Advertisement

- United Kingdom

- /

- Aerospace & Defense

- /

- AIM:CHRT

Earnings Miss: Cohort plc Missed EPS By 43% And Analysts Are Revising Their Forecasts

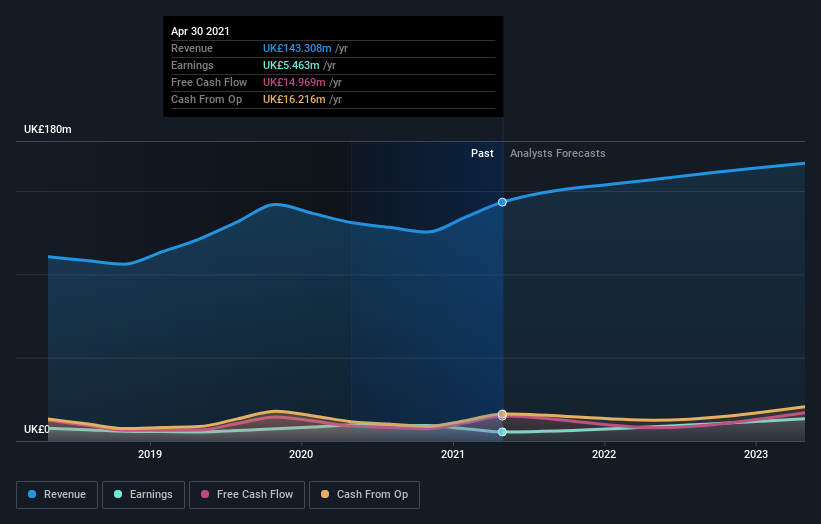

It's been a pretty great week for Cohort plc (LON:CHRT) shareholders, with its shares surging 15% to UK£5.83 in the week since its latest yearly results. Results overall were not great, with earnings of UK£0.13 per share falling drastically short of analyst expectations. Meanwhile revenues hit UK£143m and were slightly better than forecasts. Earnings are an important time for investors, as they can track a company's performance, look at what the analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. With this in mind, we've gathered the latest statutory forecasts to see what the analysts are expecting for next year.

Check out our latest analysis for Cohort

Taking into account the latest results, the consensus forecast from Cohort's three analysts is for revenues of UK£156.8m in 2022, which would reflect a meaningful 9.4% improvement in sales compared to the last 12 months. Per-share earnings are expected to leap 79% to UK£0.24. Yet prior to the latest earnings, the analysts had been anticipated revenues of UK£156.4m and earnings per share (EPS) of UK£0.29 in 2022. So there's definitely been a decline in sentiment after the latest results, noting the substantial drop in new EPS forecasts.

The consensus price target held steady at UK£6.61, with the analysts seemingly voting that their lower forecast earnings are not expected to lead to a lower stock price in the foreseeable future. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. There are some variant perceptions on Cohort, with the most bullish analyst valuing it at UK£6.90 and the most bearish at UK£6.32 per share. The narrow spread of estimates could suggest that the business' future is relatively easy to value, or thatthe analysts have a strong view on its prospects.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. It's clear from the latest estimates that Cohort's rate of growth is expected to accelerate meaningfully, with the forecast 9.4% annualised revenue growth to the end of 2022 noticeably faster than its historical growth of 5.1% p.a. over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to grow their revenue at 4.4% per year. It seems obvious that, while the growth outlook is brighter than the recent past, the analysts also expect Cohort to grow faster than the wider industry.

The Bottom Line

The biggest concern is that the analysts reduced their earnings per share estimates, suggesting business headwinds could lay ahead for Cohort. Fortunately, they also reconfirmed their revenue numbers, suggesting sales are tracking in line with expectations - and our data suggests that revenues are expected to grow faster than the wider industry. The consensus price target held steady at UK£6.61, with the latest estimates not enough to have an impact on their price targets.

With that in mind, we wouldn't be too quick to come to a conclusion on Cohort. Long-term earnings power is much more important than next year's profits. We have estimates - from multiple Cohort analysts - going out to 2023, and you can see them free on our platform here.

However, before you get too enthused, we've discovered 1 warning sign for Cohort that you should be aware of.

When trading Cohort or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About AIM:CHRT

Cohort

Provides a various products and services in defense, security, and related markets in the United Kingdom, Germany, Portugal, Africa, North and South America, and the Asia Pacific and Africa, and other European countries.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|26.3% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|4.8% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor