- United Kingdom

- /

- Professional Services

- /

- LSE:ELIX

Elixirr International And 2 Promising Small Caps With Strong Potential

Reviewed by Simply Wall St

As the United Kingdom's FTSE 100 index faces pressure from global economic challenges, particularly the sluggish recovery in China, investors are increasingly turning their attention to small-cap stocks for potential opportunities. In this environment, identifying companies with strong fundamentals and growth prospects becomes essential, making Elixirr International and two other promising small caps intriguing options for those exploring untapped potential in the UK market.

Top 10 Undiscovered Gems With Strong Fundamentals In The United Kingdom

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| B.P. Marsh & Partners | NA | 29.42% | 31.34% | ★★★★★★ |

| BioPharma Credit | NA | 7.22% | 7.91% | ★★★★★★ |

| Rights and Issues Investment Trust | NA | -7.87% | -8.41% | ★★★★★★ |

| Livermore Investments Group | NA | 9.92% | 13.65% | ★★★★★★ |

| MS INTERNATIONAL | NA | 13.42% | 56.55% | ★★★★★★ |

| Andrews Sykes Group | NA | 2.15% | 4.93% | ★★★★★★ |

| London Security | 0.22% | 10.13% | 7.75% | ★★★★★★ |

| Goodwin | 37.02% | 9.75% | 15.68% | ★★★★★☆ |

| FW Thorpe | 2.95% | 11.79% | 13.49% | ★★★★★☆ |

| AltynGold | 77.07% | 28.64% | 38.10% | ★★★★☆☆ |

Let's uncover some gems from our specialized screener.

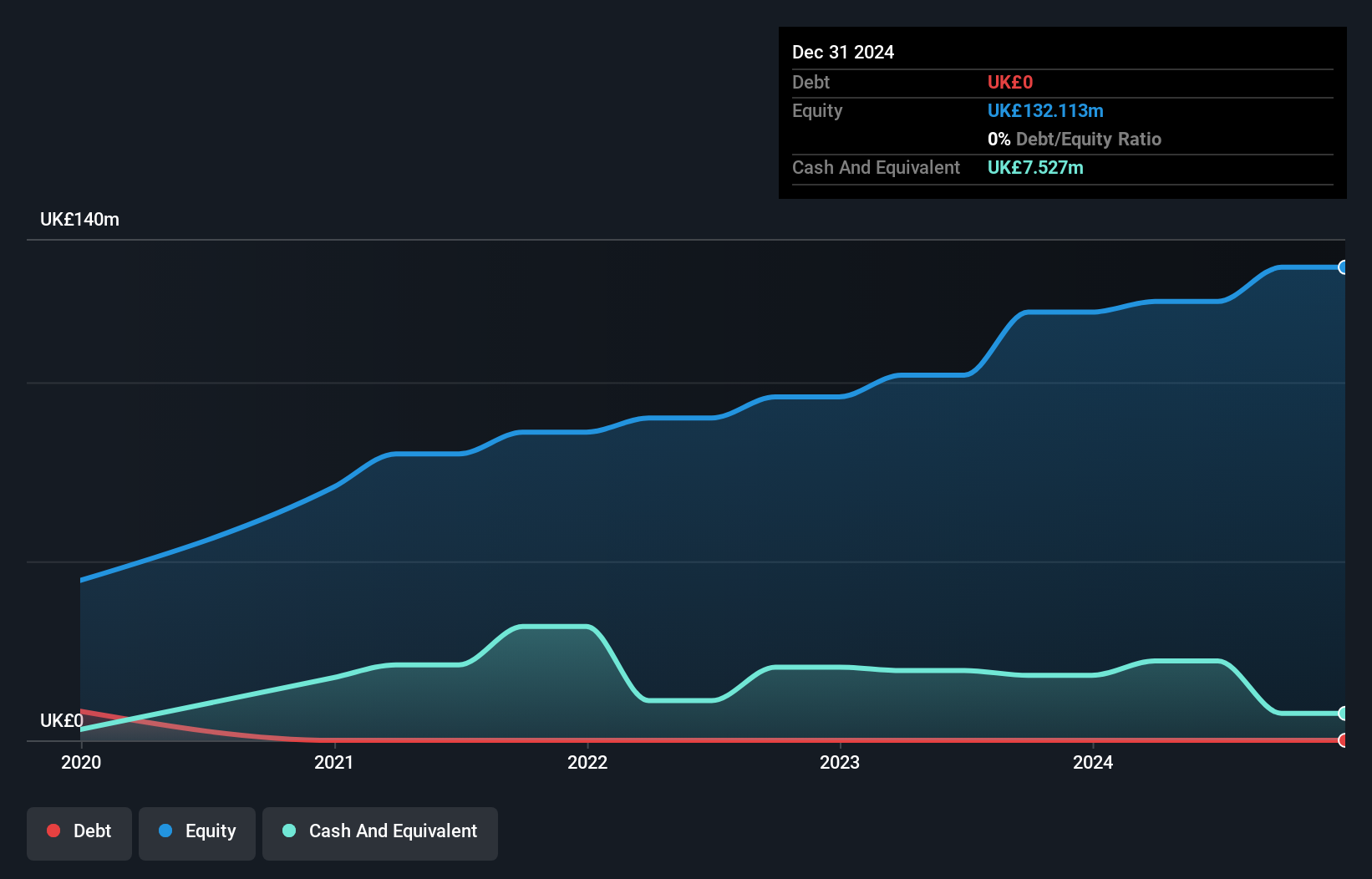

Elixirr International (AIM:ELIX)

Simply Wall St Value Rating: ★★★★★★

Overview: Elixirr International plc is a management consultancy firm operating through its subsidiaries in the United Kingdom, the United States, and internationally, with a market capitalization of £280.88 million.

Operations: Elixirr generates revenue primarily from management consulting services, amounting to £97.37 million. The company operates with a focus on optimizing its financial performance, reflected in its gross profit margin trends over time.

Elixirr International's recent earnings growth of 32.8% outpaces the Professional Services industry's 4.7%, reflecting its strong market position and strategic focus on AI and organizational transformation. Trading at 67.7% below estimated fair value, Elixirr appears undervalued compared to peers, with no debt burden enhancing its financial flexibility. Despite significant insider selling recently, the company’s robust acquisition strategy, including Insigniam, expands its U.S. presence and service offerings across 13 sectors. Analysts forecast a revenue increase of 18.2% annually over three years but expect profit margins to dip from 18.9% to 16.1%.

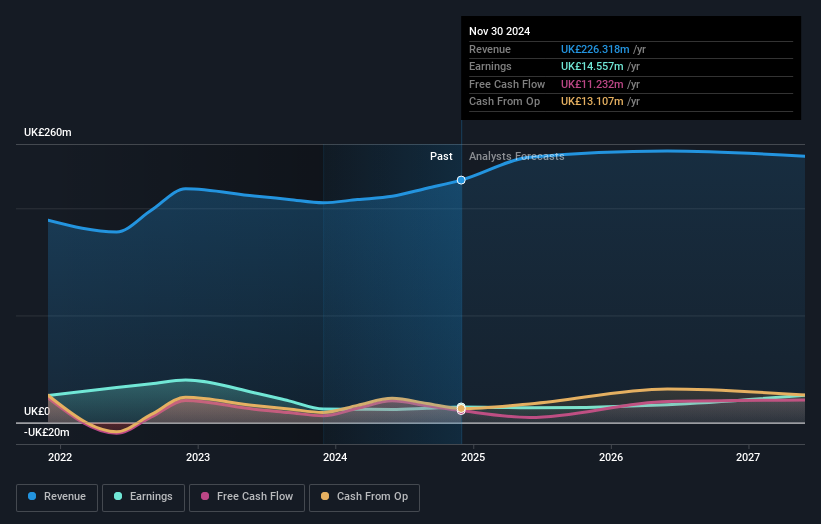

Hargreaves Services (AIM:HSP)

Simply Wall St Value Rating: ★★★★★★

Overview: Hargreaves Services Plc is a company that offers environmental and industrial services across the United Kingdom, Europe, Hong Kong, and other international markets with a market cap of £195.79 million.

Operations: The company's primary revenue stream is derived from its services segment, generating £219.11 million, while Hargreaves Land contributes £10.54 million. The net profit margin is an important indicator to consider when evaluating overall profitability and operational efficiency.

Hargreaves Services, a smaller player in the UK market, has demonstrated robust financial performance with earnings growth of 15% over the past year, outpacing its industry peers. Trading at nearly 55% below its estimated fair value, it presents a potential investment opportunity. The company is debt-free now compared to five years ago when its debt-to-equity ratio was 38.2%, enhancing financial stability. Recent results show a significant increase in net income to £3.99 million from £1.71 million last year, alongside an interim dividend rise to 18.5 pence per share from 18 pence previously declared for shareholders on April 8th, 2025.

- Click here to discover the nuances of Hargreaves Services with our detailed analytical health report.

Gain insights into Hargreaves Services' past trends and performance with our Past report.

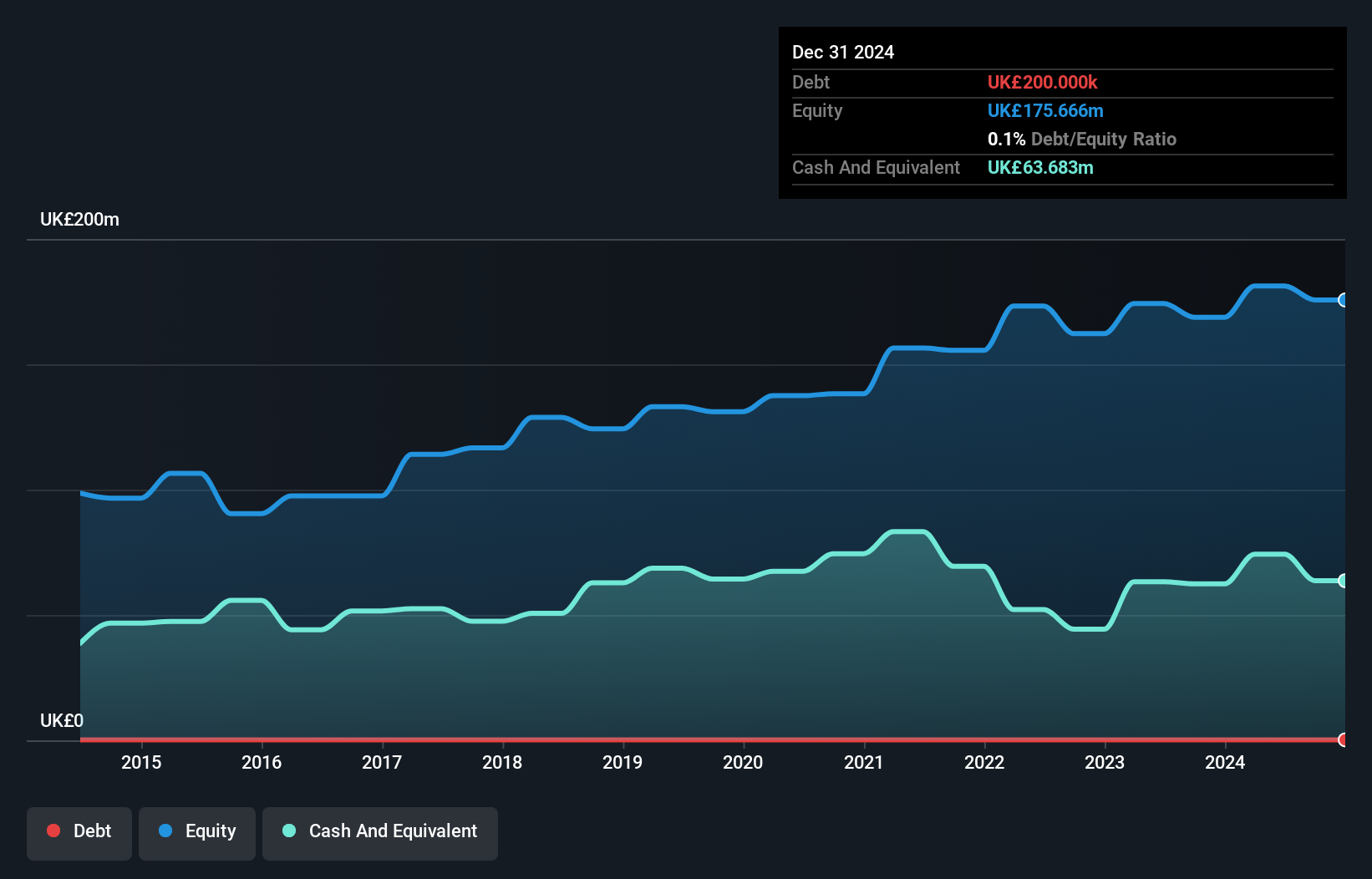

James Halstead (AIM:JHD)

Simply Wall St Value Rating: ★★★★★★

Overview: James Halstead plc is a company that manufactures and supplies flooring products for commercial and domestic uses across various regions including the United Kingdom, Europe, Scandinavia, Australasia, Asia, and internationally with a market cap of £579.33 million.

Operations: The primary revenue stream for James Halstead comes from the manufacture and distribution of flooring products, generating £268.52 million.

James Halstead, a flooring specialist in the UK, offers an intriguing blend of stability and potential. Despite sales dipping to £130.09 million from £136.45 million last year, net income rose slightly to £20.97 million. The company has reduced its debt-to-equity ratio from 0.2 to 0.1 over five years, indicating improved financial health and boasts high-quality earnings with positive free cash flow of £46.41 million as of June 2023. Trading at a discount of 16% below fair value estimates adds appeal for investors seeking undervalued opportunities while maintaining robust interest coverage suggests sound financial management practices are in place.

- Delve into the full analysis health report here for a deeper understanding of James Halstead.

Understand James Halstead's track record by examining our Past report.

Next Steps

- Explore the 61 names from our UK Undiscovered Gems With Strong Fundamentals screener here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Elixirr International might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:ELIX

Elixirr International

Through its subsidiaries, provides management consultancy services in the United Kingdom, the United States, and internationally.

High growth potential and good value.

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Clarivate Stock: When Data Becomes the Backbone of Innovation and Law

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

MicroVision will explode future revenue by 380.37% with a vision towards success

Trending Discussion