Advertisement

- United Kingdom

- /

- Metals and Mining

- /

- LSE:HOC

Top UK Growth Stocks With High Insider Ownership In March 2025

Simply Wall St

Reviewed by Simply Wall St

As the UK market grapples with global economic uncertainties, particularly influenced by China's sluggish recovery from the pandemic, investors are closely monitoring how these conditions impact indices like the FTSE 100 and FTSE 250. In such a climate, growth companies with high insider ownership can often provide a sense of stability and confidence, as significant insider stakes may indicate strong belief in their long-term potential despite broader market challenges.

Top 10 Growth Companies With High Insider Ownership In The United Kingdom

| Name | Insider Ownership | Earnings Growth |

| Gulf Keystone Petroleum (LSE:GKP) | 12.2% | 102.1% |

| Foresight Group Holdings (LSE:FSG) | 34.8% | 27% |

| Helios Underwriting (AIM:HUW) | 23.8% | 23.1% |

| ASA International Group (LSE:ASAI) | 16.8% | 29.5% |

| LSL Property Services (LSE:LSL) | 10.4% | 26.9% |

| Facilities by ADF (AIM:ADF) | 13.2% | 190% |

| Mortgage Advice Bureau (Holdings) (AIM:MAB1) | 19.8% | 25.4% |

| Judges Scientific (AIM:JDG) | 10.7% | 29.3% |

| Getech Group (AIM:GTC) | 11.8% | 114.5% |

| Anglo Asian Mining (AIM:AAZ) | 40% | 116.2% |

Here's a peek at a few of the choices from the screener.

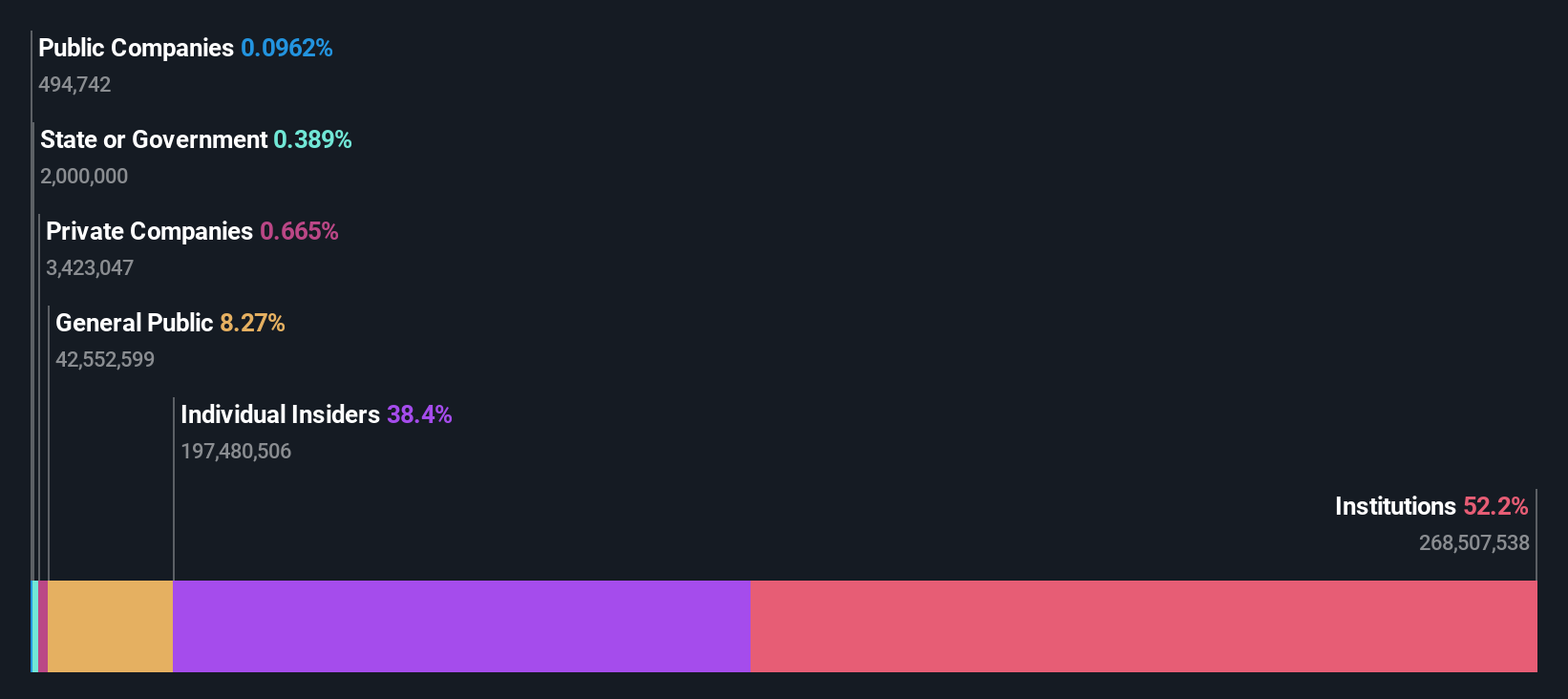

Hochschild Mining (LSE:HOC)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Hochschild Mining plc is a precious metals company involved in the exploration, mining, processing, and sale of gold and silver across several countries including Peru, Argentina, the United States, Canada, Brazil, and Chile with a market cap of approximately £946.60 million.

Operations: The company's revenue segments include $266.70 million from San Jose and $451.91 million from Inmaculada, with a segment adjustment of $79.60 million.

Insider Ownership: 38.4%

Earnings Growth Forecast: 40.3% p.a.

Hochschild Mining, with its recent appointment of Andrew Wray as an independent Non-Executive Director, is positioned for strategic growth in the UK market. Despite a volatile share price recently, the company has become profitable and its earnings are expected to grow significantly at 40.31% annually, outpacing the UK market average. Trading at 24.3% below fair value estimates and despite high debt levels, Hochschild's revenue growth forecast of 9.1% remains above the market rate.

- Delve into the full analysis future growth report here for a deeper understanding of Hochschild Mining.

- In light of our recent valuation report, it seems possible that Hochschild Mining is trading behind its estimated value.

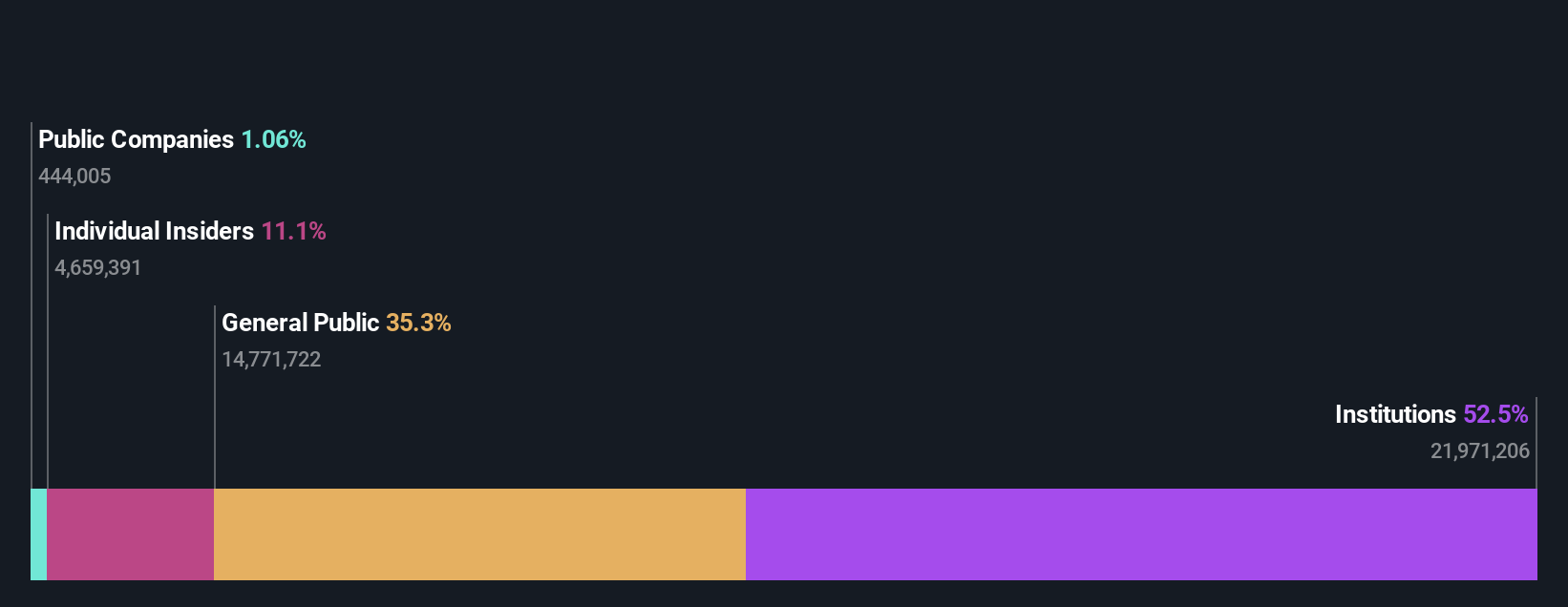

LSL Property Services (LSE:LSL)

Simply Wall St Growth Rating: ★★★★★☆

Overview: LSL Property Services plc operates in the United Kingdom, offering business-to-business services to mortgage intermediaries and estate agency franchisees, as well as valuation services to lenders, with a market cap of £281.81 million.

Operations: The company's revenue segments include Financial Services generating £47.22 million, Surveying and Valuation contributing £79.49 million, and Estate Agency (excluding Financial Services) bringing in £30.61 million.

Insider Ownership: 10.4%

Earnings Growth Forecast: 26.9% p.a.

LSL Property Services is poised for substantial growth, with earnings forecast to increase significantly at 26.9% annually, surpassing the UK market average. Revenue is expected to grow at 11.7% per year, also outpacing the market. Recent leadership changes include Adam Castleton's transition from CFO to CEO in May 2025, ensuring continuity and strategic direction. Insider activity shows more buying than selling recently, indicating confidence in its undervalued stock trading below fair value estimates.

- Unlock comprehensive insights into our analysis of LSL Property Services stock in this growth report.

- The valuation report we've compiled suggests that LSL Property Services' current price could be quite moderate.

PPHE Hotel Group (LSE:PPH)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: PPHE Hotel Group Limited is involved in owning, co-owning, developing, leasing, operating, and franchising upscale hotels across several European countries including the Netherlands and the United Kingdom, with a market cap of £547.44 million.

Operations: The company's revenue is primarily derived from its owned hotel operations in the United Kingdom (£249.03 million), Croatia (£84.27 million), the Netherlands (£66.20 million), and Germany, Hungary, and Serbia (£24.40 million), along with management and central services contributing £55.93 million.

Insider Ownership: 14.8%

Earnings Growth Forecast: 26.5% p.a.

PPHE Hotel Group anticipates significant earnings growth of 26.5% annually, outpacing the UK market. Despite slower revenue growth at 4.8% per year, it remains above the market average. Insider ownership is substantial, with Eli Papouchado and family trusts holding a large stake, though recent leadership changes followed his stepping down amid legal issues. The stock trades well below estimated fair value but faces challenges with interest coverage and dividend sustainability despite recent increases.

- Click here and access our complete growth analysis report to understand the dynamics of PPHE Hotel Group.

- Our valuation report unveils the possibility PPHE Hotel Group's shares may be trading at a discount.

Make It Happen

- Click this link to deep-dive into the 61 companies within our Fast Growing UK Companies With High Insider Ownership screener.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Hochschild Mining might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:HOC

Hochschild Mining

A precious metals company, engages in the exploration, mining, processing, and sale of gold and silver deposits in Peru, Argentina, the United Kingdom, Canada, Brazil, and Chile.

Reasonable growth potential and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

RIO is poised to weather a depressed iron ore environment, but commodity diversification comes with lower margins

Fair Value AU$110.51|4.0% overvalued

DU

Community Contributor

The demand for personalized medicine will keep Thermo Fisher Scientific thriving

Fair Value US$540.27|21.5% undervalued

UN

Community Contributor

Silver Play by A Family with 10x Potential

Fair Value UK£24.00|88.8% undervalued

RO

Community Contributor