Advertisement

- United Kingdom

- /

- Beverage

- /

- AIM:NICL

3 UK Growth Companies With High Insider Ownership Expecting Up To 25% Earnings Growth

Simply Wall St

Reviewed by Simply Wall St

In the current climate, the UK market is grappling with challenges as evidenced by recent declines in the FTSE 100 and FTSE 250 indices, largely influenced by weak trade data from China that has impacted global sentiment. Amid these fluctuations, investors often look for companies with strong growth potential and high insider ownership, as these factors can indicate alignment of interests between management and shareholders and a commitment to long-term success.

Top 10 Growth Companies With High Insider Ownership In The United Kingdom

| Name | Insider Ownership | Earnings Growth |

| Gulf Keystone Petroleum (LSE:GKP) | 12.2% | 102.1% |

| Helios Underwriting (AIM:HUW) | 23.9% | 23.1% |

| LSL Property Services (LSE:LSL) | 10.4% | 26.9% |

| Judges Scientific (AIM:JDG) | 10.7% | 29.3% |

| Facilities by ADF (AIM:ADF) | 13.2% | 161.5% |

| Mortgage Advice Bureau (Holdings) (AIM:MAB1) | 19.8% | 25.4% |

| B90 Holdings (AIM:B90) | 24.4% | 166.8% |

| Getech Group (AIM:GTC) | 11.8% | 114.5% |

| Audioboom Group (AIM:BOOM) | 27.8% | 175% |

| Anglo Asian Mining (AIM:AAZ) | 40% | 116.2% |

Let's explore several standout options from the results in the screener.

Mortgage Advice Bureau (Holdings) (AIM:MAB1)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Mortgage Advice Bureau (Holdings) plc, along with its subsidiaries, offers mortgage advice services across the United Kingdom and has a market cap of £433.52 million.

Operations: The company generates revenue of £243.31 million from its provision of financial services segment in the United Kingdom.

Insider Ownership: 19.8%

Earnings Growth Forecast: 25.4% p.a.

Mortgage Advice Bureau (Holdings) plc demonstrates strong growth potential with high insider ownership, evidenced by impressive revenue growth of 11% to approximately £266 million for 2024, surpassing UK gross lending growth. Earnings are forecast to grow significantly at 25.38% annually, outpacing the UK market's average. Despite a volatile share price and a dividend not well-covered by earnings, recent insider buying indicates confidence in future prospects. Upcoming board changes may influence strategic direction.

- Click here to discover the nuances of Mortgage Advice Bureau (Holdings) with our detailed analytical future growth report.

- Our comprehensive valuation report raises the possibility that Mortgage Advice Bureau (Holdings) is priced higher than what may be justified by its financials.

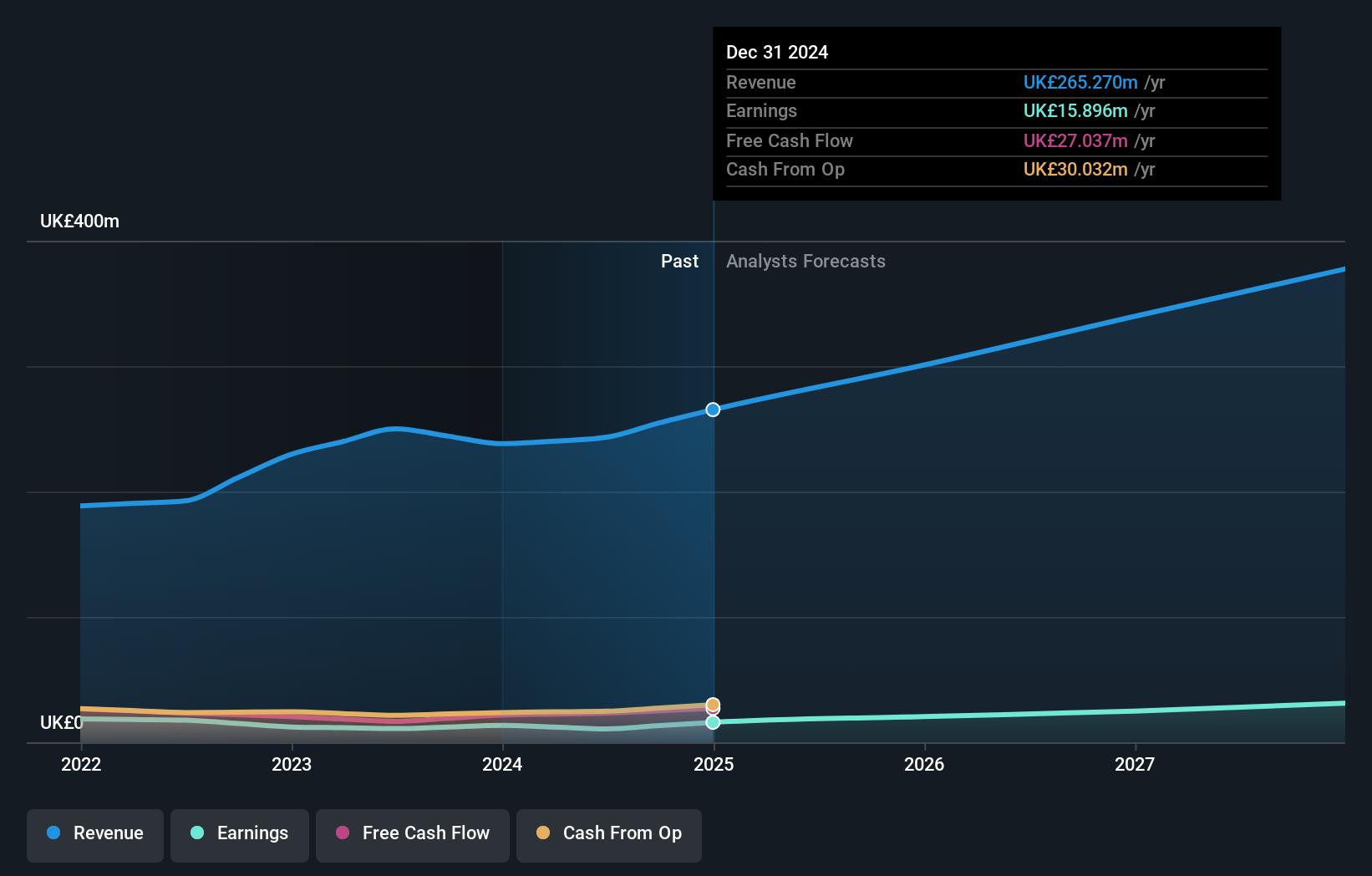

Nichols (AIM:NICL)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Nichols plc, with a market cap of £485.85 million, supplies soft drinks to the retail, wholesale, catering, licensed, and leisure industries across the United Kingdom, the Middle East, Africa, and internationally.

Operations: The company's revenue segments include £132.82 million from Packaged soft drinks and £39.99 million from Out of Home sales.

Insider Ownership: 27.7%

Earnings Growth Forecast: 14.8% p.a.

Nichols plc, with substantial insider ownership, shows potential for growth despite a slight dip in net income to £17.84 million for 2024. Revenue is expected to grow at 3.9% annually, slightly above the UK market average. Earnings are forecasted to increase by 14.8% per year, indicating robust future prospects. Recent board changes and an increased final dividend of 17.1p per share reflect strategic confidence and strong cash generation amidst a challenging earnings environment.

- Delve into the full analysis future growth report here for a deeper understanding of Nichols.

- The valuation report we've compiled suggests that Nichols' current price could be inflated.

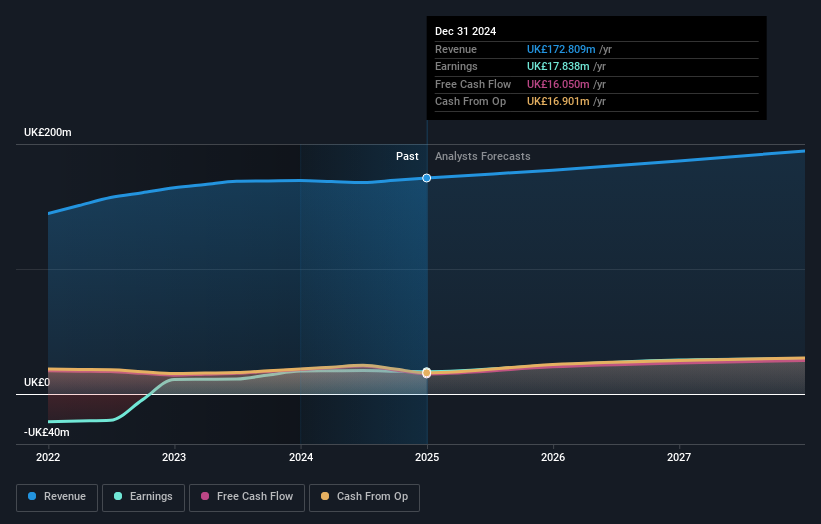

MJ Gleeson (LSE:GLE)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: MJ Gleeson plc operates in the United Kingdom, focusing on house building and land promotion and sales, with a market cap of £272.30 million.

Operations: The company's revenue is derived from two primary segments: Gleeson Land, contributing £8.40 million, and Gleeson Homes, generating £343.33 million.

Insider Ownership: 11.2%

Earnings Growth Forecast: 20.3% p.a.

MJ Gleeson, benefiting from significant insider buying, is positioned for growth with earnings expected to rise 20.3% annually, outpacing the UK market. While revenue growth at 12.5% per year lags behind the desired 20%, it still surpasses market averages. Despite a declining net income of £2.8 million for H1 2025 compared to £5.59 million in the previous year, analysts predict a stock price increase of over 40%. The dividend remains stable at 4 pence per share amidst an unstable track record.

- Click to explore a detailed breakdown of our findings in MJ Gleeson's earnings growth report.

- Our expertly prepared valuation report MJ Gleeson implies its share price may be lower than expected.

Where To Now?

- Click through to start exploring the rest of the 59 Fast Growing UK Companies With High Insider Ownership now.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Nichols might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About AIM:NICL

Nichols

Engages in supply of soft drinks to the retail, wholesale, catering, licensed, and leisure industries in the United Kingdom, the Middle East, Africa, and internationally.

Flawless balance sheet, good value and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

BL

BlackGoat on Alphabet ·

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value:US$324.481.3% undervalued

75 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6926.7% undervalued

44 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8147.4% undervalued

9 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

89 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

926 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative