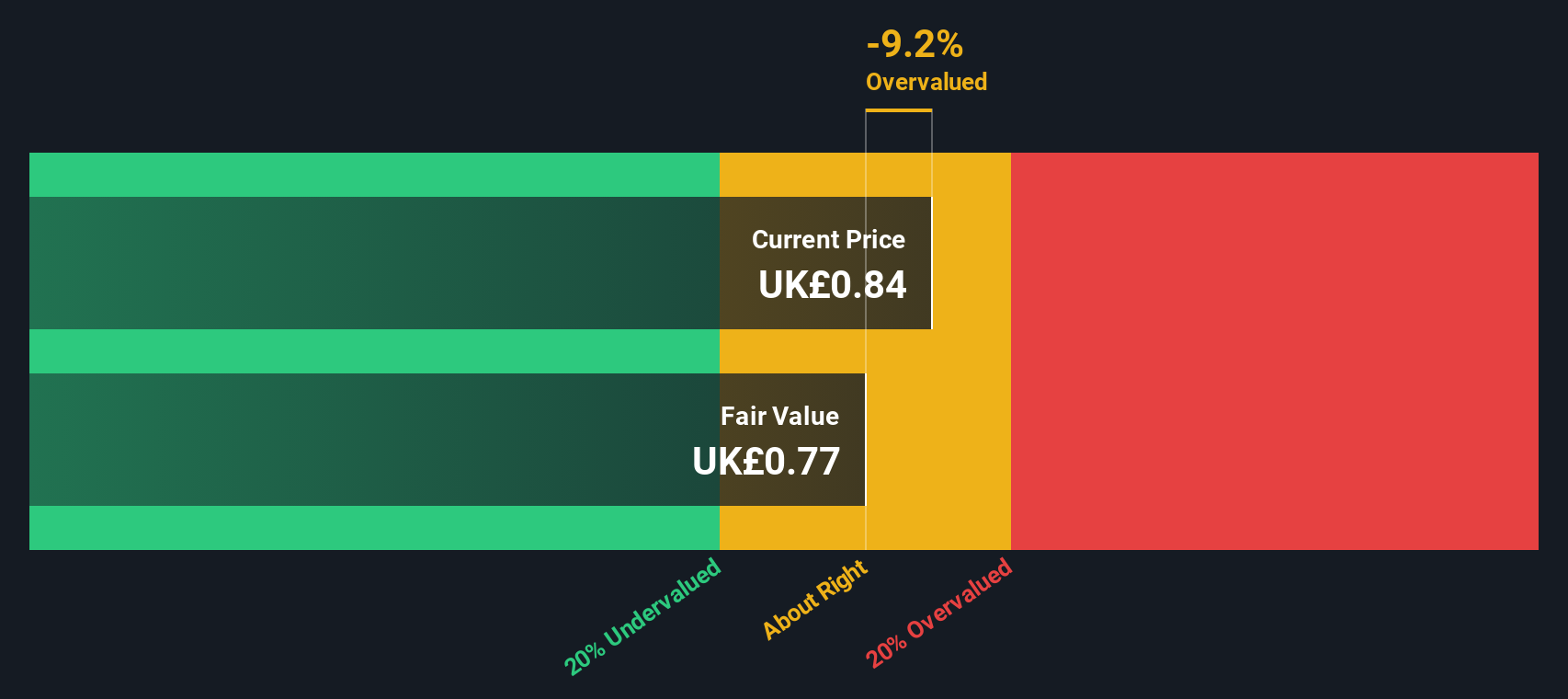

ASOS (LSE:ASC)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: ASOS is an online retailer specializing in fashion and beauty products with a market capitalization of approximately £1.28 billion.

Operations: ASOS generates its revenue primarily through online retailing, with recent figures showing £2.91 billion in sales. The company's gross profit margin has shown a declining trend, reaching 40.01% in the latest period. Operating expenses are significant, notably in general and administrative costs and sales and marketing efforts.

PE: -1.3x

ASOS, a notable player in the UK market, has been navigating financial challenges, reporting sales of £2.9 billion for the fiscal year ending September 2024, down from £3.5 billion previously. Despite a net loss of £338.7 million and high debt levels due to reliance on external borrowing, insider confidence is evident with recent share purchases in late 2024. The company anticipates revenue growth ranging from -9% to +6% for 2025, suggesting potential recovery amidst its current undervaluation challenges.

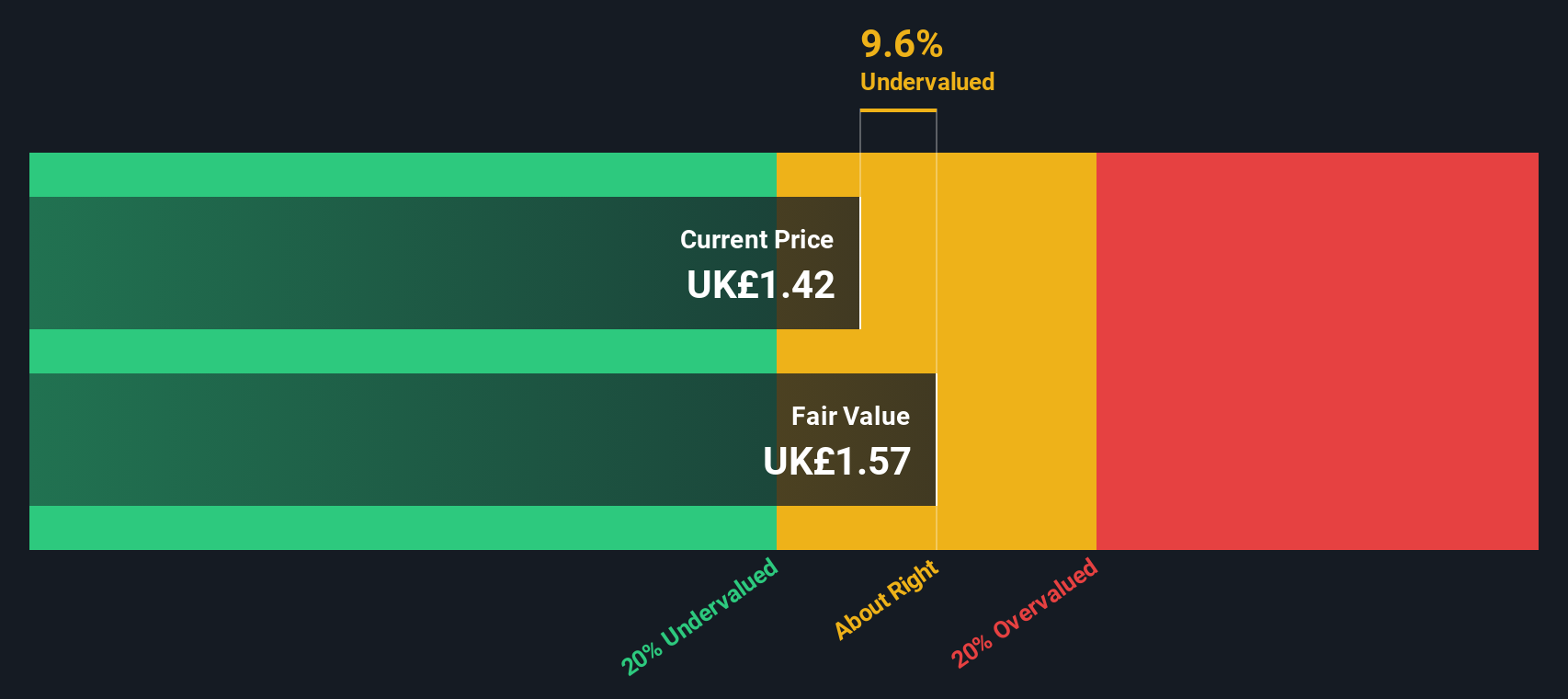

NCC Group (LSE:NCC)

Simply Wall St Value Rating: ★★★★★★

Overview: NCC Group is a global cybersecurity and risk mitigation company with operations focused on providing services such as cyber security consulting and managed detection, boasting a market cap of approximately £0.46 billion.

Operations: The company derives its revenue primarily from Cyber Security (£256.58 million) and Escode (£65.55 million). The gross profit margin has shown variability, reaching 41.61% in recent periods, while net income has experienced fluctuations with a recent negative trend, registering -£24.38 million by January 2025. Operating expenses have been significant, contributing to the overall financial performance dynamics observed over the analyzed periods.

PE: -17.2x

NCC Group, a smaller UK firm, has shown insider confidence with recent share purchases. Despite reporting a net loss of £32.5 million for the sixteen months ending September 2024, they anticipate earnings growth of nearly 75% annually. This potential for growth contrasts with their reliance on higher-risk external borrowing as their sole funding source. Recently, NCC proposed a final dividend of 1.5p per share to be paid in April 2025, indicating commitment to returning value to shareholders amidst financial challenges.

- Get an in-depth perspective on NCC Group's performance by reading our valuation report here.

Gain insights into NCC Group's historical performance by reviewing our past performance report.

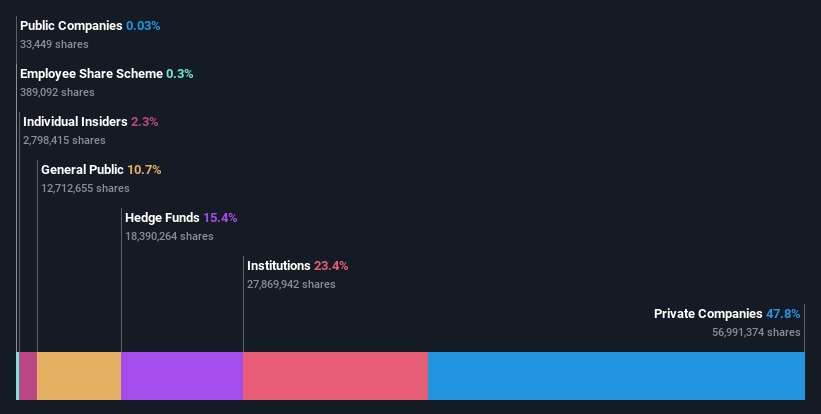

Supermarket Income REIT (LSE:SUPR)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Supermarket Income REIT focuses on investing in supermarket properties across the UK, with a market cap of £1.21 billion.

Operations: The company's revenue is primarily derived from real estate investments, with a reported gross profit margin consistently at 100.00%. Operating expenses have shown a gradual increase, reaching £5.75 million in the latest period. Net income margins have experienced significant fluctuations, recently recording a negative -0.20%.

PE: -39.5x

Supermarket Income REIT, a UK-based property investment firm, recently declared a dividend of 1.53 pence per share for Q2 2024, indicating steady income distribution to shareholders. Despite relying solely on external borrowing for funding, the company maintains a solid financial position with debt well-covered by operating cash flow. Insider confidence is evident as they increased their holdings over the past year. Earnings are projected to grow by 48% annually, suggesting potential growth in this segment.

Next Steps

- Unlock our comprehensive list of 36 Undervalued UK Small Caps With Insider Buying by clicking here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:SUPR

Supermarket Income REIT

Supermarket Income REIT plc (LSE: SUPR) is a real estate investment trust dedicated to investing in grocery properties which are an essential part of the UK's feed the nation infrastructure.

Reasonable growth potential average dividend payer.

Similar Companies

Market Insights

Community Narratives