- France

- /

- Semiconductors

- /

- ENXTPA:ALTRO

Investors Appear Satisfied With Tronic's Microsystems SA's (EPA:ALTRO) Prospects As Shares Rocket 40%

Tronic's Microsystems SA (EPA:ALTRO) shares have had a really impressive month, gaining 40% after a shaky period beforehand. Taking a wider view, although not as strong as the last month, the full year gain of 12% is also fairly reasonable.

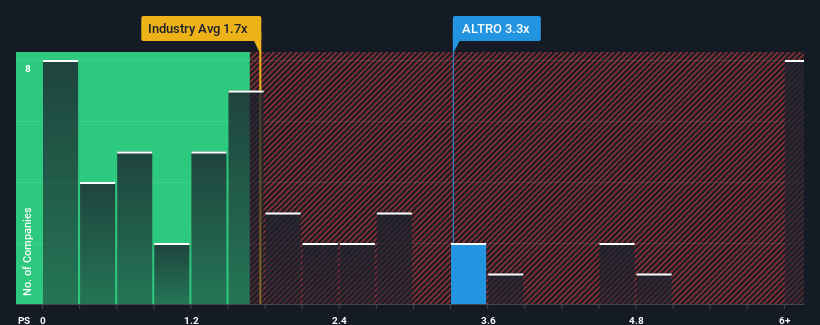

After such a large jump in price, when almost half of the companies in France's Semiconductor industry have price-to-sales ratios (or "P/S") below 1.5x, you may consider Tronic's Microsystems as a stock probably not worth researching with its 3.3x P/S ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the elevated P/S.

Check out our latest analysis for Tronic's Microsystems

How Has Tronic's Microsystems Performed Recently?

Revenue has risen at a steady rate over the last year for Tronic's Microsystems, which is generally not a bad outcome. One possibility is that the P/S ratio is high because investors think this good revenue growth will be enough to outperform the broader industry in the near future. If not, then existing shareholders may be a little nervous about the viability of the share price.

Although there are no analyst estimates available for Tronic's Microsystems, take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.Do Revenue Forecasts Match The High P/S Ratio?

Tronic's Microsystems' P/S ratio would be typical for a company that's expected to deliver solid growth, and importantly, perform better than the industry.

If we review the last year of revenue growth, the company posted a worthy increase of 6.1%. This was backed up an excellent period prior to see revenue up by 57% in total over the last three years. So we can start by confirming that the company has done a great job of growing revenues over that time.

Weighing the recent medium-term upward revenue trajectory against the broader industry's one-year forecast for contraction of 5.1% shows it's a great look while it lasts.

With this in mind, it's clear to us why Tronic's Microsystems' P/S exceeds that of its industry peers. Presumably shareholders aren't keen to offload something they believe will continue to outmanoeuvre the industry. However, its current revenue trajectory will be very difficult to maintain against the headwinds other companies are facing at the moment.

What We Can Learn From Tronic's Microsystems' P/S?

The large bounce in Tronic's Microsystems' shares has lifted the company's P/S handsomely. It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

As detailed previously, the strength of Tronic's Microsystems' recent revenue trends over the medium-term relative to a declining industry is part of the reason why it trades at a higher P/S than its industry counterparts. It could be said that investors feel this revenue growth will continue into the future, justifying a higher P/S ratio. Our only concern is whether its revenue trajectory can keep outperforming under these tough industry conditions. Otherwise, it's hard to see the share price falling strongly in the near future if its revenue performance persists.

Having said that, be aware Tronic's Microsystems is showing 3 warning signs in our investment analysis, and 1 of those shouldn't be ignored.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Tronic's Microsystems might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ENXTPA:ALTRO

Tronic's Microsystems

Manufactures and sells inertial micro-electro-mechanical-system (MEMS) sensor solutions for motion sensing, positioning, and navigation and condition monitoring of assets in France and internationally.

Slight risk and slightly overvalued.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Stride Stock: Online Education Finds Its Second Act

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)