- United Kingdom

- /

- Real Estate

- /

- LSE:IWG

3 UK Growth Stocks Insiders Are Betting On

Reviewed by Simply Wall St

Over the last 7 days, the United Kingdom market has remained flat, but it is up 7.4% over the past year with earnings forecast to grow by 14% annually. In such a promising environment, growth companies with high insider ownership can be particularly appealing as they often indicate strong confidence from those who know the business best.

Top 10 Growth Companies With High Insider Ownership In The United Kingdom

| Name | Insider Ownership | Earnings Growth |

| Energean (LSE:ENOG) | 10.6% | 30.4% |

| Integrated Diagnostics Holdings (LSE:IDHC) | 27.6% | 23.7% |

| Helios Underwriting (AIM:HUW) | 23.9% | 16.1% |

| LSL Property Services (LSE:LSL) | 10.8% | 28.2% |

| Facilities by ADF (AIM:ADF) | 22.7% | 144.7% |

| Judges Scientific (AIM:JDG) | 11.9% | 21.2% |

| Belluscura (AIM:BELL) | 36.3% | 113.4% |

| Enteq Technologies (AIM:NTQ) | 19.9% | 53.8% |

| Mortgage Advice Bureau (Holdings) (AIM:MAB1) | 19.8% | 29.0% |

| Gulf Keystone Petroleum (LSE:GKP) | 12.1% | 80.6% |

Let's take a closer look at a couple of our picks from the screened companies.

Evoke (LSE:EVOK)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Evoke plc, with a market cap of £277.57 million, offers online betting and gaming products and solutions across the United Kingdom, Ireland, Italy, Spain, and internationally.

Operations: Evoke's revenue segments include £514 million from Retail, £661.20 million from UK&I Online, and £516.10 million from International operations.

Insider Ownership: 20.5%

Evoke plc, a growth company with high insider ownership, has recently appointed Susan Standiford as an Independent Non-Executive Director. Despite reporting a net loss of £143.2 million for H1 2024, the company expects significant profitability improvement in H2 2024 due to successful product launches and effective promotions. Insiders have been substantially buying shares over the past three months, and earnings are forecasted to grow 104.91% annually with expected profitability within three years.

- Click here to discover the nuances of Evoke with our detailed analytical future growth report.

- Insights from our recent valuation report point to the potential undervaluation of Evoke shares in the market.

Hochschild Mining (LSE:HOC)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Hochschild Mining plc is a precious metals company involved in the exploration, mining, processing, and sale of gold and silver deposits across Peru, Argentina, the United States, Canada, Brazil, and Chile with a market cap of £962.04 million.

Operations: The company's revenue segments include $266.70 million from San Jose and $451.91 million from Inmaculada, with a segment adjustment of $79.60 million.

Insider Ownership: 38.4%

Hochschild Mining reported H1 2024 sales of US$391.74 million, up from US$314.02 million a year ago, with net income at US$39.52 million compared to a net loss of US$44.71 million previously. Earnings are forecasted to grow significantly at 44.63% per year, outpacing the UK market's growth rate of 14.2%. Despite trading at 47% below estimated fair value and having high debt levels, insider ownership remains robust without recent substantial insider trading activity.

- Click to explore a detailed breakdown of our findings in Hochschild Mining's earnings growth report.

- The valuation report we've compiled suggests that Hochschild Mining's current price could be quite moderate.

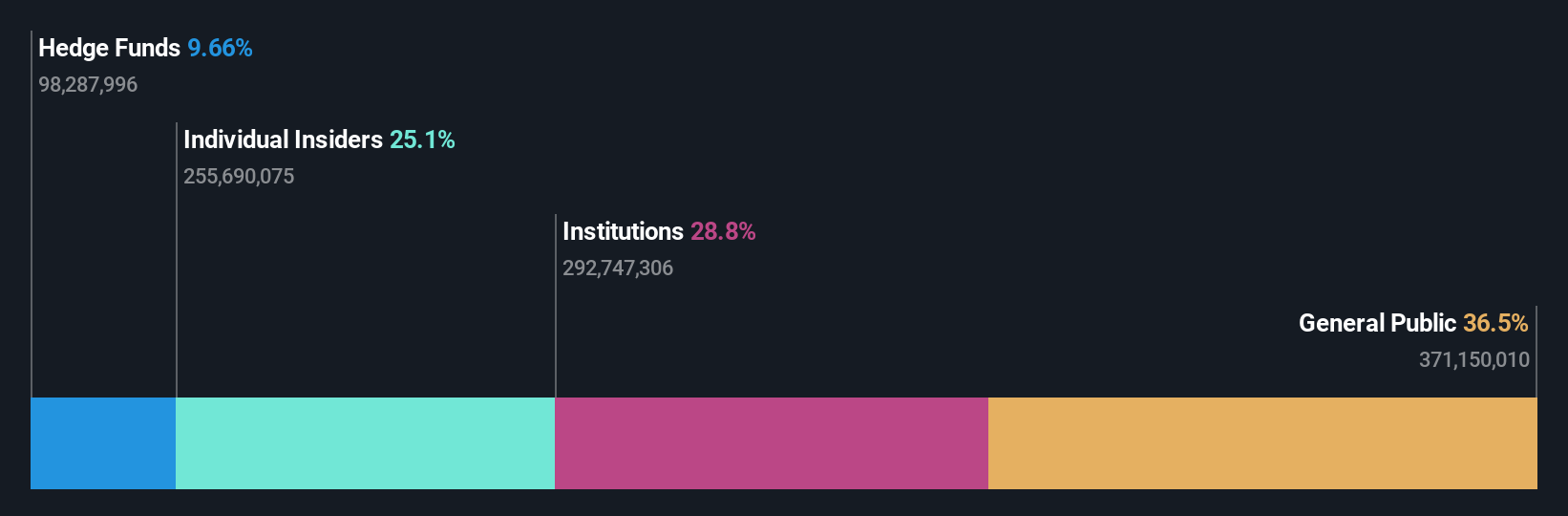

International Workplace Group (LSE:IWG)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: International Workplace Group plc, with a market cap of £1.74 billion, provides workspace solutions across the Americas, Europe, the Middle East, Africa, and the Asia Pacific through its subsidiaries.

Operations: The company's revenue segments include $400.56 million from Worka, $1.29 billion from the Americas, $341.30 million from the Asia Pacific, and $1.69 billion from Europe, the Middle East, and Africa (EMEA).

Insider Ownership: 25.2%

International Workplace Group (IWG) is forecast to become profitable within the next three years, with earnings expected to grow 115.58% annually. Insiders have been net buyers over the past three months, indicating confidence in future prospects. Despite a projected revenue growth of 8.9% per year, slower than some high-growth peers, IWG trades at good value compared to industry standards. Recent investor activism by Buckley Capital Management highlights significant undervaluation and suggests strategic actions like share buybacks and a potential US listing for enhanced valuation multiples.

- Click here and access our complete growth analysis report to understand the dynamics of International Workplace Group.

- The analysis detailed in our International Workplace Group valuation report hints at an deflated share price compared to its estimated value.

Make It Happen

- Click through to start exploring the rest of the 64 Fast Growing UK Companies With High Insider Ownership now.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:IWG

International Workplace Group

Provides workspace solutions in the Americas, Europe, the Middle East, Africa, and the Asia Pacific.

Good value with reasonable growth potential.