- United Kingdom

- /

- Consumer Durables

- /

- AIM:SDG

Despite lower earnings than five years ago, Sanderson Design Group (LON:SDG) investors are up 43% since then

It's been a soft week for Sanderson Design Group plc (LON:SDG) shares, which are down 14%. On the bright side the returns have been quite good over the last half decade. It has returned a market beating 29% in that time.

While the stock has fallen 14% this week, it's worth focusing on the longer term and seeing if the stocks historical returns have been driven by the underlying fundamentals.

Check out our latest analysis for Sanderson Design Group

While markets are a powerful pricing mechanism, share prices reflect investor sentiment, not just underlying business performance. One way to examine how market sentiment has changed over time is to look at the interaction between a company's share price and its earnings per share (EPS).

During five years of share price growth, Sanderson Design Group actually saw its EPS drop 4.5% per year.

So it's hard to argue that the earnings per share are the best metric to judge the company, as it may not be optimized for profits at this point. Since the change in EPS doesn't seem to correlate with the change in share price, it's worth taking a look at other metrics.

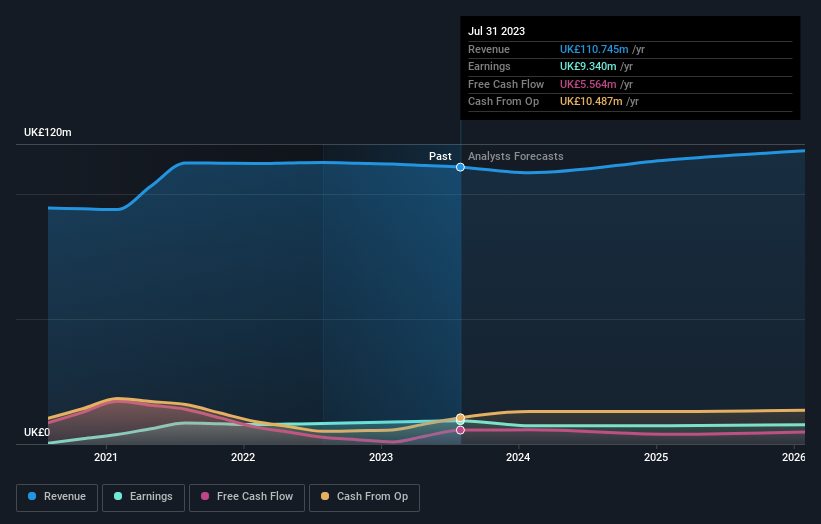

We are not particularly impressed by the annual compound revenue growth of 0.1% over five years. So it seems one might have to take closer look at earnings and revenue trends to see how they might influence the share price.

The image below shows how earnings and revenue have tracked over time (if you click on the image you can see greater detail).

It is of course excellent to see how Sanderson Design Group has grown profits over the years, but the future is more important for shareholders. Take a more thorough look at Sanderson Design Group's financial health with this free report on its balance sheet.

What About Dividends?

It is important to consider the total shareholder return, as well as the share price return, for any given stock. The TSR is a return calculation that accounts for the value of cash dividends (assuming that any dividend received was reinvested) and the calculated value of any discounted capital raisings and spin-offs. Arguably, the TSR gives a more comprehensive picture of the return generated by a stock. As it happens, Sanderson Design Group's TSR for the last 5 years was 43%, which exceeds the share price return mentioned earlier. And there's no prize for guessing that the dividend payments largely explain the divergence!

A Different Perspective

While the broader market lost about 1.7% in the twelve months, Sanderson Design Group shareholders did even worse, losing 7.2% (even including dividends). Having said that, it's inevitable that some stocks will be oversold in a falling market. The key is to keep your eyes on the fundamental developments. On the bright side, long term shareholders have made money, with a gain of 7% per year over half a decade. If the fundamental data continues to indicate long term sustainable growth, the current sell-off could be an opportunity worth considering. It's always interesting to track share price performance over the longer term. But to understand Sanderson Design Group better, we need to consider many other factors. To that end, you should learn about the 3 warning signs we've spotted with Sanderson Design Group (including 1 which is concerning) .

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of companies we expect will grow earnings.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on British exchanges.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About AIM:SDG

Sanderson Design Group

Engages in the design, manufacture, marketing, and distribution of interior furnishings, fabrics, and wallpapers worldwide.

Flawless balance sheet, undervalued and pays a dividend.