Taylor Wimpey (LSE:TW.) shares have been on the move lately, catching some attention from investors tracking the UK housebuilding sector. Over the past month, the stock has climbed around 3%, a shift worth watching.

Taylor Wimpey’s 2.6% 1-month share price return may be catching the spotlight, but it comes after a tough stretch. Its year-to-date performance is still down, and the total shareholder return over the past year is a sobering -29.5%. While near-term momentum looks tentative, long-term investors who held on have still seen gains over three and five years as the housing market ebbs and flows.

But after a rough year, with shares still trading well below analyst price targets, is Taylor Wimpey now looking undervalued? Or has the market fully accounted for its future prospects and growth risks?

Advertisement

Most Popular Narrative: 23.9% Undervalued

With Taylor Wimpey's fair value placed at £1.32, well above its latest closing price of £1.00, the market may be underestimating the company's long-term earnings power relative to analyst expectations. The most widely followed narrative suggests that operational strengths and regulatory catalysts set the stage for higher valuations if assumptions prove accurate.

Easing regulatory hurdles and a robust balance sheet enable expansion, increased completions, and sustainable shareholder returns with minimal additional capital needs. Ongoing safety costs, affordability barriers, market competition, planning delays, and mounting build inflation all threaten margins, revenue growth, and long-term earnings.

Curious how analyst expectations stack up against market reality? Shocking growth projections in revenue, profits, and future operating margins drive this valuation. The backbone of this fair value isn't just hope; it's built on ambitious financial targets and long-term industry trends. Want to uncover which numbers spark this optimism? The answer is one click away.

However, persistent affordability challenges and unexpected build cost inflation could quickly undermine even optimistic forecasts. This may limit Taylor Wimpey’s recovery potential.

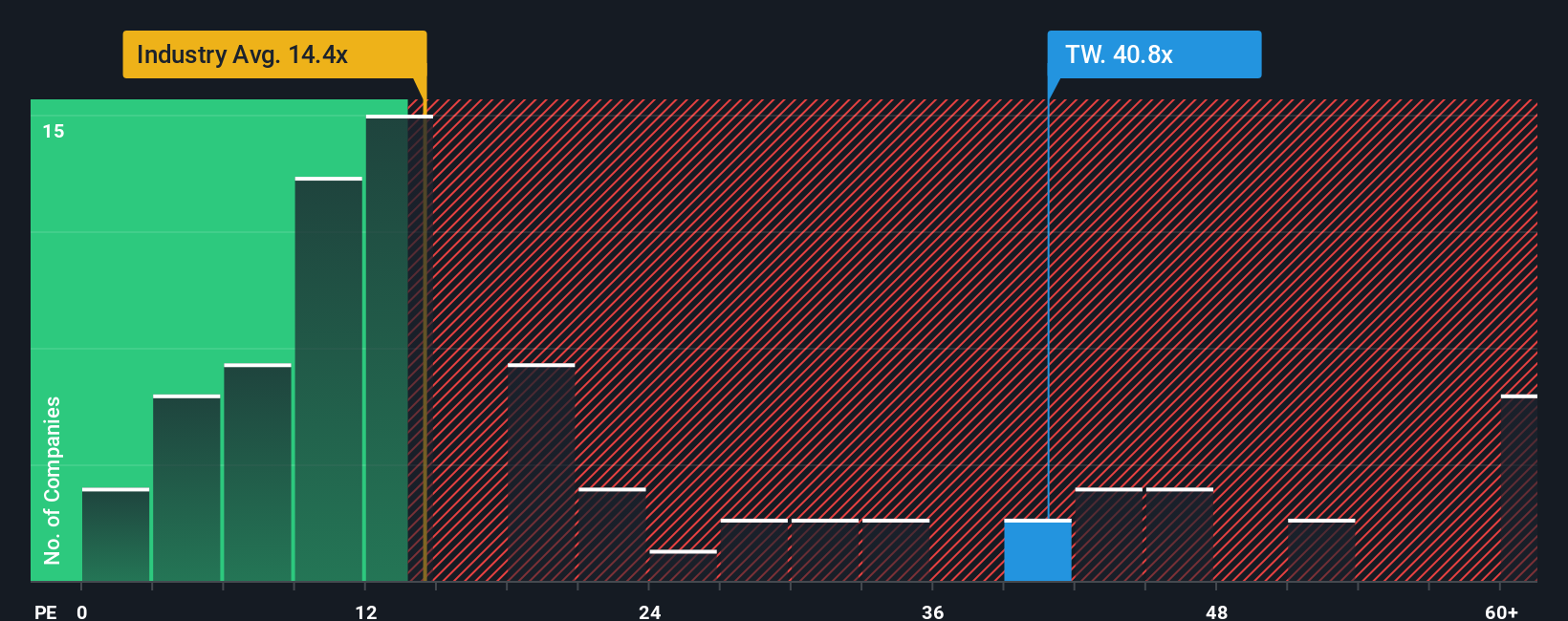

While the analyst narrative points to undervaluation, a closer look at the price-to-earnings ratio paints a different picture. Taylor Wimpey trades at 41.9 times earnings, which is more expensive than both its peer group average of 18 and the European industry average of 14.4. The fair ratio, calculated at 32.8, suggests the market may have priced in more optimism than is justified by fundamentals. Is there a risk the share price could still fall to meet more grounded expectations?

Why settle for the obvious when there are standout opportunities waiting? Level up your strategy with these focused stock shortlists that could put you ahead of the herd.

Spot the potential game-changers in tech by investigating these 24 AI penny stocks, which includes companies at the forefront of artificial intelligence breakthroughs.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Taylor Wimpey might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.