Advertisement

- United Kingdom

- /

- Media

- /

- AIM:SAA

UK Growth Stocks Insiders Are Backing

Simply Wall St

Reviewed by Simply Wall St

As the UK market grapples with global economic headwinds, notably from China's faltering trade data impacting the FTSE 100, investors are keenly observing how these challenges affect growth prospects. In such uncertain times, stocks with high insider ownership can be particularly appealing as they often indicate that company executives have confidence in their business's long-term potential.

Top 10 Growth Companies With High Insider Ownership In The United Kingdom

| Name | Insider Ownership | Earnings Growth |

| Gulf Keystone Petroleum (LSE:GKP) | 12.2% | 102.1% |

| Helios Underwriting (AIM:HUW) | 23.8% | 23.1% |

| Judges Scientific (AIM:JDG) | 10.7% | 29.3% |

| Facilities by ADF (AIM:ADF) | 13.2% | 161.5% |

| Mortgage Advice Bureau (Holdings) (AIM:MAB1) | 19.8% | 25.4% |

| B90 Holdings (AIM:B90) | 24.4% | 166.8% |

| Getech Group (AIM:GTC) | 11.8% | 114.5% |

| Audioboom Group (AIM:BOOM) | 31.4% | 175% |

| Faron Pharmaceuticals Oy (AIM:FARN) | 25.1% | 26.8% |

| Anglo Asian Mining (AIM:AAZ) | 40% | 116.2% |

Let's take a closer look at a couple of our picks from the screened companies.

Craneware (AIM:CRW)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Craneware plc, along with its subsidiaries, develops, licenses, and supports computer software for the healthcare industry in the United States and has a market cap of £619.82 million.

Operations: Craneware plc generates revenue by developing, licensing, and supporting healthcare industry software in the United States.

Insider Ownership: 16.6%

Earnings Growth Forecast: 23.9% p.a.

Craneware plc, with significant insider ownership, reported strong half-year results with sales reaching US$100.05 million and net income rising to US$7.24 million. The company forecasts earnings growth of 23.9% annually, outpacing the UK market's 14.2%. Despite slower revenue growth at 8.1%, it still exceeds the UK's average of 3.8%. Recent leadership changes include appointing Susan Nelson as a Non-Executive Director, enhancing strategic direction in healthcare finance expertise.

- Click here to discover the nuances of Craneware with our detailed analytical future growth report.

- Our comprehensive valuation report raises the possibility that Craneware is priced higher than what may be justified by its financials.

Fintel (AIM:FNTL)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Fintel Plc provides intermediary services and distribution channels to the retail financial services sector in the United Kingdom, with a market cap of £290.70 million.

Operations: The company's revenue is derived from three segments: Research & Fintech (£24.20 million), Distribution Channels (£21.40 million), and Intermediary Services (£23.30 million).

Insider Ownership: 29.2%

Earnings Growth Forecast: 31.7% p.a.

Fintel Plc, with high insider ownership and recent substantial insider buying, is undergoing leadership changes as Matt Timmins becomes sole CEO. The company's revenue is expected to grow at 7.5% annually, surpassing the UK market average of 3.8%, though slower than high-growth benchmarks. Earnings are forecast to increase significantly by 31.7% per year, outpacing the UK market's growth rate of 14.2%. However, profit margins have declined from last year’s figures.

- Click to explore a detailed breakdown of our findings in Fintel's earnings growth report.

- Our expertly prepared valuation report Fintel implies its share price may be too high.

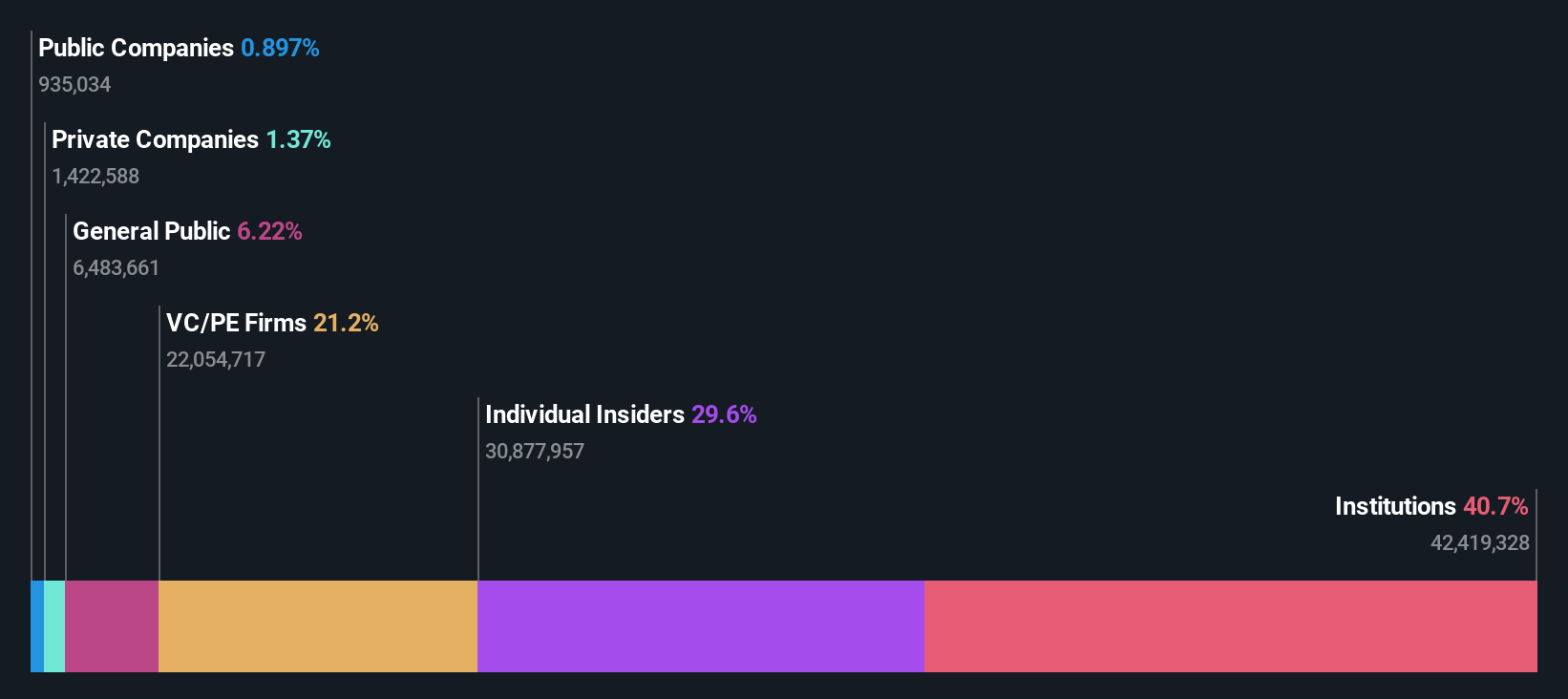

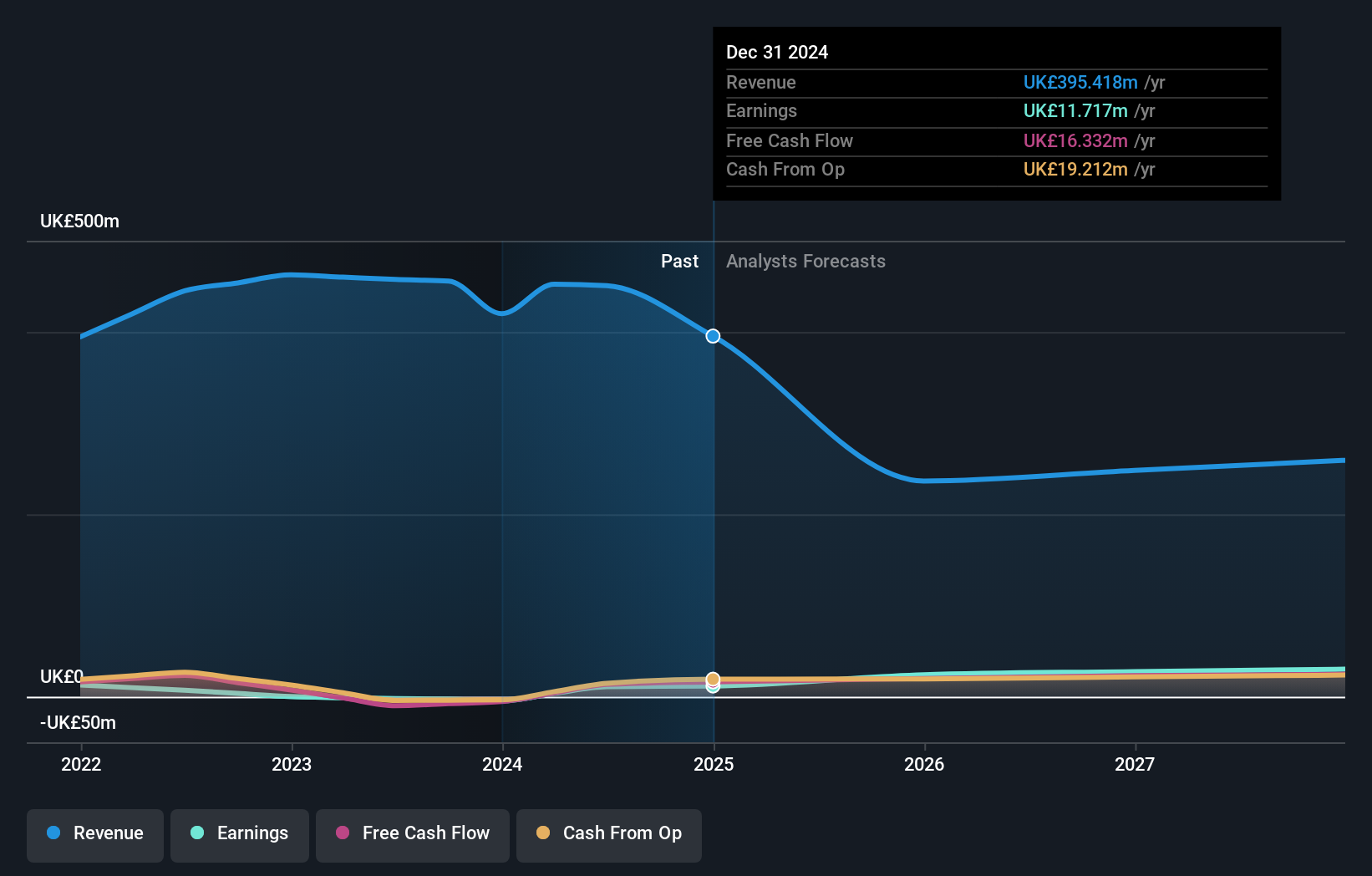

M&C Saatchi (AIM:SAA)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: M&C Saatchi plc offers advertising and marketing communications services across the UK, Europe, the Middle East, Africa, the Asia Pacific, and the Americas with a market cap of £202.95 million.

Operations: M&C Saatchi plc generates revenue through its advertising and marketing communications services across diverse regions, including the UK, Europe, the Middle East, Africa, the Asia Pacific, and the Americas.

Insider Ownership: 15.5%

Earnings Growth Forecast: 27.4% p.a.

M&C Saatchi, with significant insider ownership, has become profitable this year and is trading at a substantial discount to its estimated fair value. Despite an expected annual revenue decline of 15.4% over the next three years, earnings are forecast to grow significantly at 27.45% annually, surpassing UK market averages. Recent guidance indicates organic sales growth of 12%-16% for 2025 with EBIT growth exceeding sales projections, supported by efficiency programs and diverse portfolio strength.

- Delve into the full analysis future growth report here for a deeper understanding of M&C Saatchi.

- In light of our recent valuation report, it seems possible that M&C Saatchi is trading behind its estimated value.

Where To Now?

- Navigate through the entire inventory of 62 Fast Growing UK Companies With High Insider Ownership here.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About AIM:SAA

M&C Saatchi

Provides advertising and marketing communications services in the United Kingdom, Europe, the Middle East, the Asia Pacific, and the Americas.

Flawless balance sheet and good value.

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|26.3% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|4.8% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor