Stock Analysis

- United Kingdom

- /

- Banks

- /

- LSE:TBCG

UK Growth Companies With High Insider Ownership And Up To 31% Earnings Growth

Reviewed by Simply Wall St

As the United Kingdom braces for significant political changes with the Labour Party leading in election polls, and financial markets like the FTSE 100 showing positive movements, investors are closely monitoring these shifts. In such a landscape, growth companies with high insider ownership can be particularly appealing as they often signal strong confidence from those who know the company best.

Top 10 Growth Companies With High Insider Ownership In The United Kingdom

| Name | Insider Ownership | Earnings Growth |

| Plant Health Care (AIM:PHC) | 31.2% | 121.3% |

| Petrofac (LSE:PFC) | 16.6% | 124.5% |

| Gulf Keystone Petroleum (LSE:GKP) | 10.8% | 47.6% |

| Integrated Diagnostics Holdings (LSE:IDHC) | 26.7% | 23.5% |

| Foresight Group Holdings (LSE:FSG) | 31.8% | 31.6% |

| Velocity Composites (AIM:VEL) | 27.8% | 143.4% |

| B90 Holdings (AIM:B90) | 24.4% | 142.7% |

| Mothercare (AIM:MTC) | 15.1% | 41.2% |

| Judges Scientific (AIM:JDG) | 11.5% | 25.3% |

| Afentra (AIM:AET) | 37.2% | 64.4% |

Let's dive into some prime choices out of from the screener.

Foresight Group Holdings (LSE:FSG)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Foresight Group Holdings Limited is an infrastructure and private equity manager operating across the United Kingdom, Italy, Luxembourg, Ireland, Spain, and Australia, with a market capitalization of approximately £0.59 billion.

Operations: The company generates revenue through three primary segments: Infrastructure (£84.17 million), Private Equity (£47.35 million), and Foresight Capital Management (£9.80 million).

Insider Ownership: 31.8%

Earnings Growth Forecast: 31.6% p.a.

Foresight Group Holdings has demonstrated a strong financial performance with revenue increasing to £141.33 million and net income rising to £26.43 million in FY 2024. The company's earnings are expected to grow significantly, projected at 31.6% annually, outpacing the UK market forecast of 12.5%. Despite a robust return on equity predicted at 48.4%, the dividend coverage remains a concern, as the current yield of 4.37% is not well supported by earnings, indicating potential sustainability issues in its payout policy.

- Click here to discover the nuances of Foresight Group Holdings with our detailed analytical future growth report.

- The valuation report we've compiled suggests that Foresight Group Holdings' current price could be inflated.

Playtech (LSE:PTEC)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Playtech plc is a technology company that offers gambling software, services, content, and platform technologies across the globe, with a market capitalization of approximately £1.49 billion.

Operations: Playtech's revenue is primarily generated from its Gaming B2B and Gaming B2C segments, which reported earnings of €684.10 million and €946.60 million respectively, along with smaller contributions from HAPPYBET and Sun Bingo totaling €91.60 million.

Insider Ownership: 13.5%

Earnings Growth Forecast: 20.6% p.a.

Playtech recently announced a strategic partnership with MGM Resorts, launching live casino content from Las Vegas, enhancing its growth trajectory. Despite trading 55.2% below its estimated fair value and showing a significant earnings increase of 158.9% last year, Playtech's revenue growth is modest at 4% annually. However, earnings are expected to outperform the UK market with a forecasted annual increase of 20.6%. Challenges include low forecasted return on equity at 8.9% and large one-off items impacting financial results.

- Click here and access our complete growth analysis report to understand the dynamics of Playtech.

- Insights from our recent valuation report point to the potential undervaluation of Playtech shares in the market.

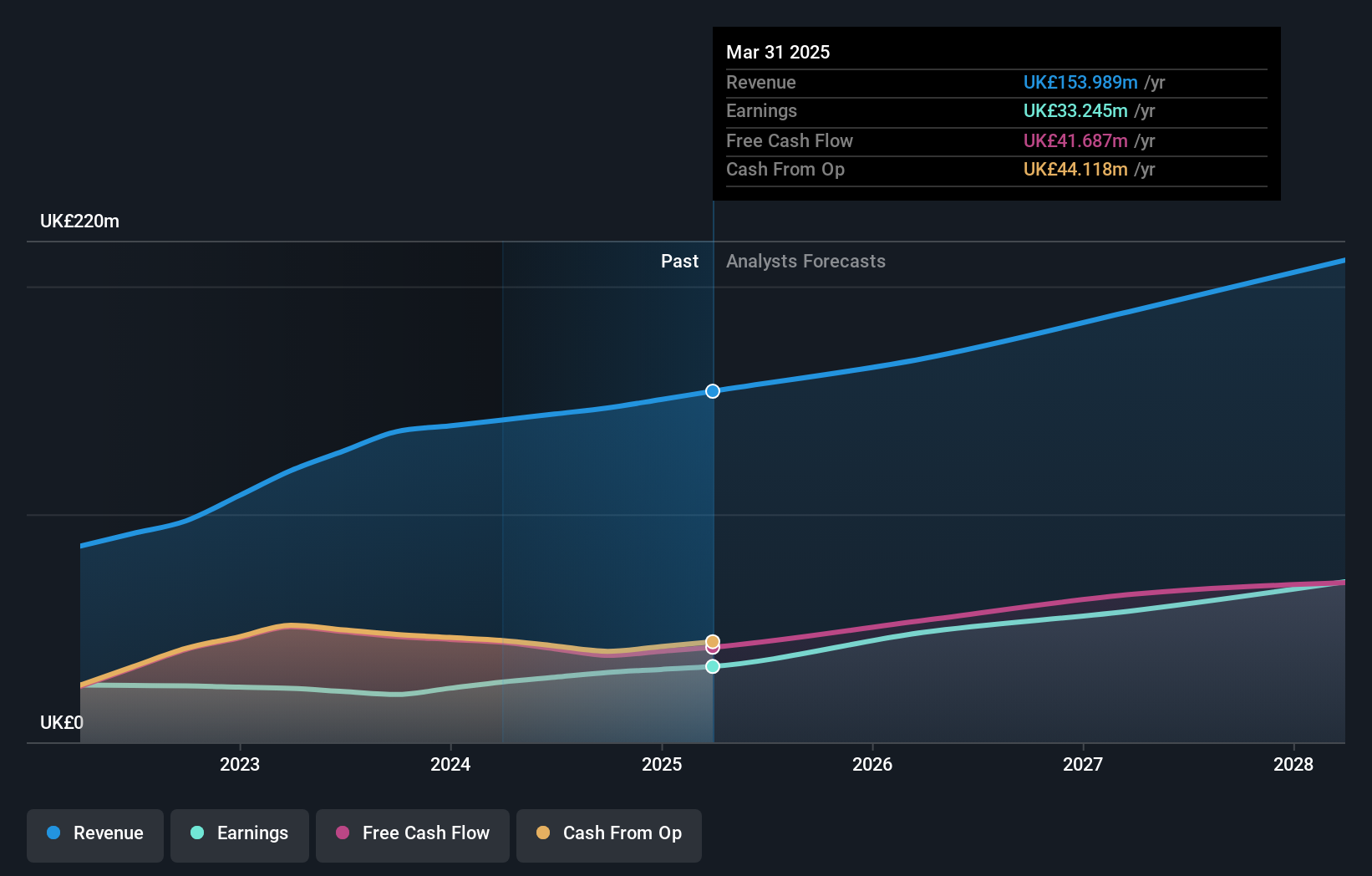

TBC Bank Group (LSE:TBCG)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: TBC Bank Group PLC operates primarily in Georgia, Azerbaijan, and Uzbekistan, offering a range of services including banking, leasing, insurance, brokerage, and card processing to both corporate and individual clients with a market cap of approximately £1.44 billion.

Operations: The company generates its revenue primarily from banking, leasing, insurance, brokerage, and card processing services across Georgia, Azerbaijan, and Uzbekistan.

Insider Ownership: 18%

Earnings Growth Forecast: 15.2% p.a.

TBC Bank Group recently announced a substantial share repurchase program, signaling confidence in its financial health and commitment to shareholder value. In the first quarter of 2024, the bank reported a notable increase in net interest income and net income, reflecting robust operational performance. Despite this positive momentum, TBC Bank is trading at 45% below its estimated fair value and faces challenges such as high volatility in share price and a high level of bad loans at 2.1%. The bank's revenue growth forecast outpaces the UK market average but remains below significant growth thresholds.

- Get an in-depth perspective on TBC Bank Group's performance by reading our analyst estimates report here.

- Our valuation report here indicates TBC Bank Group may be undervalued.

Taking Advantage

- Navigate through the entire inventory of 65 Fast Growing UK Companies With High Insider Ownership here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're helping make it simple.

Find out whether TBC Bank Group is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:TBCG

TBC Bank Group

Through its subsidiaries, provides banking, leasing, insurance, brokerage, and card processing services to corporate and individual customers in Georgia, Azerbaijan, and Uzbekistan.

Undervalued with reasonable growth potential and pays a dividend.