Advertisement

- France

- /

- Oil and Gas

- /

- ENXTPA:MAU

Etablissements Maurel & Prom S.A. (EPA:MAU) Surges 27% Yet Its Low P/E Is No Reason For Excitement

Etablissements Maurel & Prom S.A. (EPA:MAU) shareholders would be excited to see that the share price has had a great month, posting a 27% gain and recovering from prior weakness. Looking further back, the 15% rise over the last twelve months isn't too bad notwithstanding the strength over the last 30 days.

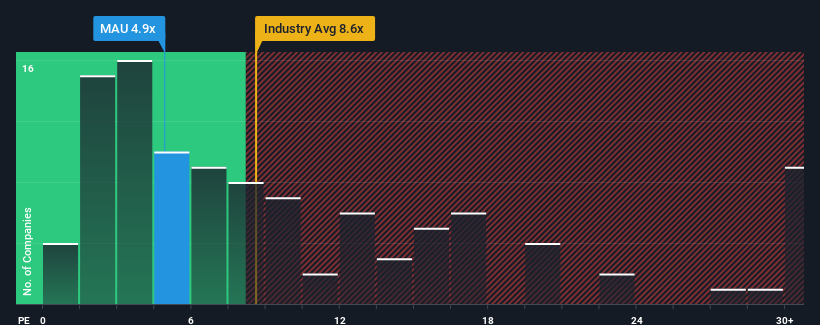

Although its price has surged higher, Etablissements Maurel & Prom may still be sending very bullish signals at the moment with its price-to-earnings (or "P/E") ratio of 4.9x, since almost half of all companies in France have P/E ratios greater than 15x and even P/E's higher than 25x are not unusual. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so limited.

With its earnings growth in positive territory compared to the declining earnings of most other companies, Etablissements Maurel & Prom has been doing quite well of late. It might be that many expect the strong earnings performance to degrade substantially, possibly more than the market, which has repressed the P/E. If not, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

See our latest analysis for Etablissements Maurel & Prom

Is There Any Growth For Etablissements Maurel & Prom?

The only time you'd be truly comfortable seeing a P/E as depressed as Etablissements Maurel & Prom's is when the company's growth is on track to lag the market decidedly.

Retrospectively, the last year delivered an exceptional 115% gain to the company's bottom line. The strong recent performance means it was also able to grow EPS by 452% in total over the last three years. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

Shifting to the future, estimates from the three analysts covering the company suggest earnings growth is heading into negative territory, declining 11% each year over the next three years. That's not great when the rest of the market is expected to grow by 14% per year.

With this information, we are not surprised that Etablissements Maurel & Prom is trading at a P/E lower than the market. Nonetheless, there's no guarantee the P/E has reached a floor yet with earnings going in reverse. There's potential for the P/E to fall to even lower levels if the company doesn't improve its profitability.

What We Can Learn From Etablissements Maurel & Prom's P/E?

Even after such a strong price move, Etablissements Maurel & Prom's P/E still trails the rest of the market significantly. It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

We've established that Etablissements Maurel & Prom maintains its low P/E on the weakness of its forecast for sliding earnings, as expected. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. It's hard to see the share price rising strongly in the near future under these circumstances.

Before you settle on your opinion, we've discovered 2 warning signs for Etablissements Maurel & Prom (1 is a bit unpleasant!) that you should be aware of.

It's important to make sure you look for a great company, not just the first idea you come across. So take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

Valuation is complex, but we're here to simplify it.

Discover if Etablissements Maurel & Prom might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ENXTPA:MAU

Etablissements Maurel & Prom

Engages in exploration and production of oil and gas, and hydrocarbons in Gabon, Tanzania, Angola, and Venezuela.

Very undervalued with flawless balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.4% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|6.1% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.2% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.6% undervalued

BE

Community Contributor