Advertisement

- United Kingdom

- /

- Personal Products

- /

- LSE:PZC

We Think The Compensation For PZ Cussons plc's (LON:PZC) CEO Looks About Right

Performance at PZ Cussons plc (LON:PZC) has been reasonably good and CEO Jonathan Myers has done a decent job of steering the company in the right direction. This is something shareholders will keep in mind as they cast their votes on company resolutions such as executive remuneration in the upcoming AGM on 24 November 2022. Based on our analysis of the data below, we think CEO compensation seems reasonable for now.

Our analysis indicates that PZC is potentially undervalued!

Comparing PZ Cussons plc's CEO Compensation With The Industry

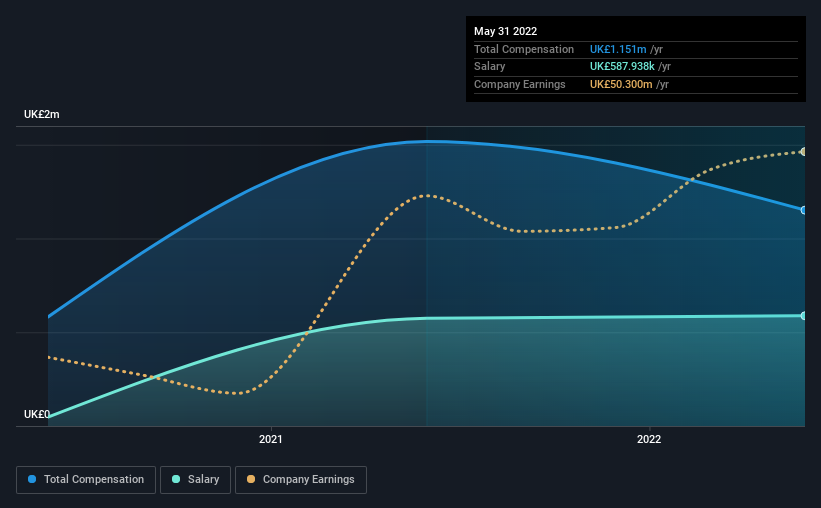

Our data indicates that PZ Cussons plc has a market capitalization of UK£856m, and total annual CEO compensation was reported as UK£1.2m for the year to May 2022. Notably, that's a decrease of 24% over the year before. Notably, the salary which is UK£587.9k, represents a considerable chunk of the total compensation being paid.

For comparison, other companies in the same industry with market capitalizations ranging between UK£340m and UK£1.4b had a median total CEO compensation of UK£1.3m. So it looks like PZ Cussons compensates Jonathan Myers in line with the median for the industry. What's more, Jonathan Myers holds UK£208k worth of shares in the company in their own name.

| Component | 2022 | 2021 | Proportion (2022) |

| Salary | UK£588k | UK£575k | 51% |

| Other | UK£563k | UK£943k | 49% |

| Total Compensation | UK£1.2m | UK£1.5m | 100% |

On an industry level, roughly 41% of total compensation represents salary and 59% is other remuneration. PZ Cussons pays out 51% of remuneration in the form of a salary, significantly higher than the industry average. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

PZ Cussons plc's Growth

PZ Cussons plc has seen its earnings per share (EPS) increase by 16% a year over the past three years. Its revenue is down 1.7% over the previous year.

This demonstrates that the company has been improving recently and is good news for the shareholders. It's always a tough situation when revenues are not growing, but ultimately profits are more important. Historical performance can sometimes be a good indicator on what's coming up next but if you want to peer into the company's future you might be interested in this free visualization of analyst forecasts.

Has PZ Cussons plc Been A Good Investment?

With a total shareholder return of 12% over three years, PZ Cussons plc shareholders would, in general, be reasonably content. But they would probably prefer not to see CEO compensation far in excess of the median.

To Conclude...

Seeing that the company has put up a decent performance, only a few shareholders, if any at all, might have questions about the CEO pay in the upcoming AGM. In saying that, any proposed increase to CEO compensation will still be assessed on how reasonable it is based on performance and industry benchmarks.

CEO compensation is a crucial aspect to keep your eyes on but investors also need to keep their eyes open for other issues related to business performance. We've identified 1 warning sign for PZ Cussons that investors should be aware of in a dynamic business environment.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About LSE:PZC

PZ Cussons

Manufactures, distributes, markets, and sells baby, beauty, and hygiene products in Europe, the Asia Pacific, the Americas, and Africa.

Very undervalued with moderate growth potential.

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|19.2% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|86.0% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|20.5% undervalued

CH

Community Contributor