- United Kingdom

- /

- Commercial Services

- /

- AIM:FRAN

UK Growth Companies With High Insider Ownership For August 2024

Reviewed by Simply Wall St

The United Kingdom market has faced recent turbulence, with the FTSE 100 index closing lower amid weak trade data from China and global economic uncertainties. In such a volatile environment, growth companies with high insider ownership can offer a compelling investment proposition, as they often demonstrate strong internal confidence and alignment of interests between management and shareholders.

Top 10 Growth Companies With High Insider Ownership In The United Kingdom

| Name | Insider Ownership | Earnings Growth |

| Filtronic (AIM:FTC) | 28.6% | 34% |

| Plant Health Care (AIM:PHC) | 34.2% | 121.3% |

| Gulf Keystone Petroleum (LSE:GKP) | 12.1% | 74.6% |

| Integrated Diagnostics Holdings (LSE:IDHC) | 26.7% | 23.5% |

| Foresight Group Holdings (LSE:FSG) | 31.9% | 27.9% |

| Helios Underwriting (AIM:HUW) | 23.9% | 14.7% |

| LSL Property Services (LSE:LSL) | 10.8% | 33.3% |

| Belluscura (AIM:BELL) | 39.5% | 117.8% |

| Velocity Composites (AIM:VEL) | 27.6% | 173.3% |

| Hochschild Mining (LSE:HOC) | 38.4% | 53.8% |

Let's dive into some prime choices out of the screener.

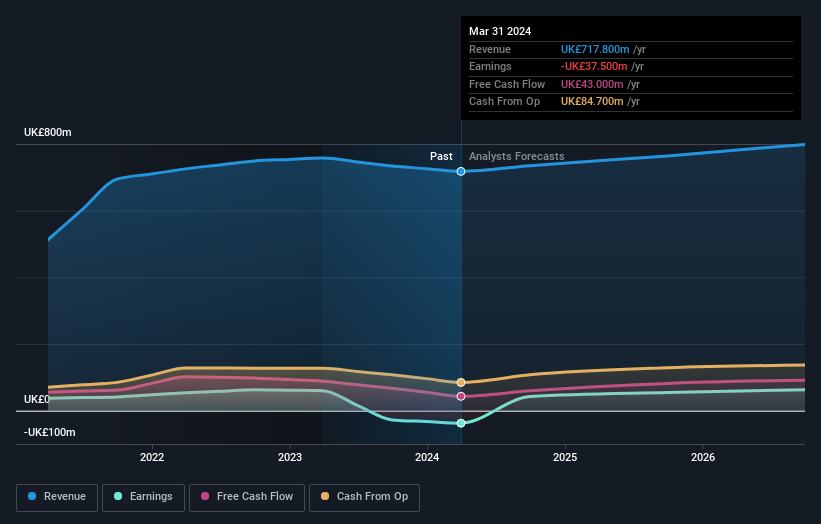

Franchise Brands (AIM:FRAN)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Franchise Brands plc, with a market cap of £348.88 million, operates in franchising and related activities across the United Kingdom, North America, and Europe through its subsidiaries.

Operations: The company's revenue segments (in millions of £) include Azura: 0.75, Pirtek: 41.95, B2C Division: 6.11, Water & Waste: 48.88, and Filta International: 27.12.

Insider Ownership: 29.8%

Franchise Brands, a growth company with high insider ownership in the UK, is forecast to achieve significant annual earnings growth of 40.7% over the next three years. Its revenue is expected to grow at 11.5% annually, outpacing the broader UK market's 3.6%. Recently, there has been substantial insider buying and no significant insider selling over the past three months. However, profit margins have decreased from 11.6% last year to 2.5%.

- Delve into the full analysis future growth report here for a deeper understanding of Franchise Brands.

- Our comprehensive valuation report raises the possibility that Franchise Brands is priced lower than what may be justified by its financials.

RWS Holdings (AIM:RWS)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: RWS Holdings plc offers technology-enabled language, content, and intellectual property (IP) services and has a market cap of £673.22 million.

Operations: The company's revenue segments in millions of £ are: IP Services: 105.10, Language Services: 325.40, Regulated Industry: 149.40, and Language & Content Technology (L&CT): 137.90.

Insider Ownership: 24.6%

RWS Holdings, with significant insider ownership, has recently launched Trados Studio 2024 and enhanced Tridion Docs with AI features. Despite a decline in half-year earnings to £11.1 million from £20.9 million, the company forecasts annual profit growth of 67.35% and revenue growth at 4.2%, surpassing the UK market's average. The stock trades significantly below its estimated fair value, though its dividend sustainability is questionable due to low coverage by earnings or free cash flows.

- Unlock comprehensive insights into our analysis of RWS Holdings stock in this growth report.

- Insights from our recent valuation report point to the potential undervaluation of RWS Holdings shares in the market.

M&C Saatchi (AIM:SAA)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: M&C Saatchi plc provides advertising and marketing communications services across the United Kingdom, Europe, the Middle East, Africa, the Asia Pacific, and the Americas with a market cap of £259.19 million.

Operations: The company's revenue segments include advertising and marketing communications services in the United Kingdom, Europe, the Middle East, Africa, the Asia Pacific, and the Americas.

Insider Ownership: 16.2%

M&C Saatchi, with substantial insider ownership, is forecast to achieve profitability within three years and has a very high projected Return on Equity of 45.5%. However, revenue is expected to decline by 14.2% annually over the same period. Recent executive changes include Simon Fuller joining as CFO and Board member on July 1, 2024. The stock trades at a significant discount to its estimated fair value despite these challenges and strategic shifts.

- Click to explore a detailed breakdown of our findings in M&C Saatchi's earnings growth report.

- According our valuation report, there's an indication that M&C Saatchi's share price might be on the cheaper side.

Key Takeaways

- Click here to access our complete index of 65 Fast Growing UK Companies With High Insider Ownership.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About AIM:FRAN

Franchise Brands

Through its subsidiaries, engages in franchising and related activities in the United Kingdom, North America, and rest of Europe.

Good value with proven track record.