- United Kingdom

- /

- Aerospace & Defense

- /

- LSE:MRO

Melrose Industries (LON:MRO) Has A Pretty Healthy Balance Sheet

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. Importantly, Melrose Industries PLC (LON:MRO) does carry debt. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first step when considering a company's debt levels is to consider its cash and debt together.

See our latest analysis for Melrose Industries

How Much Debt Does Melrose Industries Carry?

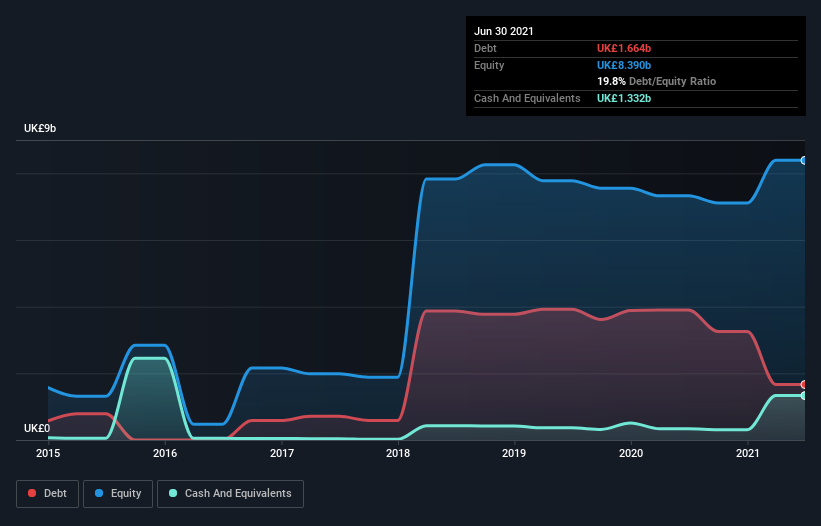

The image below, which you can click on for greater detail, shows that Melrose Industries had debt of UK£1.66b at the end of June 2021, a reduction from UK£3.90b over a year. However, it also had UK£1.33b in cash, and so its net debt is UK£332.0m.

How Strong Is Melrose Industries' Balance Sheet?

The latest balance sheet data shows that Melrose Industries had liabilities of UK£2.84b due within a year, and liabilities of UK£4.21b falling due after that. Offsetting these obligations, it had cash of UK£1.33b as well as receivables valued at UK£1.33b due within 12 months. So it has liabilities totalling UK£4.38b more than its cash and near-term receivables, combined.

Melrose Industries has a very large market capitalization of UK£7.61b, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Melrose Industries has a very low debt to EBITDA ratio of 0.31 so it is strange to see weak interest coverage, with last year's EBIT being only 1.0 times the interest expense. So while we're not necessarily alarmed we think that its debt is far from trivial. Notably, Melrose Industries made a loss at the EBIT level, last year, but improved that to positive EBIT of UK£197m in the last twelve months. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Melrose Industries's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So it is important to check how much of its earnings before interest and tax (EBIT) converts to actual free cash flow. Over the last year, Melrose Industries actually produced more free cash flow than EBIT. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Our View

Melrose Industries's interest cover was a real negative on this analysis, although the other factors we considered were considerably better. There's no doubt that its ability to to convert EBIT to free cash flow is pretty flash. Looking at all this data makes us feel a little cautious about Melrose Industries's debt levels. While debt does have its upside in higher potential returns, we think shareholders should definitely consider how debt levels might make the stock more risky. We'd be motivated to research the stock further if we found out that Melrose Industries insiders have bought shares recently. If you would too, then you're in luck, since today we're sharing our list of reported insider transactions for free.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About LSE:MRO

Melrose Industries

Provides aerospace components and systems to civil and defence markets in the United Kingdom, rest of Europe, North America, and internationally.

Reasonable growth potential with mediocre balance sheet.