- France

- /

- Electronic Equipment and Components

- /

- ENXTPA:LBIRD

Lumibird SA (EPA:LBIRD) Just Reported And Analysts Have Been Lifting Their Price Targets

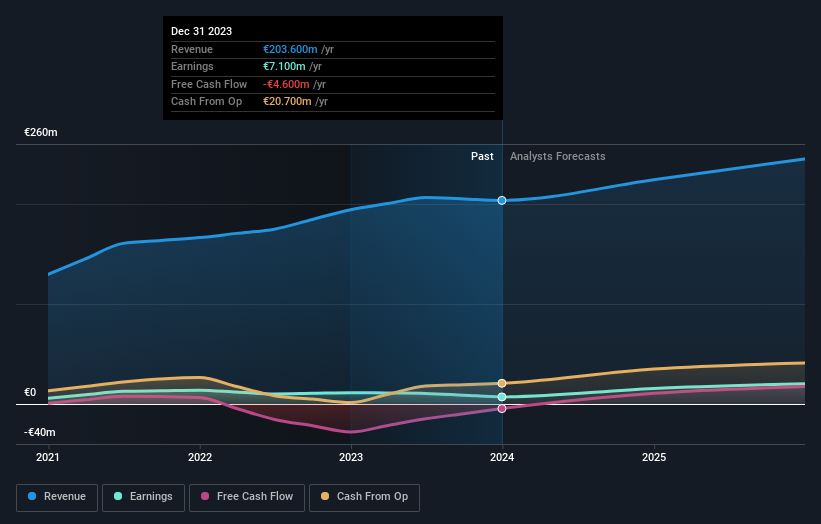

Investors in Lumibird SA (EPA:LBIRD) had a good week, as its shares rose 2.0% to close at €14.08 following the release of its full-year results. It was an okay report, and revenues came in at €204m, approximately in line with analyst estimates leading up to the results announcement. Earnings are an important time for investors, as they can track a company's performance, look at what the analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. So we gathered the latest post-earnings forecasts to see what estimates suggest is in store for next year.

See our latest analysis for Lumibird

Following the latest results, Lumibird's twin analysts are now forecasting revenues of €224.4m in 2024. This would be a solid 10% improvement in revenue compared to the last 12 months. Before this earnings report, the analysts had been forecasting revenues of €222.6m and earnings per share (EPS) of €0.77 in 2024. So we can see that while the consensus made no real change to its revenue estimates, it also no longer provides an earnings per share estimate. This suggests that revenues are what the market is focusing on after the latest results.

The average price target rose 5.3% to €17.85, with the analysts clearly having become more optimistic about Lumibird'sprospects following these results.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. We would highlight that Lumibird's revenue growth is expected to slow, with the forecast 10% annualised growth rate until the end of 2024 being well below the historical 16% p.a. growth over the last five years. Compare this against other companies (with analyst forecasts) in the industry, which are in aggregate expected to see revenue growth of 19% annually. So it's pretty clear that, while revenue growth is expected to slow down, the wider industry is also expected to grow faster than Lumibird.

The Bottom Line

The most important thing to take away is that the analysts reconfirmed their revenue estimates for next year, suggesting that the business is performing in line with expectations. Fortunately, the analysts also reconfirmed their revenue estimates, suggesting that it's tracking in line with expectations. Although our data does suggest that Lumibird's revenue is expected to perform worse than the wider industry. We note an upgrade to the price target, suggesting that the analysts believes the intrinsic value of the business is likely to improve over time.

At least one of Lumibird's twin analysts has provided estimates out to 2025, which can be seen for free on our platform here.

Before you take the next step you should know about the 2 warning signs for Lumibird (1 can't be ignored!) that we have uncovered.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ENXTPA:LBIRD

Lumibird

Designs, manufactures, and sells various lasers for scientific, industrial, and medical applications.

Reasonable growth potential with acceptable track record.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Deep Value Multi Bagger Opportunity

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Unicycive Therapeutics (Nasdaq: UNCY) – Preparing for a Second Shot at Bringing a New Kidney Treatment to Market (TEST)

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026