Advertisement

- France

- /

- Food and Staples Retail

- /

- ENXTPA:CO

Casino, Guichard-Perrachon S.A. (EPA:CO) Soars 33% But It's A Story Of Risk Vs Reward

Those holding Casino, Guichard-Perrachon S.A. (EPA:CO) shares would be relieved that the share price has rebounded 33% in the last thirty days, but it needs to keep going to repair the recent damage it has caused to investor portfolios. But the last month did very little to improve the 99% share price decline over the last year.

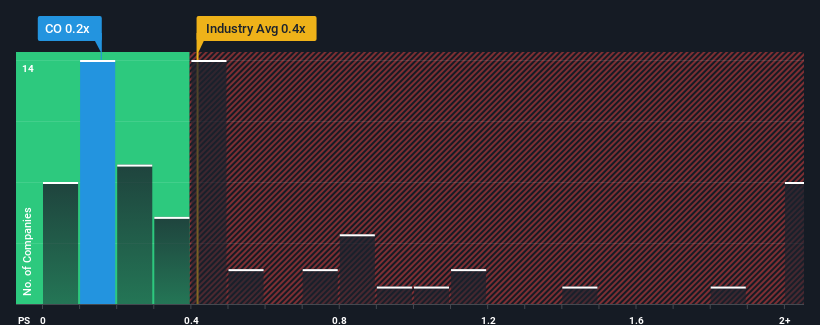

Although its price has surged higher, it's still not a stretch to say that Casino Guichard-Perrachon's price-to-sales (or "P/S") ratio of 0.2x right now seems quite "middle-of-the-road" compared to the Consumer Retailing industry in France, where the median P/S ratio is around 0.4x. While this might not raise any eyebrows, if the P/S ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

View our latest analysis for Casino Guichard-Perrachon

How Casino Guichard-Perrachon Has Been Performing

While the industry has experienced revenue growth lately, Casino Guichard-Perrachon's revenue has gone into reverse gear, which is not great. Perhaps the market is expecting its poor revenue performance to improve, keeping the P/S from dropping. However, if this isn't the case, investors might get caught out paying too much for the stock.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Casino Guichard-Perrachon.How Is Casino Guichard-Perrachon's Revenue Growth Trending?

The only time you'd be comfortable seeing a P/S like Casino Guichard-Perrachon's is when the company's growth is tracking the industry closely.

In reviewing the last year of financials, we were disheartened to see the company's revenues fell to the tune of 6.2%. This means it has also seen a slide in revenue over the longer-term as revenue is down 72% in total over the last three years. Accordingly, shareholders would have felt downbeat about the medium-term rates of revenue growth.

Looking ahead now, revenue is anticipated to climb by 327% during the coming year according to the three analysts following the company. That's shaping up to be materially higher than the 6.4% growth forecast for the broader industry.

With this in consideration, we find it intriguing that Casino Guichard-Perrachon's P/S is closely matching its industry peers. It may be that most investors aren't convinced the company can achieve future growth expectations.

The Bottom Line On Casino Guichard-Perrachon's P/S

Casino Guichard-Perrachon's stock has a lot of momentum behind it lately, which has brought its P/S level with the rest of the industry. Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that Casino Guichard-Perrachon currently trades on a lower than expected P/S since its forecasted revenue growth is higher than the wider industry. When we see a strong revenue outlook, with growth outpacing the industry, we can only assume potential uncertainty around these figures are what might be placing slight pressure on the P/S ratio. However, if you agree with the analysts' forecasts, you may be able to pick up the stock at an attractive price.

Don't forget that there may be other risks. For instance, we've identified 4 warning signs for Casino Guichard-Perrachon (2 are potentially serious) you should be aware of.

If these risks are making you reconsider your opinion on Casino Guichard-Perrachon, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ENXTPA:CO

Casino Guichard-Perrachon

Operates as a food retailer in France, Latin America, and internationally.

Slight and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|24.5% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|45.3% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|33.9% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|56.1% undervalued

AX

Community Contributor