Advertisement

- United Kingdom

- /

- Chemicals

- /

- LSE:CAR

Carclo's (LON:CAR) Returns On Capital Not Reflecting Well On The Business

If you're looking at a mature business that's past the growth phase, what are some of the underlying trends that pop up? Typically, we'll see the trend of both return on capital employed (ROCE) declining and this usually coincides with a decreasing amount of capital employed. Ultimately this means that the company is earning less per dollar invested and on top of that, it's shrinking its base of capital employed. On that note, looking into Carclo (LON:CAR), we weren't too upbeat about how things were going.

Understanding Return On Capital Employed (ROCE)

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. To calculate this metric for Carclo, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.063 = UK£6.3m ÷ (UK£128m - UK£28m) (Based on the trailing twelve months to March 2022).

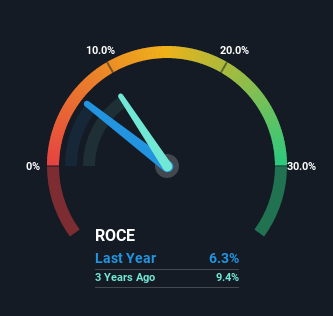

So, Carclo has an ROCE of 6.3%. In absolute terms, that's a low return and it also under-performs the Chemicals industry average of 12%.

Our analysis indicates that CAR is potentially undervalued!

Above you can see how the current ROCE for Carclo compares to its prior returns on capital, but there's only so much you can tell from the past. If you'd like to see what analysts are forecasting going forward, you should check out our free report for Carclo.

How Are Returns Trending?

In terms of Carclo's historical ROCE movements, the trend doesn't inspire confidence. To be more specific, the ROCE was 10% five years ago, but since then it has dropped noticeably. Meanwhile, capital employed in the business has stayed roughly the flat over the period. Companies that exhibit these attributes tend to not be shrinking, but they can be mature and facing pressure on their margins from competition. So because these trends aren't typically conducive to creating a multi-bagger, we wouldn't hold our breath on Carclo becoming one if things continue as they have.

The Bottom Line On Carclo's ROCE

In summary, it's unfortunate that Carclo is generating lower returns from the same amount of capital. We expect this has contributed to the stock plummeting 88% during the last five years. Unless there is a shift to a more positive trajectory in these metrics, we would look elsewhere.

One more thing: We've identified 5 warning signs with Carclo (at least 2 which are a bit concerning) , and understanding them would certainly be useful.

While Carclo may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About LSE:CAR

Carclo

Engages in the manufacture and sale of injection molded plastic parts.

Undervalued with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|30.0% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|51.9% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|34.5% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|55.1% undervalued

AX

Community Contributor