Advertisement

March 2025's Undervalued Small Caps With Insider Action In Global

Simply Wall St

Reviewed by Simply Wall St

In March 2025, global markets are grappling with economic uncertainty and inflation concerns, as consumer sentiment hits a 12-year low and U.S. stock indexes decline amid trade policy tensions. Despite these challenges, value stocks have shown resilience, outperforming growth shares for several weeks, suggesting that investors may find opportunities in small-cap stocks that demonstrate strong fundamentals and potential for growth in this volatile environment.

Top 10 Undervalued Small Caps With Insider Buying Globally

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Tristel | 23.2x | 3.3x | 40.28% | ★★★★★★ |

| Bytes Technology Group | 23.3x | 5.9x | 9.59% | ★★★★★☆ |

| Robert Walters | NA | 0.2x | 45.61% | ★★★★★☆ |

| Speedy Hire | NA | 0.2x | 27.18% | ★★★★★☆ |

| Sing Investments & Finance | 7.4x | 3.8x | 35.02% | ★★★★☆☆ |

| Saturn Oil & Gas | 7.2x | 0.5x | -39.69% | ★★★★☆☆ |

| Seeing Machines | NA | 2.1x | 39.33% | ★★★★☆☆ |

| Arendals Fossekompani | 21.4x | 1.6x | 46.10% | ★★★☆☆☆ |

| Westshore Terminals Investment | 13.2x | 3.8x | 31.80% | ★★★☆☆☆ |

| Manawa Energy | NA | 2.7x | 40.62% | ★★★☆☆☆ |

Let's dive into some prime choices out of from the screener.

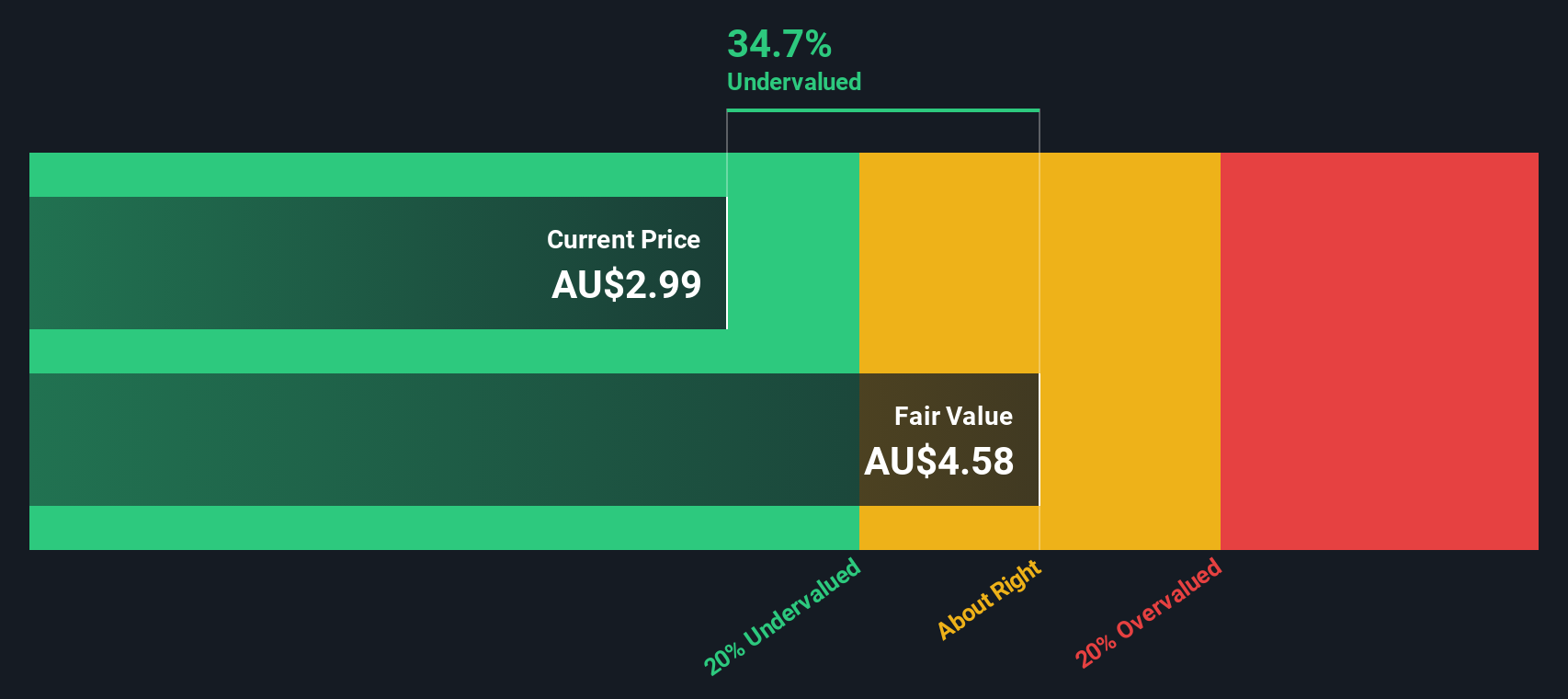

FleetPartners Group (ASX:FPR)

Simply Wall St Value Rating: ★★★★★★

Overview: FleetPartners Group operates as a provider of fleet management and leasing services, catering to corporate and government clients, with a market capitalization of approximately A$1.02 billion.

Operations: FleetPartners Group generates revenue through its core business activities, with a notable focus on managing costs effectively. Over recent periods, the gross profit margin has shown a downward trend from 42.28% in September 2017 to 29.20% by March 2025. The company faces significant cost of goods sold (COGS) and operating expenses, which are key components influencing its financial performance and profitability dynamics.

PE: 7.6x

FleetPartners Group, a small company in the leasing sector, faces challenges with its funding structure relying entirely on external borrowing, which is riskier compared to customer deposits. Despite insider confidence reflected in recent share purchases, earnings are projected to decline by 6% annually over the next three years. The company's debt coverage by operating cash flow remains inadequate. However, it extended its buyback plan until March 31, 2025, indicating potential strategic adjustments ahead.

- Unlock comprehensive insights into our analysis of FleetPartners Group stock in this valuation report.

Gain insights into FleetPartners Group's past trends and performance with our Past report.

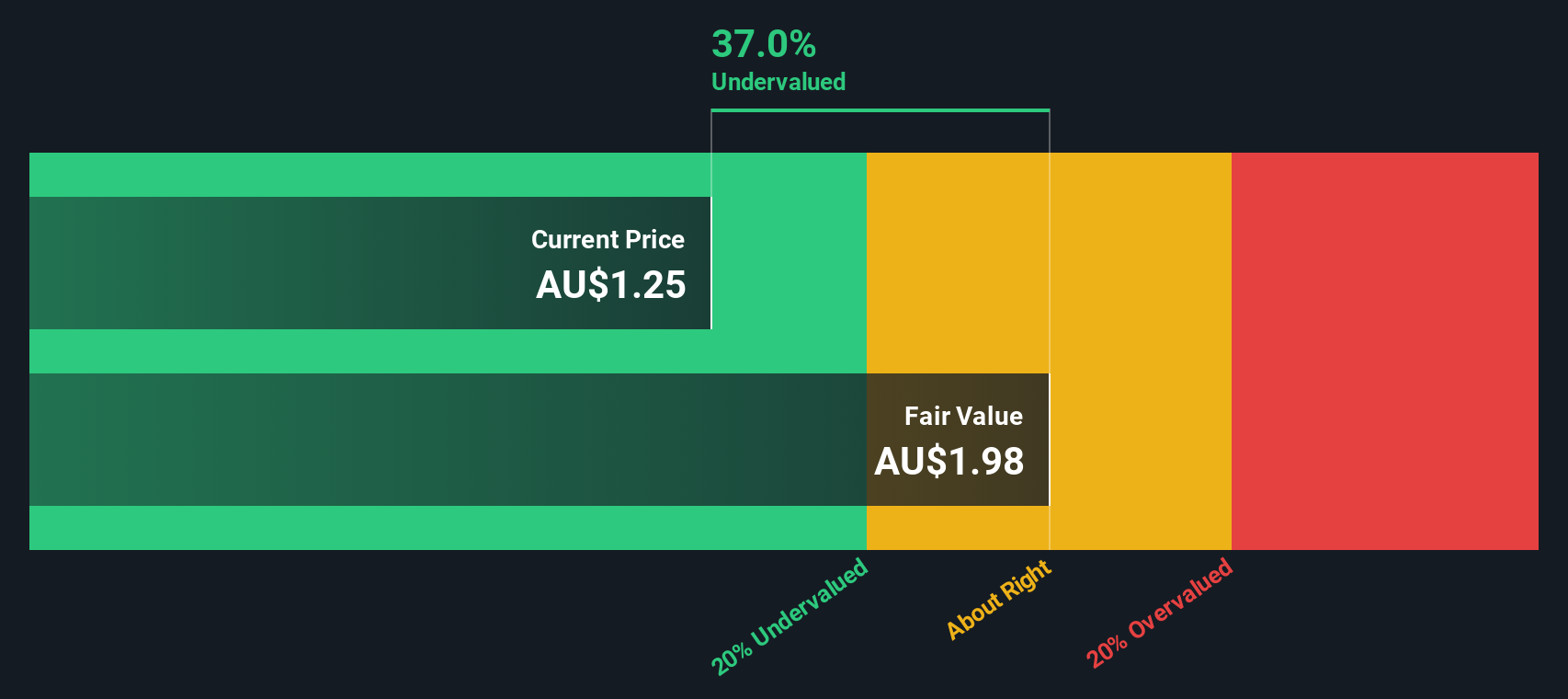

Infomedia (ASX:IFM)

Simply Wall St Value Rating: ★★★★★★

Overview: Infomedia is a company that specializes in publishing periodicals, with operations generating revenue primarily from this segment.

Operations: Infomedia generates revenue primarily from periodical publishing, with a gross profit margin of 95.32% as of the latest period. Operating expenses are a significant cost component, driven largely by general and administrative expenses, which reached A$71.36 million in the most recent quarter. The net income margin has shown variability over time, standing at 11.16% in the latest reported period.

PE: 31.2x

Infomedia, a smaller company in the tech sector, has been gaining attention due to its earnings growth forecast of nearly 20% annually. Despite relying entirely on external borrowing for funding, which carries higher risk than customer deposits, the company is actively managing its capital structure with a buyback program targeting up to 18.8 million shares by March 2026. Recent financials show improved performance with net income rising to A$8.33 million from A$5.12 million year-on-year, reflecting stronger operational results amid executive changes following health-related resignations.

- Get an in-depth perspective on Infomedia's performance by reading our valuation report here.

Review our historical performance report to gain insights into Infomedia's's past performance.

Seplat Energy (LSE:SEPL)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Seplat Energy is an independent energy company focused on oil and gas exploration and production, with a market cap of approximately £0.61 billion.

Operations: Seplat Energy's revenue is primarily derived from oil, contributing $990.99 million, and gas, with $124.91 million. The company's cost of goods sold (COGS) has been significant in recent periods, impacting its net income margins. Notably, the gross profit margin has shown variability over time but was 52.26% as of September 2023.

PE: 8.7x

Seplat Energy, a smaller company in the energy sector, is navigating financial complexities with recent debt refinancing and a special dividend announcement. The company issued $650 million in senior notes to manage existing debts and announced dividends of 6.9 US cents per share for May 2025. Despite high external borrowing risks, its revenue grew to $1.12 billion last year, up from $1.06 billion previously, reflecting potential for future growth despite forecasted earnings decline over the next three years.

- Click here to discover the nuances of Seplat Energy with our detailed analytical valuation report.

Explore historical data to track Seplat Energy's performance over time in our Past section.

Key Takeaways

- Investigate our full lineup of 147 Undervalued Global Small Caps With Insider Buying right here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:IFM

Infomedia

A technology company, develops and supplies electronic parts catalogues, service quoting software, and e-commerce solutions for the automotive industry worldwide.

Very undervalued with flawless balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|30.0% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|51.9% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|34.5% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|55.1% undervalued

AX

Community Contributor