If you have been tracking COFACE (ENXTPA:COFA), the latest shake-up in their executive team has likely caught your attention. The company just named Christina Montes De Oca as the new CEO for its North America region, effective mid-September. This move brings a proven leader with deep experience in commercial strategy and trade credit insurance into a key growth market for COFACE. It signals that the company is looking to sharpen its focus and possibly expand its North American operations. Replacing Oscar Villalonga, who is moving on from the group, Christina joins the Executive Committee and brings with her a track record from both Marsh & McLennan Companies and Allianz Trade North America.

Looking at COFACE's share price, it has had a mixed run lately, with short-term momentum dipping this month but a solid performance year-to-date and over the past year. The stock is up roughly 13% over the past year and has more than tripled investors’ money over five years, though prices have softened over the past month. These movements come as the company posted moderate annual revenue and income growth, keeping the conversation focused on long-term value despite recent fluctuations.

Given the new leadership in a major regional role and this mix of recent performance, investors may be considering whether the market is underestimating COFACE’s growth potential or if everything is already reflected in the price.

Advertisement

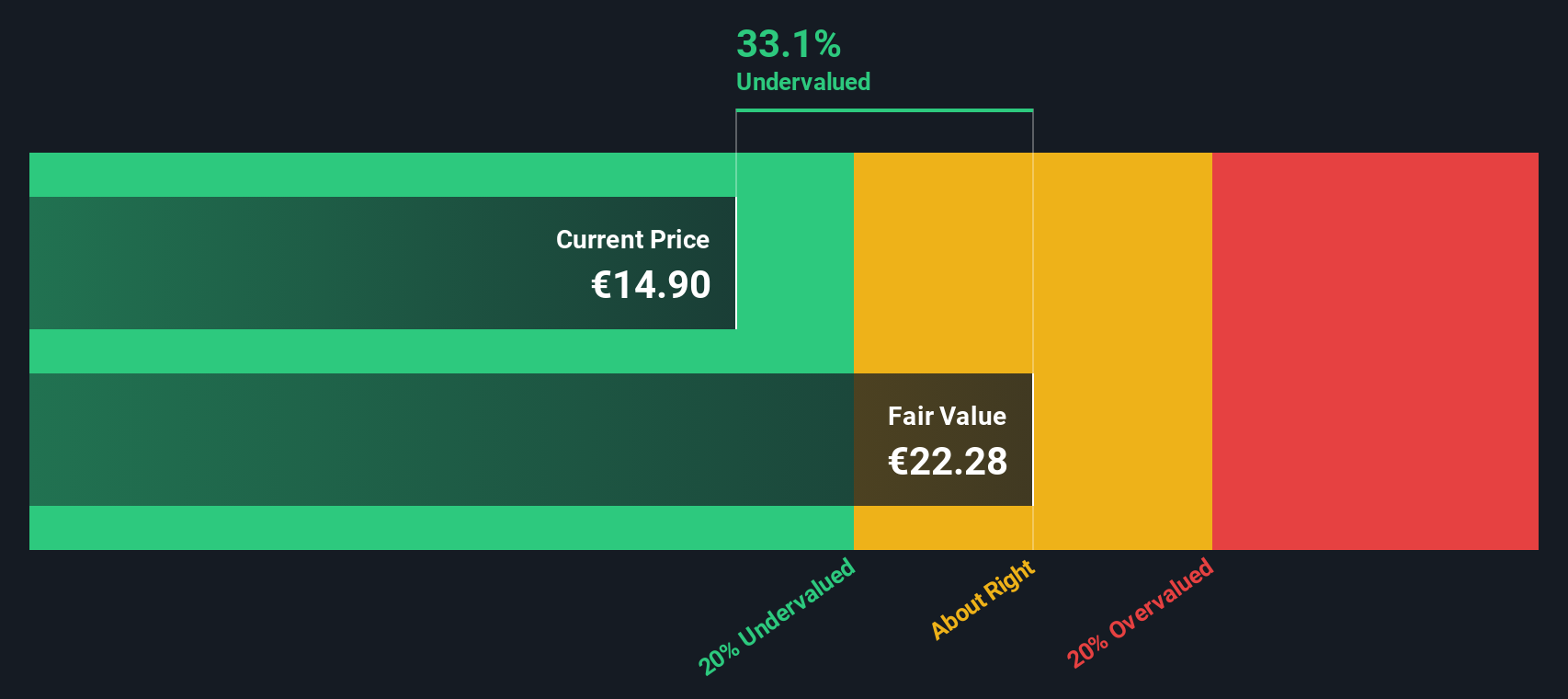

Most Popular Narrative: 15.6% Undervalued

According to the most widely followed narrative, COFACE is viewed as notably undervalued, with a fair value calculation suggesting the shares could be worth significantly more based on future earnings prospects and analyst expectations.

The company's high client retention rate of 92.3% and selective growth strategy are likely to stabilize and potentially increase revenue, contributing to consistent revenue streams. The deliberate investment in technology and data is expected to drive efficiencies and improve net margins over time, enhancing the overall profitability of the company.

Curious how this undervaluation could play out? There is a bigger story than just headline profit and growth rates. This narrative is built on some bold analyst assumptions, including margin trends, company-specific growth levers, and a future valuation multiple that may surprise even seasoned investors. Are you ready to discover what ambitious projections fuel that significant upside and why they could change your outlook for COFACE?

However, ongoing cost pressures and elevated insolvencies could threaten profitability and create challenges for the bullish outlook for COFACE’s long-term growth.

Looking at COFACE through the lens of our DCF model provides a different perspective. This method suggests an even greater degree of undervaluation than the first approach. Could the market be missing something important?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out COFACE for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own COFACE Narrative

If you see things differently, or want to dig deeper into the numbers yourself, you can develop your own take in just a few minutes. Do it your way

Don’t let potential opportunities pass you by. Now is the time to take your investing to the next level. Maximize your strategy with handpicked stocks from themes shaping the future of markets.

Boost your portfolio’s income by tapping into companies offering dividend stocks with yields > 3% and enjoy the steady rewards of strong dividend yields.

Spot market movers with growth potential by tracking promising businesses trading below their true value via undervalued stocks based on cash flows before the rest of the crowd catches on.

Jump on the innovation trend and join the wave of transformation with smart picks among next-gen healthcare disruptors using healthcare AI stocks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield) • Undervalued Small Caps with Insider Buying • High growth Tech and AI Companies

Through its subsidiaries, provides credit insurance products and related services for microenterprises, small and medium enterprises, mid-market companies, international corporations, financial institutions, and clients of distribution partners.