Advertisement

- United Kingdom

- /

- Insurance

- /

- AIM:HUW

Is Now The Time To Put Helios Underwriting (LON:HUW) On Your Watchlist?

Some have more dollars than sense, they say, so even companies that have no revenue, no profit, and a record of falling short, can easily find investors. And in their study titled Who Falls Prey to the Wolf of Wall Street?' Leuz et. al. found that it is 'quite common' for investors to lose money by buying into 'pump and dump' schemes.

So if you're like me, you might be more interested in profitable, growing companies, like Helios Underwriting (LON:HUW). While profit is not necessarily a social good, it's easy to admire a business that can consistently produce it. Conversely, a loss-making company is yet to prove itself with profit, and eventually the sweet milk of external capital may run sour.

View our latest analysis for Helios Underwriting

How Fast Is Helios Underwriting Growing Its Earnings Per Share?

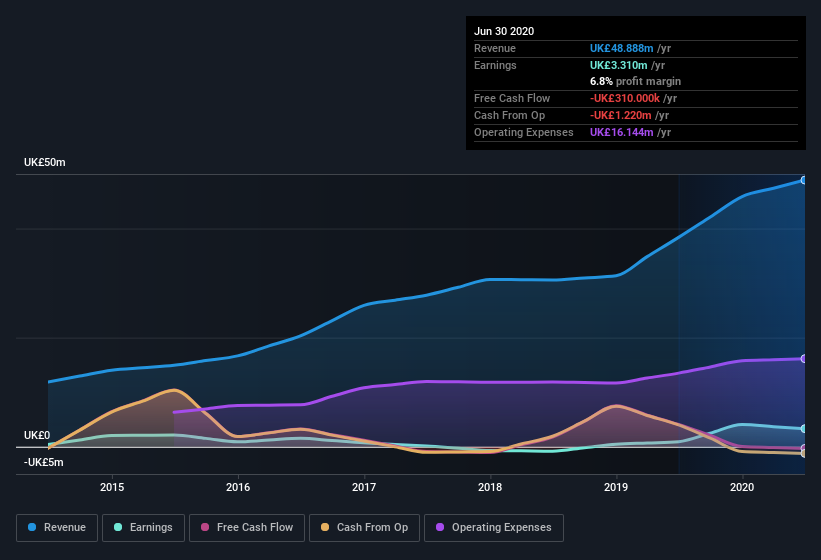

Over the last three years, Helios Underwriting has grown earnings per share (EPS) like young bamboo after rain; fast, and from a low base. So I don't think the percent growth rate is particularly meaningful. As a result, I'll zoom in on growth over the last year, instead. Like a firecracker arcing through the night sky, Helios Underwriting's EPS shot from UK£0.065 to UK£0.19, over the last year. You don't see 193% year-on-year growth like that, very often. The best case scenario? That the business has hit a true inflection point.

One way to double-check a company's growth is to look at how its revenue, and earnings before interest and tax (EBIT) margins are changing. Not all of Helios Underwriting's revenue this year is revenue from operations, so keep in mind the revenue and margin numbers I've used might not be the best representation of the underlying business. While we note Helios Underwriting's EBIT margins were flat over the last year, revenue grew by a solid 27% to UK£49m. That's a real positive.

In the chart below, you can see how the company has grown earnings, and revenue, over time. For finer detail, click on the image.

Since Helios Underwriting is no giant, with a market capitalization of UK£108m, so you should definitely check its cash and debt before getting too excited about its prospects.

Are Helios Underwriting Insiders Aligned With All Shareholders?

Like standing at the lookout, surveying the horizon at sunrise, insider buying, for some investors, sparks joy. This view is based on the possibility that stock purchases signal bullishness on behalf of the buyer. Of course, we can never be sure what insiders are thinking, we can only judge their actions.

Helios Underwriting insiders both bought and sold shares over the last twelve months, but they did end up spending UK£29k more on stock than they received from selling it. So, on balance, the insider transactions are mildly encouraging. It is also worth noting that it was Independent Non-Executive Chairman of the Board Harold Clunie Cunningham who made the biggest single purchase, worth UK£19k, paying UK£0.89 per share.

On top of the insider buying, it's good to see that Helios Underwriting insiders have a valuable investment in the business. To be specific, they have UK£20m worth of shares. That shows significant buy-in, and may indicate conviction in the business strategy. Those holdings account for over 18% of the company; visible skin in the game.

While insiders already own a significant amount of shares, and they have been buying more, the good news for ordinary shareholders does not stop there. That's because on our analysis the CEO, Nigel Hanbury, is paid less than the median for similar sized companies. For companies with market capitalizations between UK£71m and UK£284m, like Helios Underwriting, the median CEO pay is around UK£406k.

The Helios Underwriting CEO received total compensation of just UK£192k in the year to . That looks like modest pay to me, and may hint at a certain respect for the interests of shareholders. While the level of CEO compensation isn't a huge factor in my view of the company, modest remuneration is a positive, because it suggests that the board keeps shareholder interests in mind. I'd also argue reasonable pay levels attest to good decision making more generally.

Does Helios Underwriting Deserve A Spot On Your Watchlist?

Helios Underwriting's earnings have taken off like any random crypto-currency did, back in 2017. Just as heartening; insiders both own and are buying more stock. This quick rundown suggests that the business may be of good quality, and also at an inflection point, so maybe Helios Underwriting deserves timely attention. It's still necessary to consider the ever-present spectre of investment risk. We've identified 4 warning signs with Helios Underwriting (at least 1 which doesn't sit too well with us) , and understanding these should be part of your investment process.

The good news is that Helios Underwriting is not the only growth stock with insider buying. Here's a list of them... with insider buying in the last three months!

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

If you decide to trade Helios Underwriting, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Helios Underwriting might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About AIM:HUW

Helios Underwriting

Provides a limited liability investment for its shareholders in the Lloyd’s insurance market in the United Kingdom.

Undervalued with adequate balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|13.6% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$89.00|23.6% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|37.6% undervalued

TR

Community Contributor