- United Kingdom

- /

- Hospitality

- /

- LSE:CCL

Does Carnival plc's (LON:CCL) P/E Ratio Signal A Buying Opportunity?

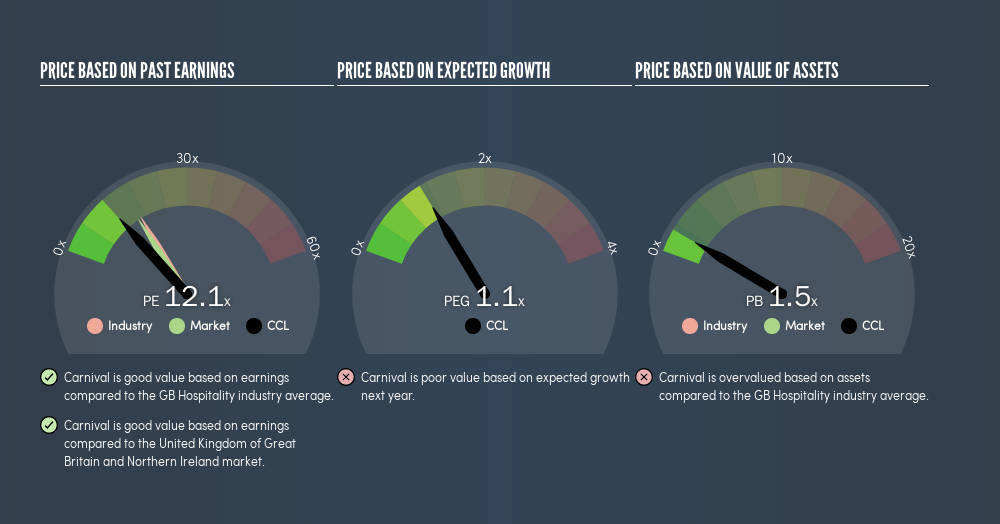

The goal of this article is to teach you how to use price to earnings ratios (P/E ratios). We'll show how you can use Carnival plc's (LON:CCL) P/E ratio to inform your assessment of the investment opportunity. Carnival has a price to earnings ratio of 12.09, based on the last twelve months. That corresponds to an earnings yield of approximately 8.3%.

Check out our latest analysis for Carnival

How Do You Calculate Carnival's P/E Ratio?

The formula for price to earnings is:

Price to Earnings Ratio = Price per Share (in the reporting currency) ÷ Earnings per Share (EPS)

Or for Carnival:

P/E of 12.09 = $53.73 (Note: this is the share price in the reporting currency, namely, USD ) ÷ $4.45 (Based on the trailing twelve months to November 2018.)

Is A High Price-to-Earnings Ratio Good?

A higher P/E ratio implies that investors pay a higher price for the earning power of the business. That is not a good or a bad thing per se, but a high P/E does imply buyers are optimistic about the future.

How Growth Rates Impact P/E Ratios

Probably the most important factor in determining what P/E a company trades on is the earnings growth. When earnings grow, the 'E' increases, over time. That means unless the share price increases, the P/E will reduce in a few years. So while a stock may look expensive based on past earnings, it could be cheap based on future earnings.

It's great to see that Carnival grew EPS by 23% in the last year. And it has bolstered its earnings per share by 25% per year over the last five years. With that performance, you might expect an above average P/E ratio.

How Does Carnival's P/E Ratio Compare To Its Peers?

The P/E ratio essentially measures market expectations of a company. We can see in the image below that the average P/E (16.4) for companies in the hospitality industry is higher than Carnival's P/E.

This suggests that market participants think Carnival will underperform other companies in its industry. While current expectations are low, the stock could be undervalued if the situation is better than the market assumes. It is arguably worth checking if insiders are buying shares, because that might imply they believe the stock is undervalued.

A Limitation: P/E Ratios Ignore Debt and Cash In The Bank

The 'Price' in P/E reflects the market capitalization of the company. That means it doesn't take debt or cash into account. Hypothetically, a company could reduce its future P/E ratio by spending its cash (or taking on debt) to achieve higher earnings.

Such expenditure might be good or bad, in the long term, but the point here is that the balance sheet is not reflected by this ratio.

Is Debt Impacting Carnival's P/E?

Carnival's net debt is 25% of its market cap. This is a reasonably significant level of debt -- all else being equal you'd expect a much lower P/E than if it had net cash.

The Verdict On Carnival's P/E Ratio

Carnival trades on a P/E ratio of 12.1, which is below the GB market average of 15.9. The company does have a little debt, and EPS growth was good last year. The low P/E ratio suggests current market expectations are muted, implying these levels of growth will not continue.

When the market is wrong about a stock, it gives savvy investors an opportunity. If it is underestimating a company, investors can make money by buying and holding the shares until the market corrects itself. So this freevisualization of the analyst consensus on future earnings could help you make the right decision about whether to buy, sell, or hold.

But note: Carnival may not be the best stock to buy. So take a peek at this freelist of interesting companies with strong recent earnings growth (and a P/E ratio below 20).

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About LSE:CCL

Carnival Corporation &

A cruise company, provides leisure travel services in North America, Australia, Europe, and internationally.

Solid track record and good value.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Butler National (Buks) outperforms.

A tech powerhouse quietly powering the world’s AI infrastructure.

Keppel DC REIT (SGX: AJBU) is a resilient gem in the data center space.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)