Advertisement

- United Kingdom

- /

- Personal Products

- /

- AIM:CRL

Creightons (LON:CRL) Takes On Some Risk With Its Use Of Debt

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Creightons Plc (LON:CRL) does use debt in its business. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for Creightons

What Is Creightons's Debt?

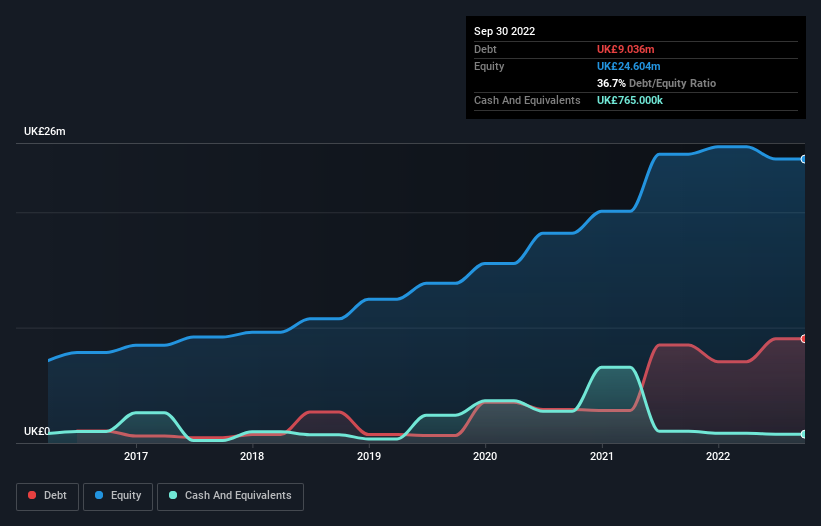

The image below, which you can click on for greater detail, shows that at September 2022 Creightons had debt of UK£9.04m, up from UK£8.50m in one year. However, it does have UK£765.0k in cash offsetting this, leading to net debt of about UK£8.27m.

A Look At Creightons' Liabilities

We can see from the most recent balance sheet that Creightons had liabilities of UK£16.7m falling due within a year, and liabilities of UK£7.74m due beyond that. On the other hand, it had cash of UK£765.0k and UK£14.5m worth of receivables due within a year. So it has liabilities totalling UK£9.21m more than its cash and near-term receivables, combined.

Creightons has a market capitalization of UK£21.9m, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Creightons's debt is 2.8 times its EBITDA, and its EBIT cover its interest expense 5.4 times over. This suggests that while the debt levels are significant, we'd stop short of calling them problematic. Importantly, Creightons's EBIT fell a jaw-dropping 62% in the last twelve months. If that decline continues then paying off debt will be harder than selling foie gras at a vegan convention. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since Creightons will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So it's worth checking how much of that EBIT is backed by free cash flow. In the last three years, Creightons's free cash flow amounted to 25% of its EBIT, less than we'd expect. That's not great, when it comes to paying down debt.

Our View

Mulling over Creightons's attempt at (not) growing its EBIT, we're certainly not enthusiastic. Having said that, its ability to cover its interest expense with its EBIT isn't such a worry. Looking at the bigger picture, it seems clear to us that Creightons's use of debt is creating risks for the company. If everything goes well that may pay off but the downside of this debt is a greater risk of permanent losses. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. To that end, you should be aware of the 4 warning signs we've spotted with Creightons .

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About AIM:CRL

Creightons

Develops, manufactures, and markets toiletries and fragrances in the United Kingdom and internationally.

Excellent balance sheet and good value.

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|26.3% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|4.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor