- United Kingdom

- /

- Building

- /

- LSE:ECEL

UK Dividend Stocks To Consider In March 2025

Reviewed by Simply Wall St

As the UK market grapples with the ripple effects of weak trade data from China, evidenced by recent declines in the FTSE 100 and FTSE 250 indices, investors are increasingly looking for stability amid global economic uncertainties. In such a climate, dividend stocks can offer a reliable income stream and potential resilience against market volatility, making them an attractive consideration for those seeking steady returns.

Top 10 Dividend Stocks In The United Kingdom

| Name | Dividend Yield | Dividend Rating |

| WPP (LSE:WPP) | 6.44% | ★★★★★★ |

| Man Group (LSE:EMG) | 6.34% | ★★★★★☆ |

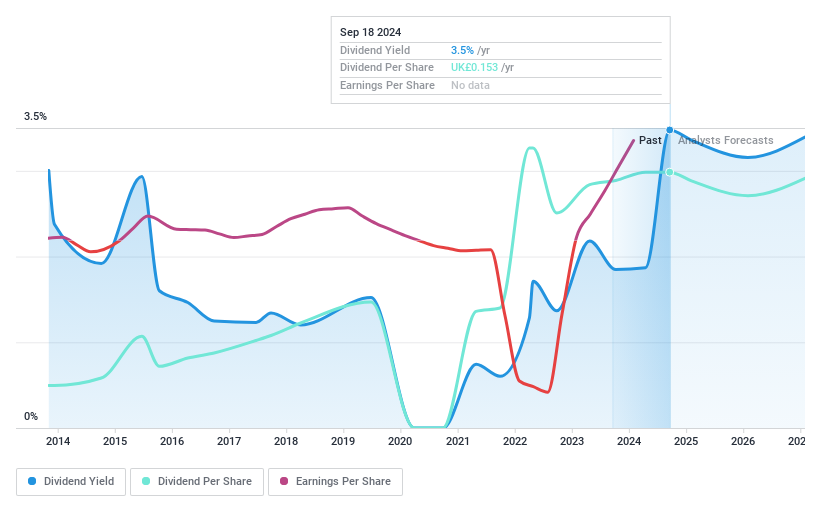

| Keller Group (LSE:KLR) | 3.49% | ★★★★★☆ |

| 4imprint Group (LSE:FOUR) | 4.70% | ★★★★★☆ |

| Grafton Group (LSE:GFTU) | 4.23% | ★★★★★☆ |

| DCC (LSE:DCC) | 3.82% | ★★★★★☆ |

| Big Yellow Group (LSE:BYG) | 4.88% | ★★★★★☆ |

| OSB Group (LSE:OSB) | 7.35% | ★★★★★☆ |

| NWF Group (AIM:NWF) | 4.71% | ★★★★★☆ |

| James Latham (AIM:LTHM) | 7.78% | ★★★★★☆ |

Click here to see the full list of 56 stocks from our Top UK Dividend Stocks screener.

Let's review some notable picks from our screened stocks.

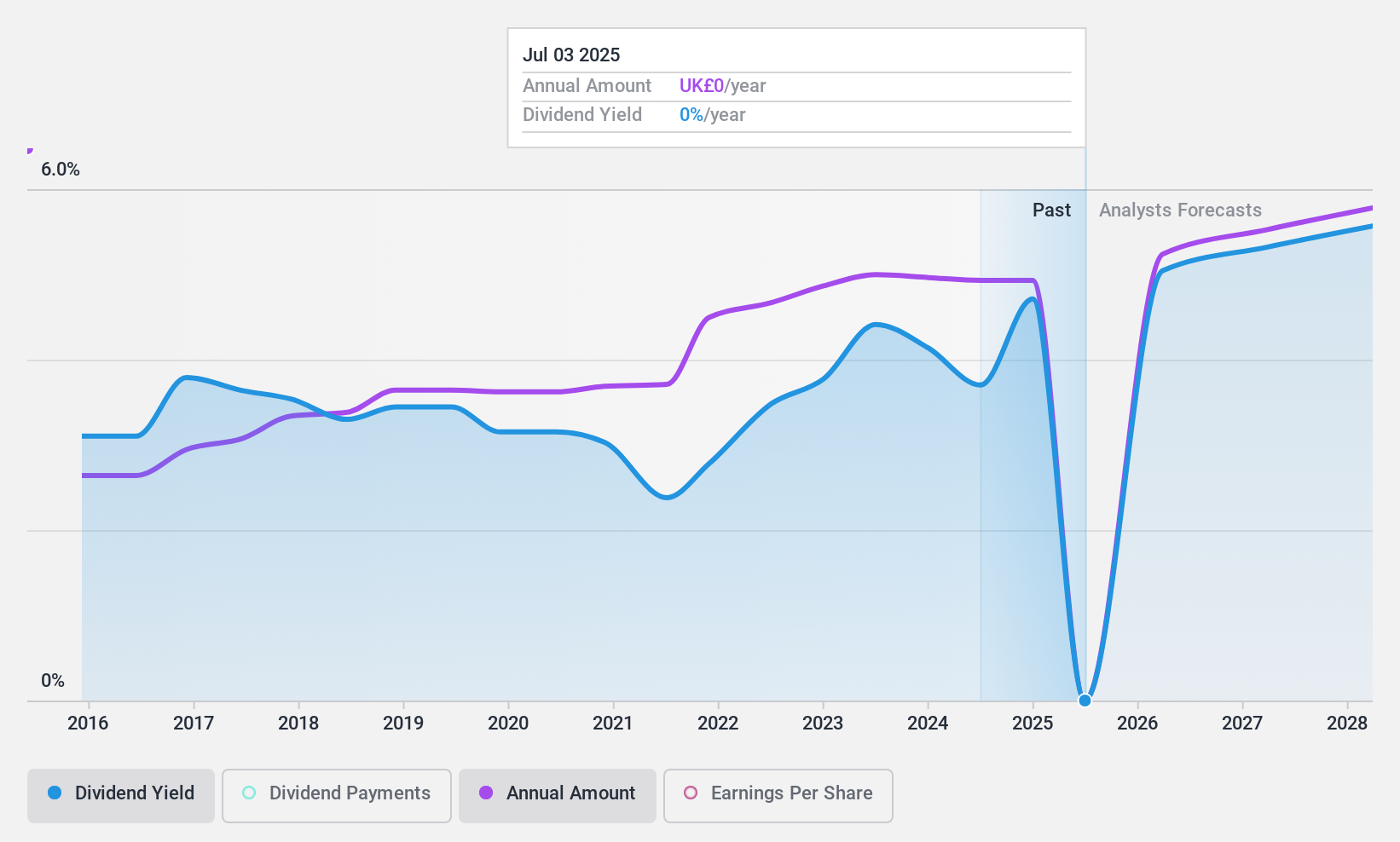

Next 15 Group (AIM:NFG)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Next 15 Group plc, along with its subsidiaries, offers communications services across the United Kingdom, Europe, Africa, the United States, and the Asia Pacific regions and has a market cap of £302.84 million.

Operations: Next 15 Group plc generates revenue through its communications services offered across multiple regions, including the United Kingdom, Europe, Africa, the United States, and the Asia Pacific.

Dividend Yield: 5%

Next 15 Group's dividend payments are well covered by both earnings and cash flows, with low payout ratios of 25.2% and 23.3%, respectively. However, the dividends have been volatile over the past decade, making them less reliable for consistent income. Despite recent earnings growth of 132%, future earnings are expected to decline significantly, which could impact future dividend sustainability. The stock trades at a good value compared to peers but has experienced high volatility recently.

- Dive into the specifics of Next 15 Group here with our thorough dividend report.

- In light of our recent valuation report, it seems possible that Next 15 Group is trading behind its estimated value.

Big Yellow Group (LSE:BYG)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Big Yellow Group is the UK's leading brand in self-storage, with a market cap of £1.81 billion.

Operations: Big Yellow Group generates revenue primarily from the provision of self-storage and related services, amounting to £203.01 million.

Dividend Yield: 4.9%

Big Yellow Group offers a stable dividend history with payments reliably increasing over the past decade, supported by earnings and cash flows with payout ratios around 77%. Although its dividend yield of 4.88% is below the top UK payers, it remains covered by free cash flow. The stock trades at a favorable price-to-earnings ratio of 6.8x compared to the market average and is expected to rise based on analyst targets despite forecasted earnings declines.

- Click here to discover the nuances of Big Yellow Group with our detailed analytical dividend report.

- Our valuation report here indicates Big Yellow Group may be undervalued.

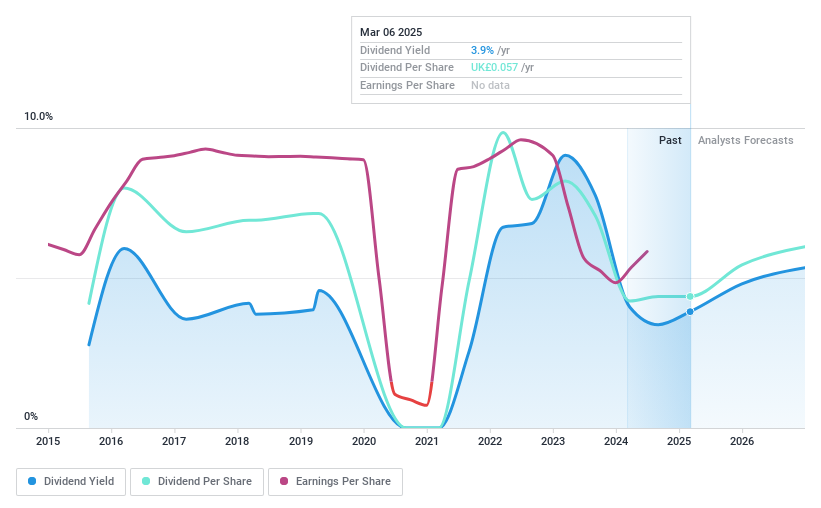

Eurocell (LSE:ECEL)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Eurocell plc manufactures, distributes, and recycles PVC building products such as windows, doors, and roofline components in the UK and Ireland with a market cap of £158.19 million.

Operations: Eurocell plc generates revenue through its Profiles segment, contributing £209.80 million, and its Building Plastics segment, contributing £212.30 million.

Dividend Yield: 3.9%

Eurocell's dividends have grown over the past decade, with a recent 10% increase to 6.1 pence per share for 2024. While its dividend yield of 3.88% is below top UK payers, payouts are well-covered by earnings and cash flows with ratios of 61.3% and 18.1%, respectively. Despite a volatile dividend history, Eurocell's buyback program aims to enhance earnings per share by repurchasing up to £5 million in shares, potentially supporting future dividend stability.

- Delve into the full analysis dividend report here for a deeper understanding of Eurocell.

- The analysis detailed in our Eurocell valuation report hints at an deflated share price compared to its estimated value.

Turning Ideas Into Actions

- Investigate our full lineup of 56 Top UK Dividend Stocks right here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Eurocell might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:ECEL

Eurocell

Engages in manufacture, distribution, and recycling of windows, doors, and roofline polyvinyl chloride (PVC) building products in the United Kingdom and the Republic of Ireland.

Flawless balance sheet, undervalued and pays a dividend.

Similar Companies

Market Insights

Community Narratives